ECO 202 – FINAL TEST. 35 Questions and Answers. 100% Pass rate.

Document Content and Description Below

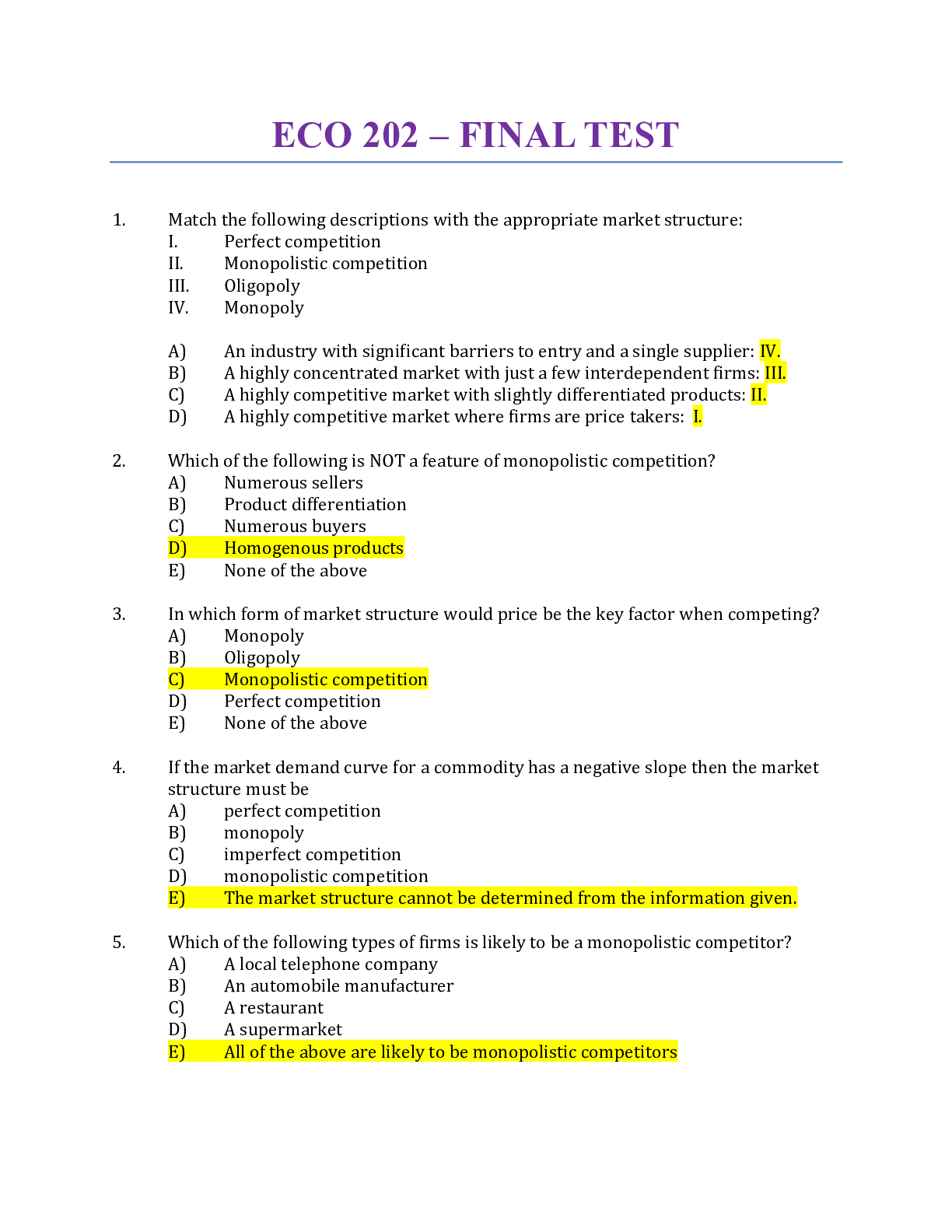

ECO 202 – FINAL TEST 1. Match the following descriptions with the appropriate market structure: I. Perfect competition II. Monopolistic competition III. Oligopoly IV. Monopoly A) An ... industry with significant barriers to entry and a single supplier: IV. B) A highly concentrated market with just a few interdependent firms: III. C) A highly competitive market with slightly differentiated products: II. D) A highly competitive market where firms are price takers: I. 2. Which of the following is NOT a feature of monopolistic competition? A) Numerous sellers B) Product differentiation C) Numerous buyers D) Homogenous products E) None of the above 3. In which form of market structure would price be the key factor when competing? A) Monopoly B) Oligopoly C) Monopolistic competition D) Perfect competition E) None of the above 4. If the market demand curve for a commodity has a negative slope then the market structure must be A) perfect competition B) monopoly C) imperfect competition D) monopolistic competition E) The market structure cannot be determined from the information given. 5. Which of the following types of firms is likely to be a monopolistic competitor? A) A local telephone company B) An automobile manufacturer C) A restaurant D) A supermarket E) All of the above are likely to be monopolistic competitors 6. The fact that Pepsi uses a predominantly blue can, while Coke uses a red and white one is an example of... A) Collusion B) Product choice C) Product differentiation D) Price competition E) None of the above 7. A monopolistically competitive firm's demand curve is... A) Elastic because it has several competitors producing similar, but not identical goods B) Perfectly elastic because it has many competitors producing identical goods. C) Inelastic because it has at most no competitors producing the same good. D) None of the other choices 8. Suppose that in the short run, a monopolistically competitive industry faces P<ATC. This will cause... A) Firms to enter the industry and each firm's demand curve to shift to the right until profits are normal. B) Firms to enter the industry and each firm's demand curve to shift left, until profits are normal. C) Firms to leave the industry and each firm's demand curve to shift right until profits are restored. D) None of the other choices. 9. Which of the following is not true of an oligopoly? A) It consists of a few large firms. B) There is a mutual interdependence between firms in the oligopoly. C) Firms that are part of the oligopoly produce only a differentiated product. D) None of the above 10. Which of the following firms belong to an oligopolistic market? A) McDonald's B) Kellogg's food products C) Stelco steel D) All of the above 11. Suppose that there are six firms in an industry. Firm A has a 10% market share, firm B has a 20% market share, Firm C has a 30% market share, while firms D, E and F have market shares of 15%, 20% and 5% respectively. The Herfindahl index for this industry is A) 1500 B) 2050 C) 2500 D) 1650 E) None of the above 12. A perfectly competitive industry would have a Herfindahl index of... A) Close to 0 B) 10,000 C) 100 D) 5000 E) None of the above 13. If two oligopolistic firms agree to collusion, A) One will agree to set the product price high, while another will keep it low. B) Both firms will agree to keep the product price low. C) Both firms will agree to keep their product price high so as to maximize profits. D) Both firms will agree to try and force other firms out of business. E) None of the above 14. Which of the following is an obstacle to collusion? A) Economic slowdowns often cause the oligopoly to reduce its price. B) It is often difficult to block the entry of new firms. C) There is a temptation for firms to cheat and lower their price to increase profits. D) All of the other choices. E) None of the above 15. Non-price competition such as advertising is often more attractive to oligopolists than price wars because... A) Developing new products and advertising makes it difficult for competing firms to imitate them. B) Firms may have a difficult time imitating price changes. C) Price changes usually provide more lasting gains than non-price competing. D) All of the other choices. E) None of the other choices. 16. If a producing firm does not have enough time to expand its plant capacity, it is: A) bankrupt. B) operating in the short run. C) operating in the long run. D) losing money. E) None of the above. 17. Economic costs of production differ from accounting costs of production in that: A) economic costs include expenditures for hired resources while accounting costs do not. B) economic costs add the opportunity cost of a firm using its own resources. C) accounting costs are always larger than economic costs. D) accounting costs include expenditures for hired resources while economic costs do not. E) None of the above. 18. An example of a long run adjustment is: A) a soybean farmer turns on the irrigation system after a month long dry spell. B) Walmart builds another Supercenter. C) your university offers Saturday morning classes next fall. D) Ford Motor Company lays off 2,000 assembly line workers. E) None of the above. 19. The reason the marginal product of labor in the short run increases at first and then falls is because: A) the management is inefficient. B) there are fewer opportunities for division of labor and specialization. C) as more labor is hired, they are not as skilled as the first ones hired. D) the extra workers have busy work piled on them. E) None of the above. 20. If 11 workers can produce a total of 54 units of a product and another worker has a marginal product of six, then the average product of 12 workers is: A) 5. B) 48. C) 54. D) 60. E) None of the above. 21. Economies of scale exist because as a firm increases its size in the long run: A) labor and management can specialize their activities more. B) as a larger input buyer the firm can purchase inputs at a lower per unit cost. C) the firm can afford more sophisticated technology in production. D) All of the above. E) None of the above. 22. In natural monopolies such as the generation of electricity, long-run average costs continue to decrease as the plant size gets larger, because: A) diseconomies of scale are very minor but economies of scale continue. B) there are no fixed costs. C) someone must have made a mistake at lower levels of output. D) diminishing returns are not present. E) None of the above. USE THE FOLLOWING GRAPH FOR PROBLEMS 23 – 25 23. In the above figure, the difference between average total costs and average variable costs is: A) fixed costs. B) average fixed costs. C) marginal costs. D) sunk costs. E) None of the above. 24. In the figure above, average variable costs approach average total costs as output rises because: A) fixed costs are falling. B) total costs are falling. C) marginal costs are above average variable costs. D) average fixed costs are falling. E) None of the above. 25. In the figure above, when marginal costs are rising: A) marginal product of labor is declining. B) average variable costs are also rising. C) average total costs are also rising. D) all of the above. E) None of the above. 26. Both individual buyers and sellers in perfect competition: A) have the market price dictated to them by government. B) have to take the market price as a given. C) can influence the market price by their own individual actions. D) can influence the market price by joining with a few of their competitors. E) None of the above. 27. If a perfectly competitive seller is producing at an output where price is $11 and the marginal cost is $14.54, then to maximize profits the firm should: A) produce a larger level of output. B) not enough information given to answer the question. C) produce a smaller level of output. D) continue producing at the current output. E) None of the above. 28. A very large number of small sellers who sell identical products implies: A) downward sloping demand for each seller’s product. B) the inability of one seller to influence price. C) a multitude of vastly different selling prices. D) chaos in the market. E) None of the above. 29. When a competitive firm finds that the market price is below its minimum average variable cost level, it will sell: A) any positive output the entrepreneur decides upon because all of it can be sold. B) nothing at all, the firm shuts down. C) the output where average total costs equal price. D) the output level where marginal revenue equals marginal cost E) None of the above. USE THE FOLLOWING GRAPH FOR PROBLEMS 30 – 35 30. At price P1, the firm in the figure above would produce: A) zero. B) Q3. C) Q5. D) Q6. E) None of the above. 31. At price P2, the firm in the above figure would produce: A) Q6. B) zero. C) Q5. D) Q1. E) None of the above. 32. At price P1, the firm in the above figure would: A) break even. B) lose more than fixed costs. C) lose less than fixed costs. D) lose fixed costs. E) None of the above. 33. At price P3, the firm in the figure above would: A) suffer a loss equal to fixed costs. B) make a profit. C) break even. D) suffer a loss less than fixed costs. E) None of the above. 34. At price P4 in the long run, the industry including the firm in the figure above would: A) cease to exist. B) have exit of some existing firms. C) have entry of new firms. D) remain the same size. E) None of the above. 35. At price P2 in the long run, the industry including the firm in the above figure would: A) cease to exists. B) have entry of new firms. C) remain the same size. D) have exit of some existing firms. E) None of the above. [Show More]

Last updated: 2 years ago

Preview 1 out of 8 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

Reviews( 0 )

$13.00

Can't find what you want? Try our AI powered Search

Document information

Connected school, study & course

About the document

Uploaded On

Jan 29, 2021

Number of pages

8

Written in

Additional information

This document has been written for:

Uploaded

Jan 29, 2021

Downloads

0

Views

83