Business > QUESTIONS & ANSWERS > AFM 274 S22 Midterm 1_Solutions (All)

AFM 274 S22 Midterm 1_Solutions

Document Content and Description Below

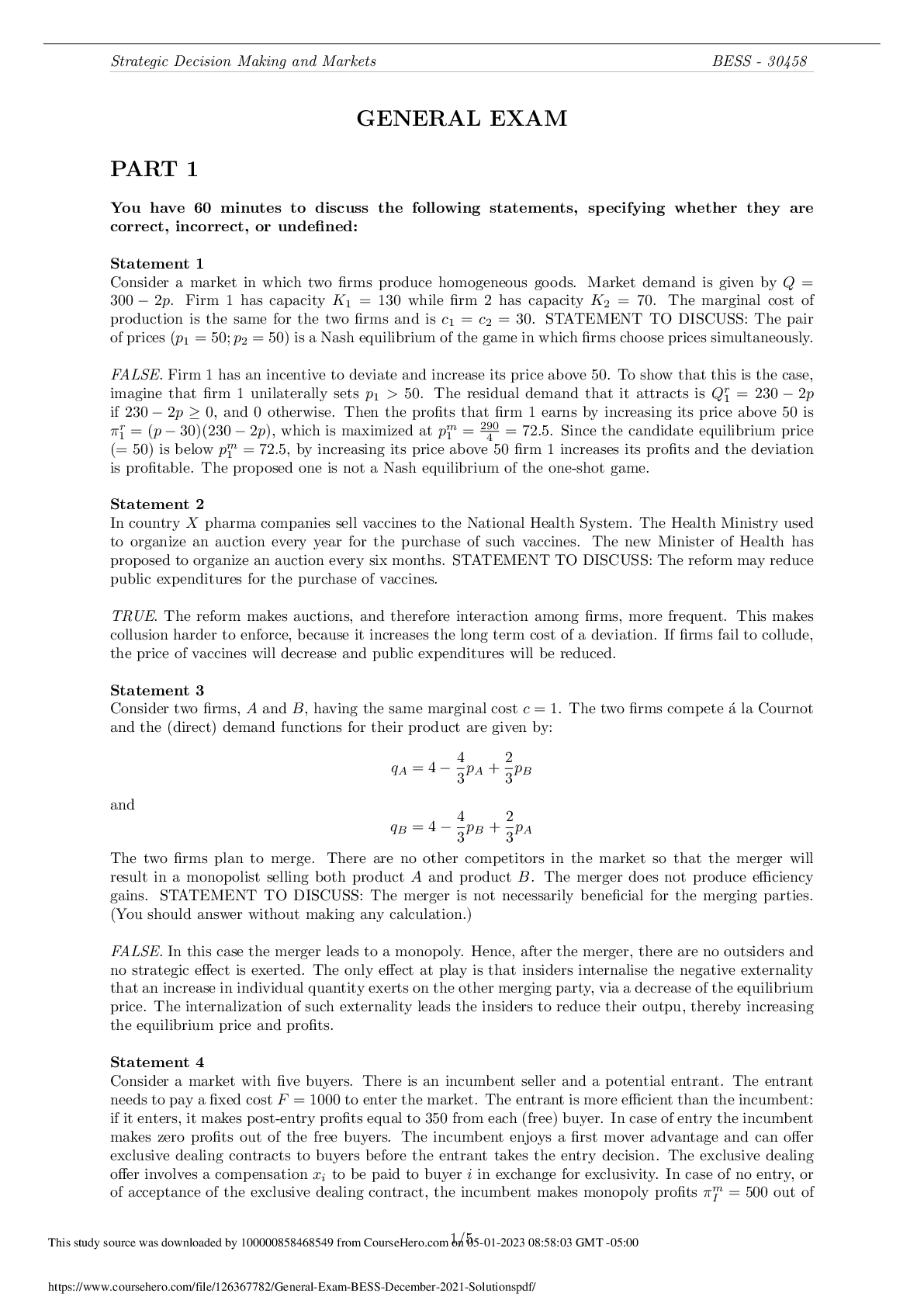

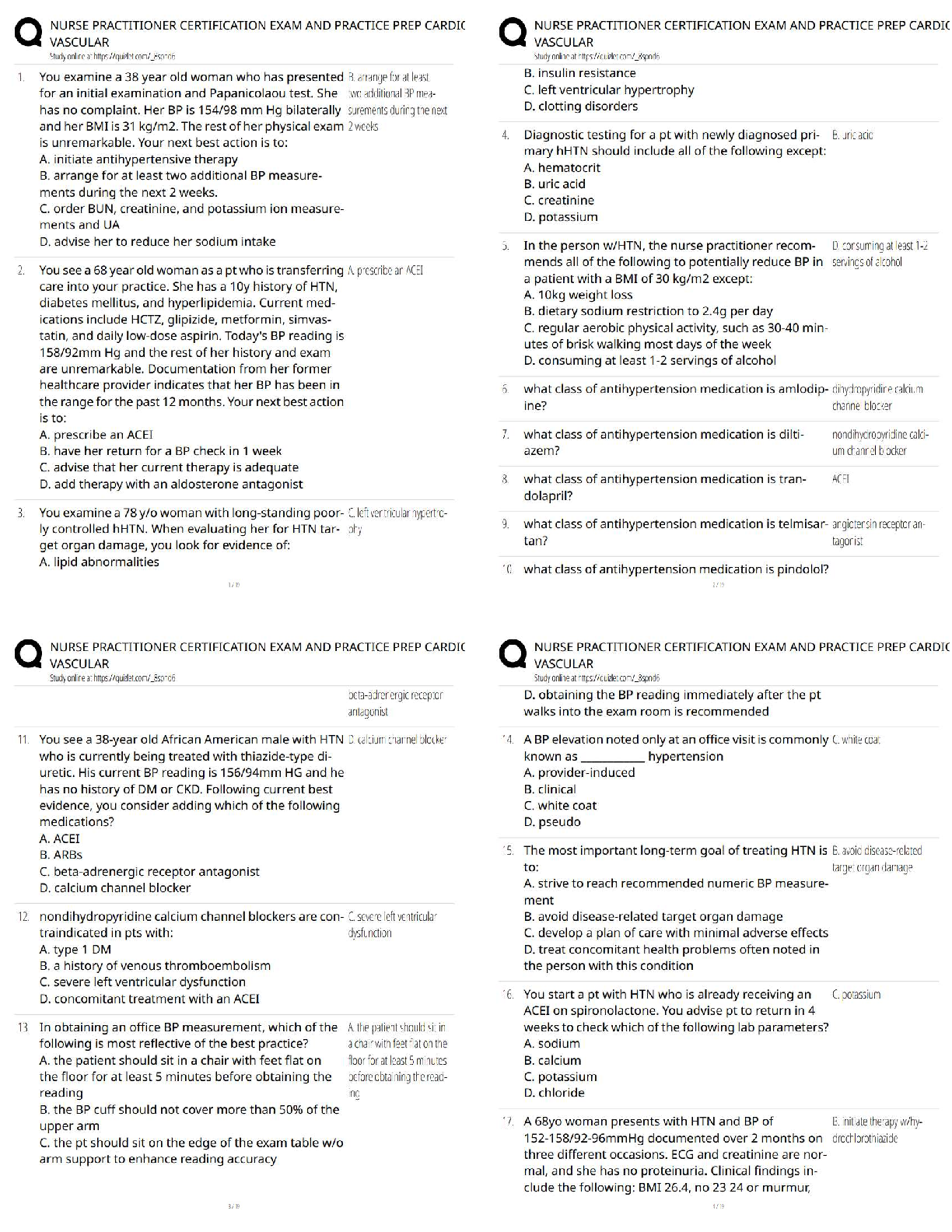

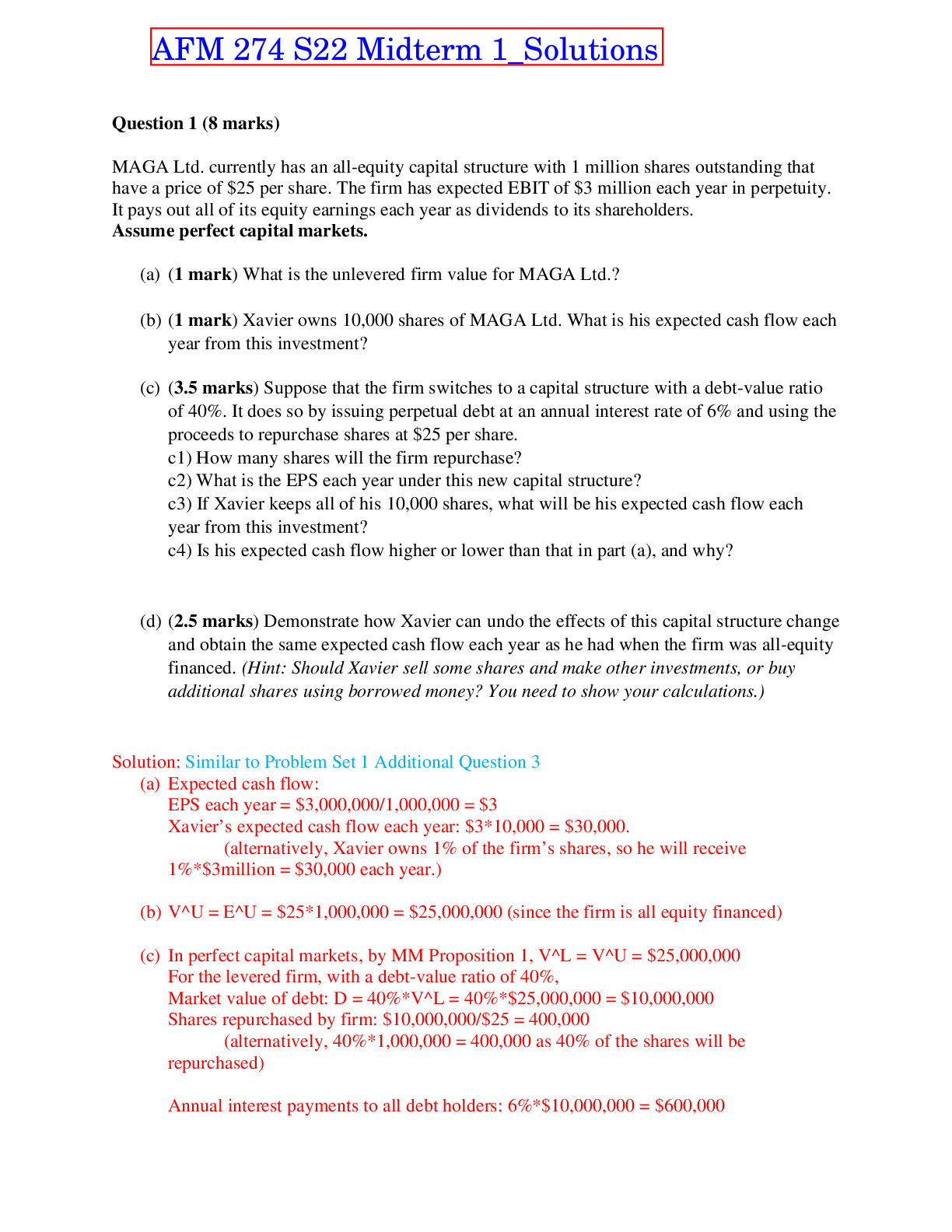

MAGA Ltd. currently has an all-equity capital structure with 1 million shares outstanding that have a price of $25 per share. The firm has expected EBIT of $3 million each year in perpetuity. It pays ... out all of its equity earnings each year as dividends to its shareholders. Assume perfect capital markets. (a) (1 mark) What is the unlevered firm value for MAGA Ltd.? (b) (1 mark) Xavier owns 10,000 shares of MAGA Ltd. What is his expected cash flow each year from this investment? (c) (3.5 marks) Suppose that the firm switches to a capital structure with a debt-value ratio of 40%. It does so by issuing perpetual debt at an annual interest rate of 6% and using the proceeds to repurchase shares at $25 per share. c1) How many shares will the firm repurchase? c2) What is the EPS each year under this new capital structure? c3) If Xavier keeps all of his 10,000 shares, what will be his expected cash flow each year from this investment? c4) Is his expected cash flow higher or lower than that in part (a), and why? (d) (2.5 marks) Demonstrate how Xavier can undo the effects of this capital structure change and obtain the same expected cash flow each year as he had when the firm was all-equity financed. (Hint: Should Xavier sell some shares and make other investments, or buy additional shares using borrowed money? You need to show your calculations.) Question 2 (10 marks) U and L are two firms which are identical in all relevant aspects except that U is unlevered whereas L has $40 million of perpetual debt on which it pays an interest rate of 5% per year. Assume that the asset cost of capital for U is 10%, and that the expected perpetual EBIT for each firm is $10 million per year. For part (a) and (b), assume perfect capital markets without taxes. (a) (1.5 marks) What is the equity value for the two firms U and L? (b) (1.5 marks) Suppose that firm U has the same equity value as you calculated in part (a), but firm L has equity value that is $10 million lower than what you calculated in part (b). Briefly explain how you can make an arbitrage profit by filling up the following sentence: _______ firm L’s equity, ________ firm L’s debt, and simultaneously ________ firm U’s equity. (For each blank, choose one of the two words: “sell” or “buy”.) For part (c) and (d), assume each firm faces a corporate tax rate of 20%, but capital markets are otherwise perfect and efficient. (c) (2 marks) Calculate the firm value for both U and L. (d) Suppose firm U’s management team decides to do a leveraged recapitalization to capture the interest tax shields. Originally firm U has 11 million shares outstanding, now it announces to switch to L by issuing $40 million of perpetual debt to buy back shares. (i) (3 marks) Prepare the firm’s market value balance sheet immediately after the debt is issued but before the shares are repurchased.(2 marks) What will be the firm’s share price just before the repurchase? How (ii) many shares will be repurchased? Question 3 (6 marks) Blunt Instruments Ltd. has a market value debt-equity ratio of 1, which it plans to maintain in the future. The market value of the firm’s equity is $50 million. The firm pays an annual interest rate of 8% on its debt. It is expected to have free cash flows of $8,000,000 after one year. This amount is forecasted to grow at 2% per year forever. The firm faces a corporate tax rate of 50%, but capital markets are otherwise perfect. (a) (2 marks) What is the firm’s weighted average cost of capital? (b) (2 marks) What is the firm’s pretax WACC? (c) (2 marks) What is the present value of the firm’s interest tax shield? Question 4 (7 marks) TwoBee Corp. is currently all-equity financed. It announces that it is going to launch a special product that can change its total assets at the end of the year to $150 million if the new project succeeds (with a probability of 60%) or $80 million if it fails (with a probability of 40%). TwoBee has 1 million shares outstanding at the start of the year. Assume that present values can be calculated using a discount rate of 5% per year for all investors of the firm. (a) (2 marks) How much is TwoBee’s equity worth in millions at the start of the year? What is its share price? (Keep two decimal places.) (b) (3 marks) Now suppose TwoBee decides to have leverage by issuing a zero-coupon bond with a $100 million face value due exactly one year from today and uses the proceeds to repurchase shares. Suppose in the event of default, TwoBee’s assets will decrease by $20 million due to financial distress costs. Assume efficient markets except for financial distress costs. b1) What is the market value of the bond today? b2) What is the value of TwoBee’s equity immediately after the debt issuance? b3) How many shares are repurchased? (c) (2 marks) Determine who bears the bankruptcy costs, equity holders or debt holders? (Hint: Compare the share price in (a) and the share price in (b)) Question 5 (4 marks) Suppose SAF Inc. has debt outstanding of $20 million which is due after one year, and all its assets (including cash) have a market value of 0. In an attempt to save the firm, SAF is considering an investment project which costs $50 million today and returns a payoff of $80 million after one year or a payoff of $60 million after one year, with the probability of 50% and 50%, respectively. SAF is considering raising $50 million by issuing new equity to finance this project. Assume that present values can be calculated by discounting expected payoffs at the discount rate of 10% per year. Also assume perfect capital markets. (a) (2 marks) Calculate the net present value of this project. Should the firm take this project? (b) (2 marks) What is the net present value to new shareholders? Would new shareholders finance this project? Would debt holders agree with the new shareholders? Question 6 (6 marks) Assess whether the statement is true or false. Justify your answer. All marks are based on the quality of your argument supporting your answer. (a) (2 marks) Firms in the Information Technology sector should, on average, have a higher debt-equity ratio than those in the Utilities sector. (b) (2 marks) In a perfect capital market, holding everything else constant, expected return of equity decreases when the risk of debt increases. (c) (2 marks) If there is adverse selection in the market, internal capital can be cheaper than external sources of funds Question 7: Multiple choice questions (9 marks) Choose only the MOST correct answer. There are 6 multiple choice problems spanning two pages. IMPORTANT: Answer all MCQ’s on the BUBBLE SHEET provided. Make sure that the entire bubble is filled in. You may circle the correct answer for each question on your exam paper, however you must transfer these to the bubble sheet for marking. 1. (1.5 marks) Which of the following statements is true? A. Firms with more free cash flows should decrease leverage to control management incentives. B. When a firm faces financial distress, shareholders might not want to invest and might want to withdraw money from the firm if possible. C. An over-investment problem occurs when shareholders have an incentive to invest in risky positive-NPV projects. D. The debt-overhang problem refers to the problem wherein there is such much debt that share-holders take on negative-NPV projects to exploit debt holders. 2. (1.5 marks) Which of the following statements is false? A. When a firm faces financial distress, creditors can gain by making sufficiently risky investments, even if they have negative NPV. B. When a firm has leverage, a conflict of interest exists if investment decisions have different consequences for the value of equity and the value of debt. C. In some circumstances, managers may take actions that benefit shareholders but harm the firm’s creditors and lower the total value of the firm. D. Agency costs are costs that arise when there are conflicts of interest between stakeholders. 3. (1.5 marks) The reason that MM Proposition I needs to be modified in the presence of corporate taxation is because: A. Levered firms pay less taxes compared with identical unlevered firms. B. Bondholders require higher rates of return compared with stockholders. C. Earnings per share are no longer relevant with taxes. D. The risk of equity changes as the debt ratio goes up. 4. (1.5 marks) ???? = ?? ??+?? ???? + ?? ??+?? ???? The term ???? in the equation is: A. the same as the beta of the firm’s assets. B. the required return on the firm’s equity. C. equal to zero if the firm’s equity is riskless. D. the proportion of the firm financed with equity. 5. (1.5 marks) Which of the following statements is false? A. Creditors often place restrictions on the actions that the firm can take. Such restrictions are referred to as debt covenants. B. Covenants are often designed to prevent management from exploiting debt holders, so they may help to reduce agency costs. C. Agency costs are smallest for long-term debt. D. Covenants may limit the firm’s ability to pay large dividends or the types of investments that the firm can make. 6. (1.5 marks) Assume that capital markets are perfect. When a firm increases its leverage, the WACC does not change and is the same as unlevered cost of capital (????) because: A. Cost of debt is often higher than cost of equity. B. Cost of debt and cost of equity are the same. C. When firms borrow more, cost of equity increases but cost of debt decreases, so the two effects offset each other. D. Even though cost of debt and cost of equity both rise when leverage is high, more weight is put on the lower-cost debt; the savings from the low cost of debt are exactly offset by a higher cost of equity. [Show More]

Last updated: 2 years ago

Preview 1 out of 9 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

Reviews( 0 )

$9.50

Can't find what you want? Try our AI powered Search

Document information

Connected school, study & course

About the document

Uploaded On

Apr 20, 2023

Number of pages

9

Written in

All

Additional information

This document has been written for:

Uploaded

Apr 20, 2023

Downloads

0

Views

80