2019 PN Hesi Exit V1

Education > QUESTIONS & ANSWERS > Test Bank Chapter 9 Inventories Additional Valuation Issues. (All)

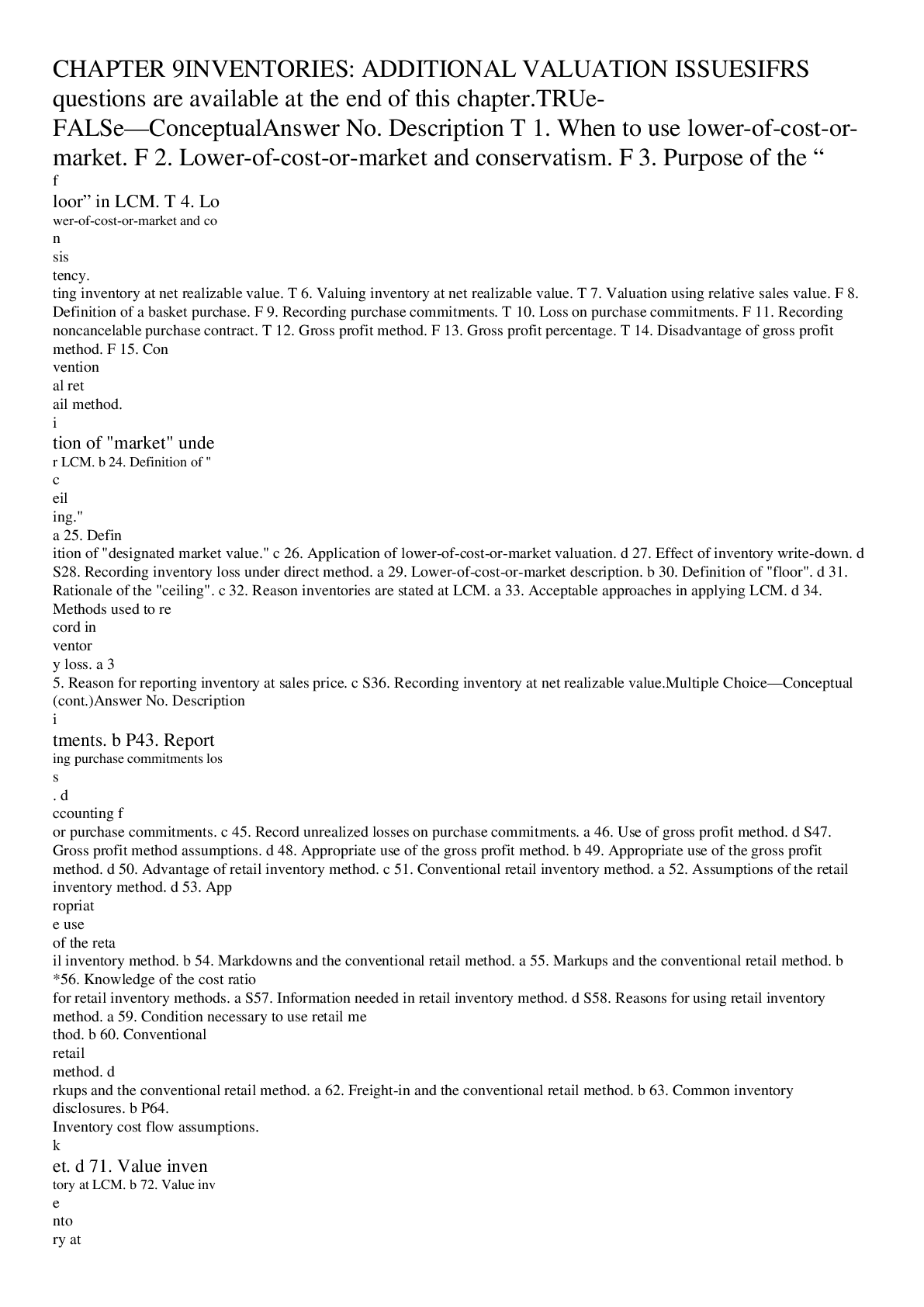

Test Bank Chapter 9 Inventories Additional Valuation Issues. CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES IFRS questions are available at the end of this chapter. TRU ... E-FALSE—Conceptual Description T 1. When to use lower-of-cost-or-market. F 2. Lower-of-cost-or-market and conservatism. F 3. Purpose of the “floor” in LCM. T 4. Lower-of-cost-or-market and consistency. F 5. Reporting inventory at net realizable value. T 6. Valuing inventory at net realizable value. T 7. Valuation using relative sales value. F 8. Definition of a basket purchase. F 9. Recording purchase commitments. T 10. Loss on purchase commitments. F 11. Recording noncancelable purchase contract. T 12. Gross profit method. F 13. Gross profit percentage. T 14. Disadvantage of gross profit method. F 15. Conventional retail method. F 16. Definition of markup. T 17. Accounting for abnormal shortages. F 18. Computing inventory turnover ratio. T 19. Average days to sell inventory. T 20 LIFO retail method. MULTIPLE CHOICE—Conceptual Description d 21. Knowledge of lower-of-cost-or-market valuations. d 22. Appropriate use of LCM valuation. c 23. Definition of "market" under LCM. b 24. Definition of "ceiling." a 25. Definition of "designated market value." c 26. Application of lower-of-cost-or-market valuation. d 27. Effect of inventory write-down. d S28. Recording inventory loss under direct method. a 29. Lower-of-cost-or-market description. b 30. Definition of "floor". d 31. Rationale of the "ceiling". c 32. Reason inventories are stated at LCM. a 33. Acceptable approaches in applying LCM. d 34. Methods used to record inventory loss. a 35. Reason for reporting inventory at sales price. c S36. Recording inventory at net realizable value. MULTIPLE CHOICE—Conceptual (cont.) Description b 37. Net realizable value under LCM. d 38. Definition of "net realizable value." a 39. Valuation of inventory at net realizable value. d 40. Appropriate use of net realizable value. a 41. Material purchase commitments. a 42. Loss recognition on purchase commitments. b P43. Reporting purchase commitments loss. d 44. Accounting for purchase commitments. c 45. Record unrealized losses on purchase commitments. a 46. Use of gross profit method. d S47. Gross profit method assumptions. d 48. Appropriate use of the gross profit method. b 49. Appropriate use of the gross profit method. d 50. Advantage of retail inventory method. c 51. Conventional retail inventory method. a 52. Assumptions of the retail inventory method. d 53. Appropriate use of the retail inventory method. b 54. Markdowns and the conventional retail method. a 55. Markups and the conventional retail method. b *56. Knowledge of the cost ratio for retail inventory methods. a S57. Information needed in retail inventory method. d S58. Reasons for using retail inventory method. a 59. Condition necessary to use retail method. b 60. Conventional retail method. d 61. Net markups and the conventional retail method. a 62. Freight-in and the conventional retail method. b 63. Common inventory disclosures. b P64. Inventory cost flow assumptions. a P65. Computing average days to sell inventory. c 66. Inventory turnover ratio. c *67. Dollar-value LIFO retail method. MULTIPLE CHOICE—Computational Description a 68. Value inventory at LCM. b 69. Lower-of-cost-or-market. b 70. Lower-of-cost-or-market. d 71. Value inventory at LCM. b 72. Value inventory at LCM. c 73. Value inventory at LCM. c 74. Determine market value under LCM. b 75. Value inventory under LCM. d 76. Determine cost amount under LCM. c 77. Value inventory under LCM. b 78. Value inventory under LCM. a 79. Value inventory under LCM. c 80. Value inventory under LCM. MULTIPLE CHOICE—Computational (cont.) Description c 81. Determining net realizable value. c 82. Determining net realizable value. b 83. Relative sales value method. b 84. Relative sales value method. c 85. Relative sales method of inventory valuation. b 86. Calculate cost using relative sales value method. d 87. Calculate cost using relative sales value method. a 88. Calculate cost using relative sales value method. a 89. Entry for purchase commitment loss. c 90. Recording purchase under purchase commitment. c 91. Entry for purchase commitment loss. c 92. Recognizing loss on purchase commitments. b 93. Recognizing loss on purchase commitments. a 94. Estimating ending inventory using gross profit method. a 95. Estimating ending inventory using gross profit method. d 96. Calculate cost of goods sold given a markup on cost. d 97. Calculate merchandise purchases given a markup on cost. a 98. Calculate total sales from cost information. a 99. Markup on cost equivalent to a markup on selling price. b 100. Estimate ending inventory using gross profit method. c 101. Calculate ending inventory using gross profit method . b 102. Calculate ending inventory using gross profit method. a 103. Estimate cost of inventory destroyed by fire. a 104. Determine items to be included in inventory. c 105. Determine gross profit as percentage of cost. c 106. Calculate gross profit amount. d 107. Calculate ending inventory using gross profit method. d 108. Calculate ending inventory using gross profit method. c 109. Calculate ending inventory using gross profit method. a 110. Calculate ending inventory using conventional retail. c 111. Calculate ending inventory using conventional retail. b 112. Calculate ending inventory using conventional retail. b 113. Calculate cost of retail ratio to approximate LCM. b 114. Calculate ending inventory at retail. a 115. Calculate cost to retail ratio approximating LCM. b 116. Calculate cost of inventory lost using retail method. b *117. Calculate ending inventory at cost using LIFO retail. c *118. Determine cost to retail ratio using LIFO retail. a 119. Calculate ending inventory at retail. a 120. Calculate ending inventory at retail. c 121. Average days to sell inventory. c 122. Average days to sell inventory. b 123. Calculate inventory turnover ratio. d 124. Calculate inventory turnover ratio. d 125. Determine cost to retail ratio to approximate LCM. d 126. Calculate ending inventory at retail. a 127. Calculate ending inventory using conventional retail. c *128. Determine cost to retail ratio using LIFO cost. a *129. Calculate ending inventory cost using dollar-value LIFO. MULTIPLE CHOICE—Computational (cont.) Description b *130. Calculate cost of ending inventory using LIFO retail. a *131. Calculate ending inventory cost using dollar-value LIFO. P These questions also appear in the Problem-Solving Survival Guide. S These questions also appear in the Study Guide. * This topic is dealt with in an Appendix to the chapter. MULTIPLE CHOICE—CPA Adapted Description d 132. Recognizing a loss due to LCM. b 133. Appropriate use of replacement costs in LCM. b 134. Identification of the designated market value. a 135. Estimate cost of inventory lost by theft. a 136. Determine cost of ending inventory using retail method. d 137. Determine cost of ending inventory using retail method. a *138. Calculate ending inventory using LIFO retail. EXERCISES Item Description E9-139 Lower-of-cost-or-market. E9-140 Lower-of-cost-or-market. E9-141 Lower-of-cost-or-market. E9-142 Lower-of-cost-or-market. E9-143 Lower-of-cost-or-market. E9-144 Relative sales value method. E9-145 Gross profit method. E9-146 Gross profit method. E9-147 Gross profit method. E9-148 Comparison of inventory methods. PROBLEMS Item Description P9-149 Gross profit method. P9-150 Retail inventory method. *P9-151 Retail inventory method. *P9-152 LIFO retail inventory method, fluctuating prices. *P9-153 LIFO retail inventory method, stable prices. *P9-154 Dollar-value LIFO retail method. *P9-155 Retail LIFO. CHAPTER LEARNING OBJECTIVES 1. Describe and apply the lower-of-cost-or-market rule. 2. Explain when companies value inventories at net realizable value. 3. Explain when companies use the relative sales value method to value inventories. 4. Discuss accounting issues related to purchase commitments. 5. Determine ending inventory by applying the gross profit method. 6. Determine ending inventory by applying the retail inventory method. 7. Explain how to report and analyze inventory. *8. Determine ending inventory by applying the LIFO retail methods. *SUMMARY OF LEARNING OBJECTIVES BY QUESTIONS Item Type Item Type Item Type Item Type Item Type Item Type Item Type Learning Objective 1 1. TF 23. MC 29. MC 68. MC 74. MC 80. MC 141. E 2. TF 24. MC 30. MC 69. MC 75. MC 132. MC 142. E 3. TF 25. MC 31. MC 70. MC 76. MC 133. MC 143. E 4. TF 26. MC 32. MC 71. MC 77. MC 134. MC 148. E 21. MC 27. MC 33. MC 72. MC 78. MC 139. E 22. MC S28. MC 34. MC 73. MC 79. MC 140. E Learning Objective 2 5. TF 35. MC 37. MC 39. MC 81. MC &n [Show More]

Last updated: 3 years ago

Preview 1 out of 30 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

Can't find what you want? Try our AI powered Search

Connected school, study & course

About the document

Uploaded On

Nov 04, 2020

Number of pages

30

Written in

All

This document has been written for:

Uploaded

Nov 04, 2020

Downloads

0

Views

71

Scholarfriends.com Online Platform by Browsegrades Inc. 651N South Broad St, Middletown DE. United States.

We're available through e-mail, Twitter, and live chat.

FAQ

Questions? Leave a message!

Copyright © Scholarfriends · High quality services·

.png)