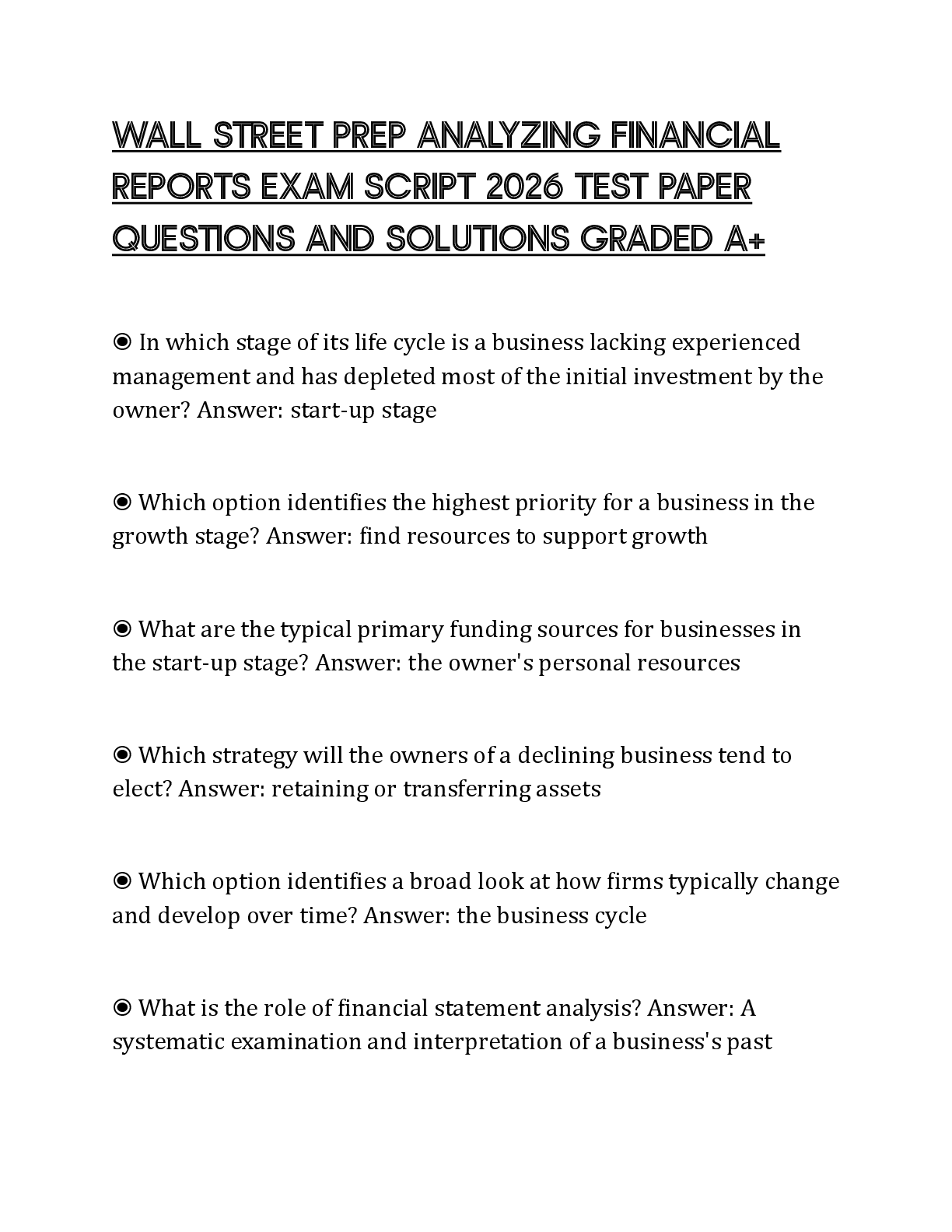

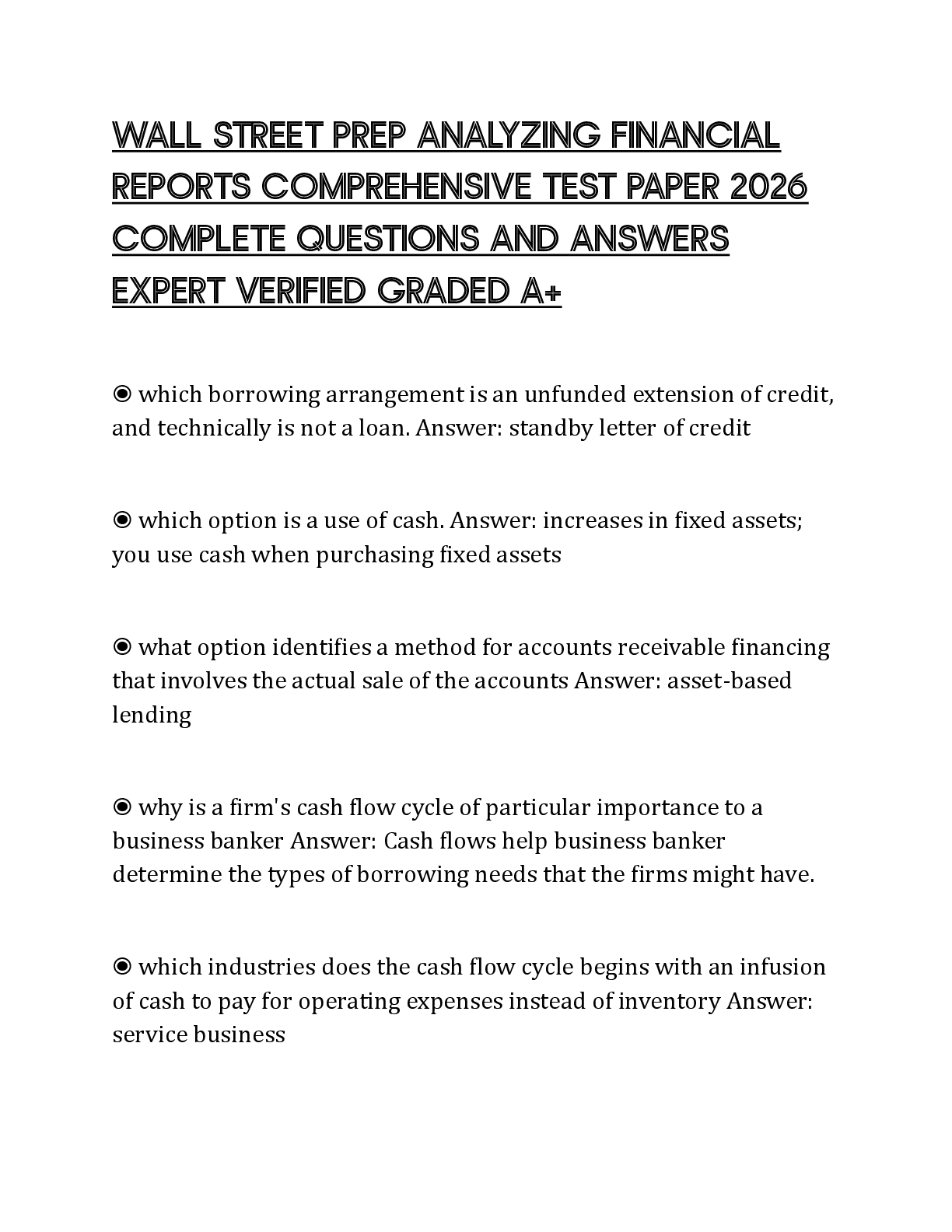

Wall Street Prep Fixed Income and Debt

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 5 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Also available in bundle (1)

Click Below to Access Bundle(s)

BUNDLE FOR Excel Crash Course Exam from Wall Street Prep - Wall Street Prep

Excel Crash Course Exam from Wall Street Prep - Wall Street Prep. Excel Crash Course Exam from Wall Street Prep - Wall Street Prep. Completed Exam Wall Street Prep Wall Street Prep Wall Stree...

By clairegrades 4 years ago

$25

5

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jul 16, 2022

Number of pages

5

Written in

All

Additional information

This document has been written for:

Uploaded

Jul 16, 2022

Downloads

0

Views

128

Document Keyword Tags

Recommended For You

Get more on EXAM »

Excel Crash Course Exam from Wall Street Prep - Wall Street Pr...

Excel Crash Course Exam from Wall Street Prep - Wall Street Pr...

Excel Crash Course Exam from Wall Street Prep - Wall Street Pr...

.png)

Fundamentals of Corporate Finance, 5e Robert Parrino, David K...

.png)

Financial Management for Public, Health, and Not-for-Profit Or...

.png)

.png)

.png)