Portage Learning Set M1. Biochemistry Quizzes and answers. Rated A+.

Financial Accounting > QUESTIONS & ANSWERS > Strayer University ACC 403. Week 9 Homework. Questions and Answers. (All)

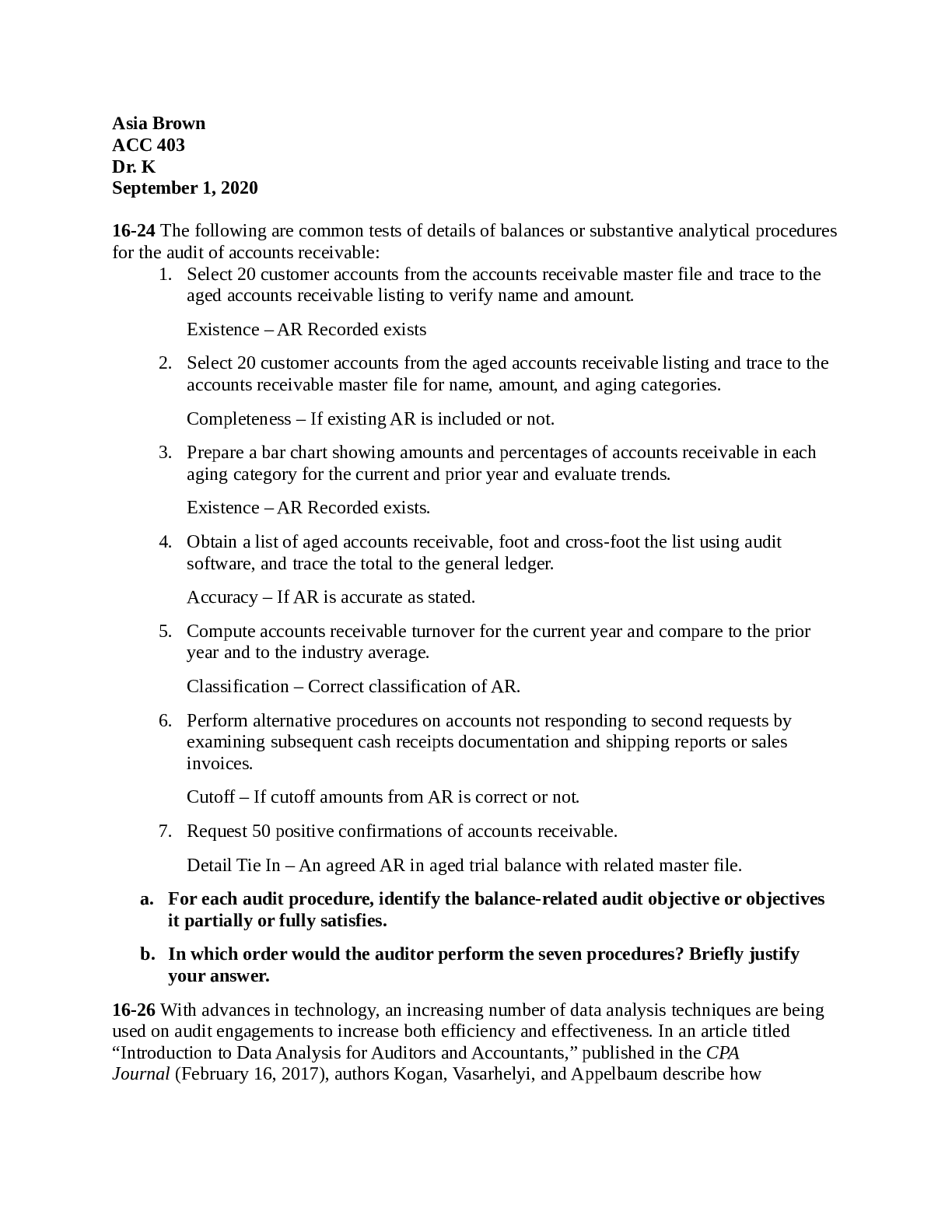

16-24 The following are common tests of details of balances or substantive analytical procedures for the audit of accounts receivable: 1. Select 20 customer accounts from the accounts receivable mas ... ter file and trace to the aged accounts receivable listing to verify name and amount. Existence – AR Recorded exists 2. Select 20 customer accounts from the aged accounts receivable listing and trace to the accounts receivable master file for name, amount, and aging categories. Completeness – If existing AR is included or not. 3. Prepare a bar chart showing amounts and percentages of accounts receivable in each aging category for the current and prior year and evaluate trends. Existence – AR Recorded exists. 4. Obtain a list of aged accounts receivable, foot and cross-foot the list using audit software, and trace the total to the general ledger. Accuracy – If AR is accurate as stated. 5. Compute accounts receivable turnover for the current year and compare to the prior year and to the industry average. Classification – Correct classification of AR. 6. Perform alternative procedures on accounts not responding to second requests by examining subsequent cash receipts documentation and shipping reports or sales invoices. Cutoff – If cutoff amounts from AR is correct or not. 7. Request 50 positive confirmations of accounts receivable. Detail Tie In – An agreed AR in aged trial balance with related master file. a. For each audit procedure, identify the balance-related audit objective or objectives it partially or fully satisfies. b. In which order would the auditor perform the seven procedures? Briefly justify your answer. 16-26 With advances in technology, an increasing number of data analysis techniques are being used on audit engagements to increase both efficiency and effectiveness. In an article titled “Introduction to Data Analysis for Auditors and Accountants,” published in the CPA Journal (February 16, 2017), authors Kogan, Vasarhelyi, and Appelbaum describe howtechnology-driven data analysis can be used in all stages of the audit. Read the article on data analysis (available at www.cpajournal.com) to answer the following questions: a. The authors discuss the emphasis on “audit by exception” when using data analysis. What does “audit by exception” mean and how does it differ from a traditional audit approach using statistical sampling? How does an auditor identify the exceptions? Modern audit engagements often involve examination of clients that are using Big Data and analytics to remain competitive and relevant in today's business environment. Client systems now are integrated with the cloud, the Internet of Things, and external data sources such as social media. b. The authors note that data visualization can be used to conduct exploratory data analysis. Describe how data visualization could be used in the audit of the sales and collection cycle. Data visualization is another form of visual art that grabs our interest and keeps our eyes on the message. When we see a chart, we quickly see trends and outliers. If we can see something, we internalize it quickly. It’s storytelling with a purpose. If you’ve ever stared at a massive spreadsheet of data and couldn’t see a trend, you know how much more effective a visualization can be. c. Choose one of the methods identified by the authors as emerging approaches, for example blockchain or deep learning, and discuss how an auditor might test one of the accounts receivable balance-related audit objectives using this method. Blockchain technology. Despite such advancements, the application of blockchain to accounting and assurance remains under-explored. 16-35 The following are various changes in audit circumstances. Audit Circumstance 1. The client began experiencing an increase in returns due to product changes that resulted in increased defects. a 2. You found several pricing errors in your substantive tests of transactions for sales. h 3. In performing substantive tests of transactions for cash receipts, you found that receipts were promptly recorded in customer accounts, but there were delays in depositing the receipts at the bank. d 4. The client entered into a new loan agreement with the bank. Accounts receivable are pledged as collateral for the loan.f 5. The client did not reconcile the accounts receivable subsidiary records with the accounts receivable balance in the general ledger on a regular basis. c 6. Substantive analytical procedures indicated a significant slowing in accounts receivable turnover. g 7. The client entered into sales contracts with new customers that differ from the client’s standard sales contracts. b 8. The client had a significant increase in sales near year end. e 9. Accounts receivable confirmations were ineffective due to a very low response rate in the prior-year audit. i Match each change in audit circumstance with the most likely test of details of balances response. Each response is used once. a. Expand testing of sales returns after year end and compare the level of returns with the prior year. b. Send positive confirmations that include requests for information on side agreements and special terms. c. Increase the number of accounts traced from the accounts receivable trial balance to the accounts receivable subsidiary records. d. Expand the review of cash receipts after year end to evaluate the collectibility of accounts receivable. e. Increase the sample size for sales cutoff testing for sales recorded before year end. f. Send a confirmation to the bank confirming amounts pledged as collateral under loan agreements. g. Increase the sample size for positive confirmations of accounts receivable. h. While at the client’s premises at year end, obtain information on the last few cash receipts at year end for cash receipts cutoff testing. i. Perform alternative procedures to test the existence and accuracy of accounts receivable instead of sending positive confirmations. [Show More]

Last updated: 3 years ago

Preview 1 out of 11 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

.png)

Virginia Commonwealth University BIOC 403 Biochemistry_BIOCHEM 403 Test2 . 25 Q&A Virginia Commonwealth University BIOC 403 Summer Test2 Key Biochemistry 403 Exam #2 Virginia Commonwealth Univer...

By QuizMaster 3 years ago

$19

5

Can't find what you want? Try our AI powered Search

Connected school, study & course

About the document

Uploaded On

Apr 04, 2022

Number of pages

11

Written in

All

This document has been written for:

Uploaded

Apr 04, 2022

Downloads

0

Views

248

Scholarfriends.com Online Platform by Browsegrades Inc. 651N South Broad St, Middletown DE. United States.

We're available through e-mail, Twitter, Facebook, and live chat.

FAQ

Questions? Leave a message!

Copyright © Scholarfriends · High quality services·