Solution for ACCT2101 Final Exam Practice Questions _revised 2022

Document Content and Description Below

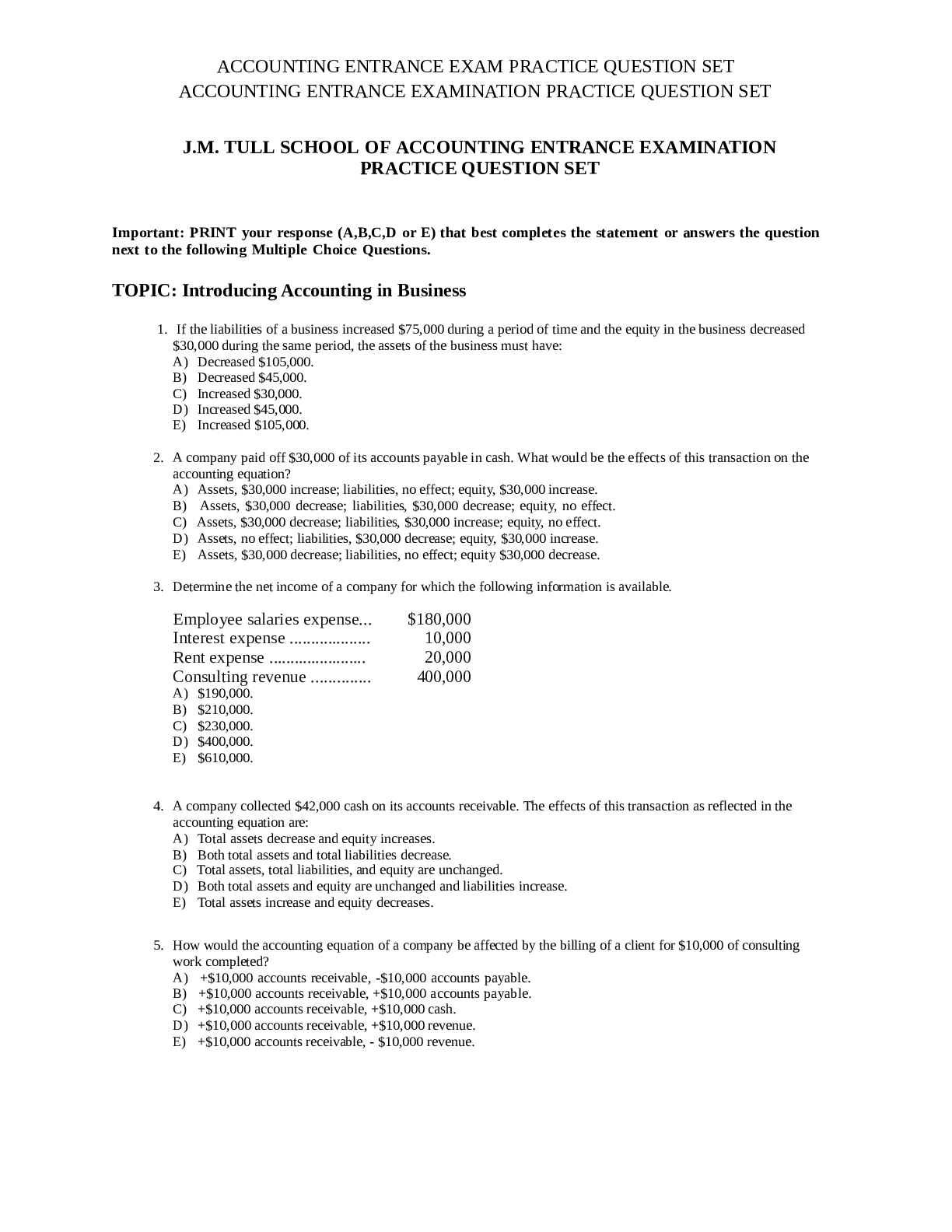

Final Exam Practice Questions

SECTION A: MULTIPLE CHOICE QUESTIONS

1. Financial stability refers to the ability of an entity to:

a) minimise expenses.

b) increase market share.

c) meet long-term obligations.

d) ach

...

[Show More]

Last updated: 3 years ago

Preview 1 out of 14 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Nov 10, 2022

Number of pages

14

Written in

All

Additional information

This document has been written for:

Uploaded

Nov 10, 2022

Downloads

0

Views

174

Document Keyword Tags

Recommended For You

Get more on EXAM » (1).png)

$5.5

13 Pages

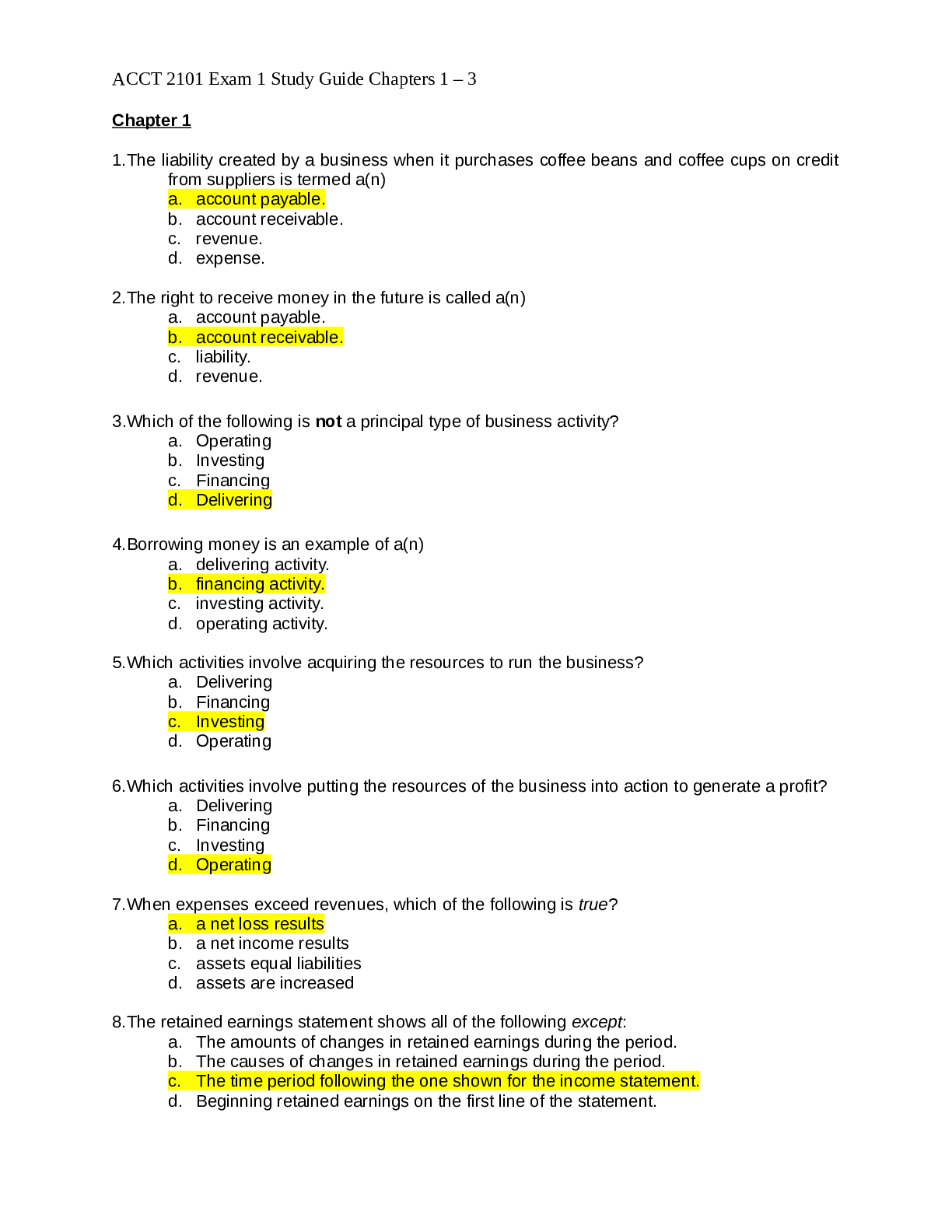

ACCT 2101 Exam 1 Study Guide Chapters 1 – 3 questions with ans...

$7.5

13 Pages

ACCT2101: ACCOUNTING ENTRANCE EXAM PRACTICE QUESTION SET (J.M....

$15

13 Pages

ACCT 2101 EXAM 1 STUDY GUIDE CHAPTER 1-3 QUESTIONS AND ANSWERS

.png)

$15

12 Pages

ACCT 2101 Exam 2 Study Guide Chapters 4, 5, & 7 QUESTIONS WELL...

.png)

$17

13 Pages

ACCT 2101X EAM 2 STUDY GUIDE CHAPTER 4-6 QUESTIONS WELL SOLVED...

$13

26 Pages

Louisiana State University ACCT 2101 ch10 ( 120 QUESTIONS WITH...

$20

566 Pages

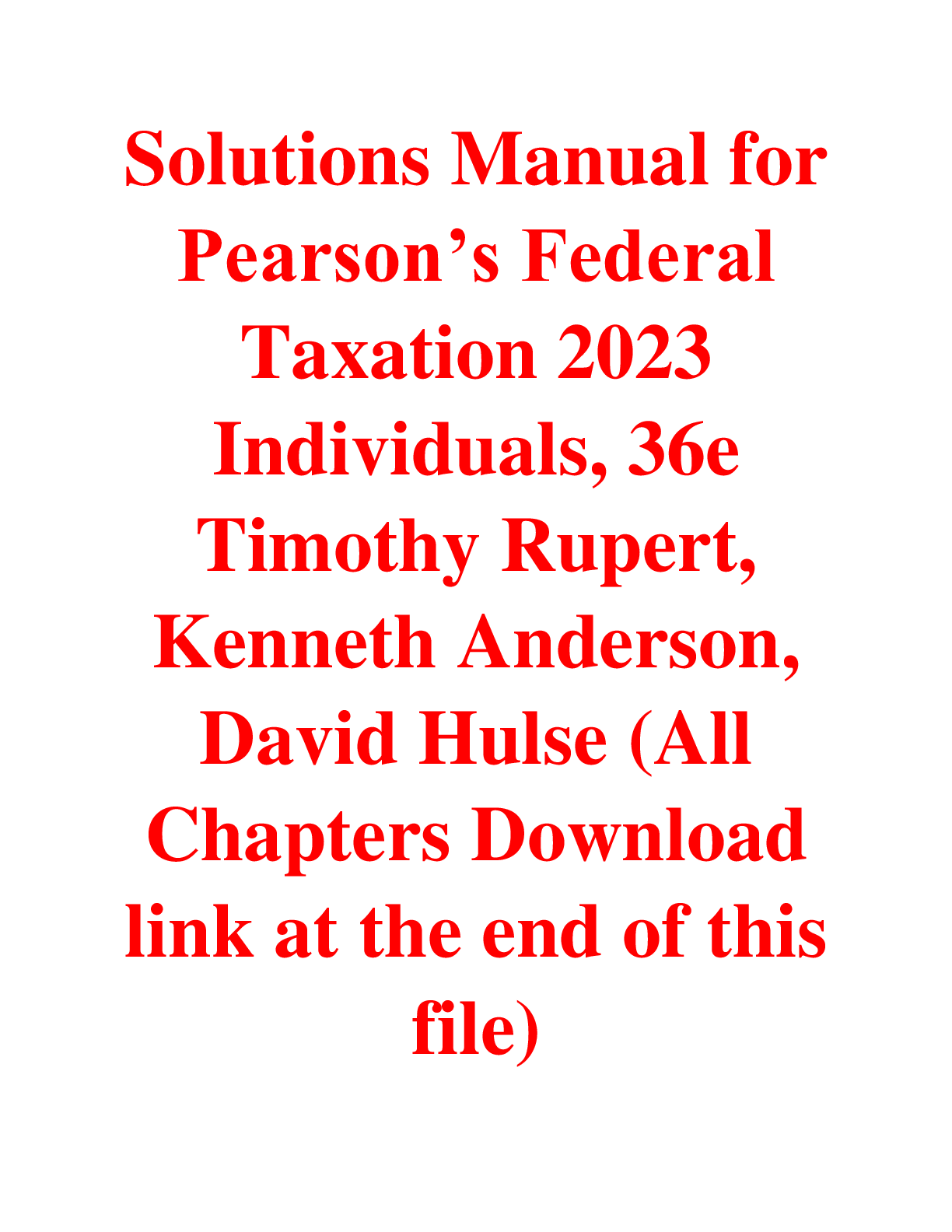

Pearson’s Federal Taxation 2023 Individuals, 36e Timothy Ruper...

$20

643 Pages

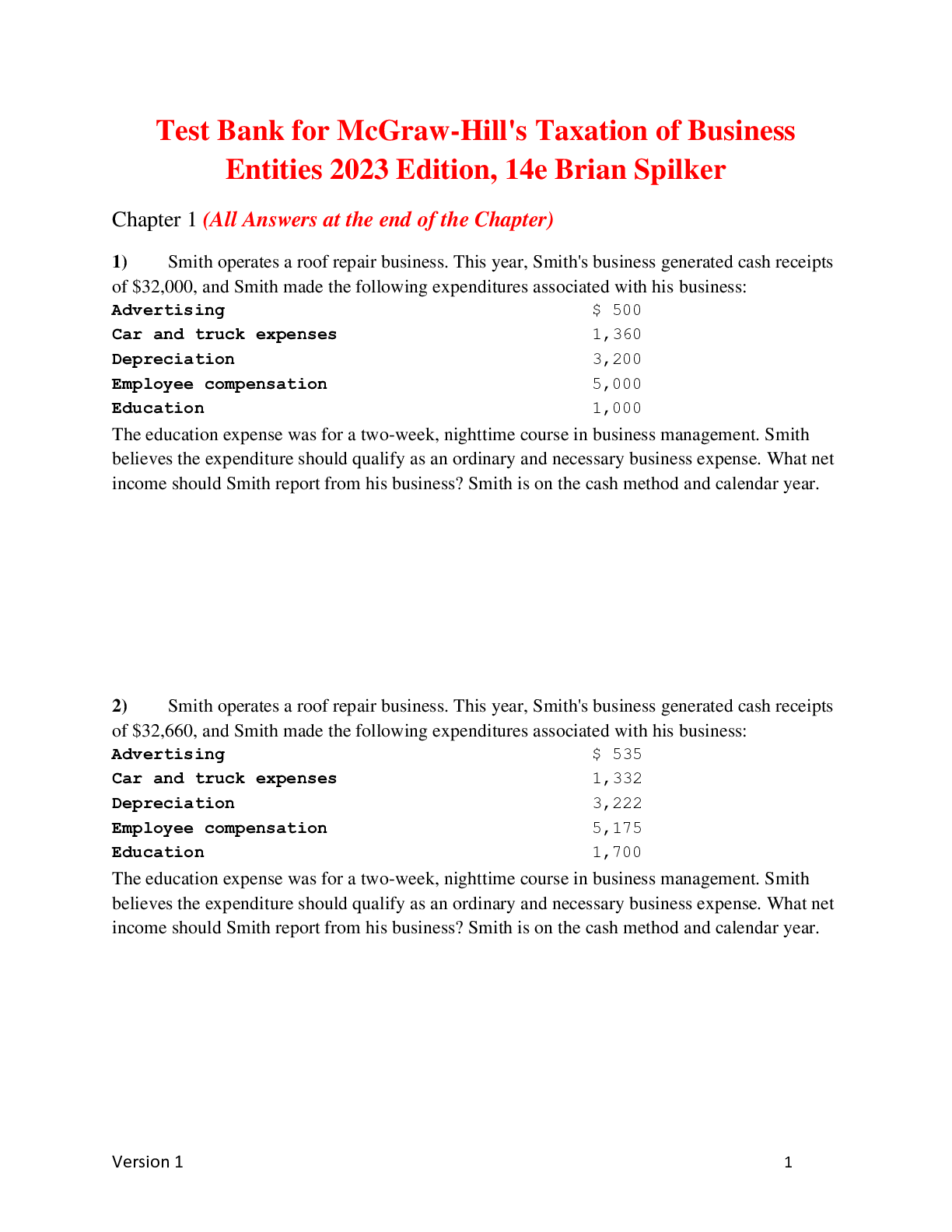

McGraw-Hill's Taxation of Business Entities 2023 Edition, 14e...

$22

374 Pages

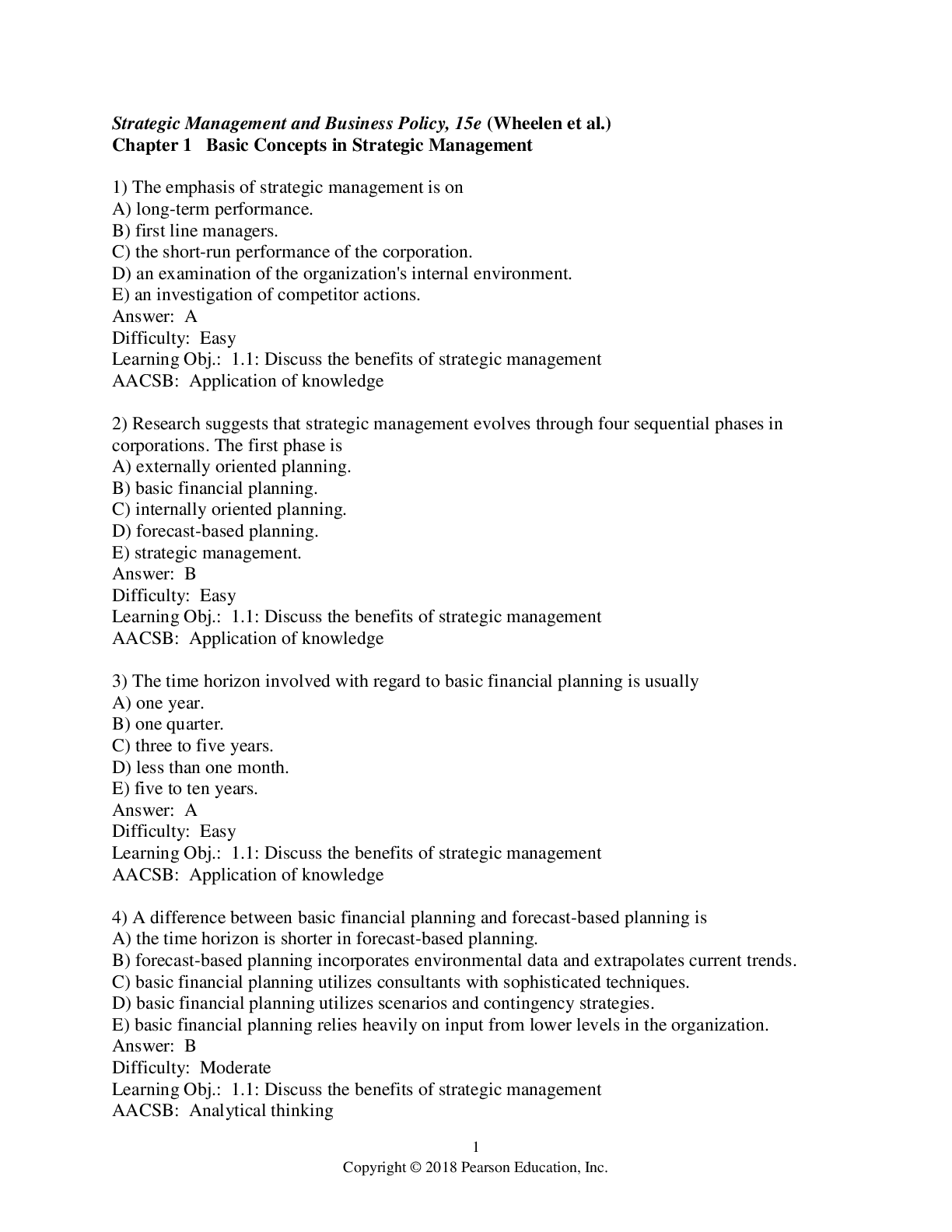

Concepts in Strategic Management and Business Policy Globaliza...

$32

2186 Pages

Business Law 17th Edition Langvardt Test Bank.Answers and chea...

$25

61 Pages

Business Ethics 5th Edition Crane, Matten, Glozer, Spence | Te...

More related documents below