FIN 421 Assignment 2

Assignment 2 - FIN 421 - Spring 2021_Data.xlsx

In this assignment you will apply mean variance analysis for an asset allocation decision.

Mean Variance Analysis in Practice

Assume you are a p

...

FIN 421 Assignment 2

Assignment 2 - FIN 421 - Spring 2021_Data.xlsx

In this assignment you will apply mean variance analysis for an asset allocation decision.

Mean Variance Analysis in Practice

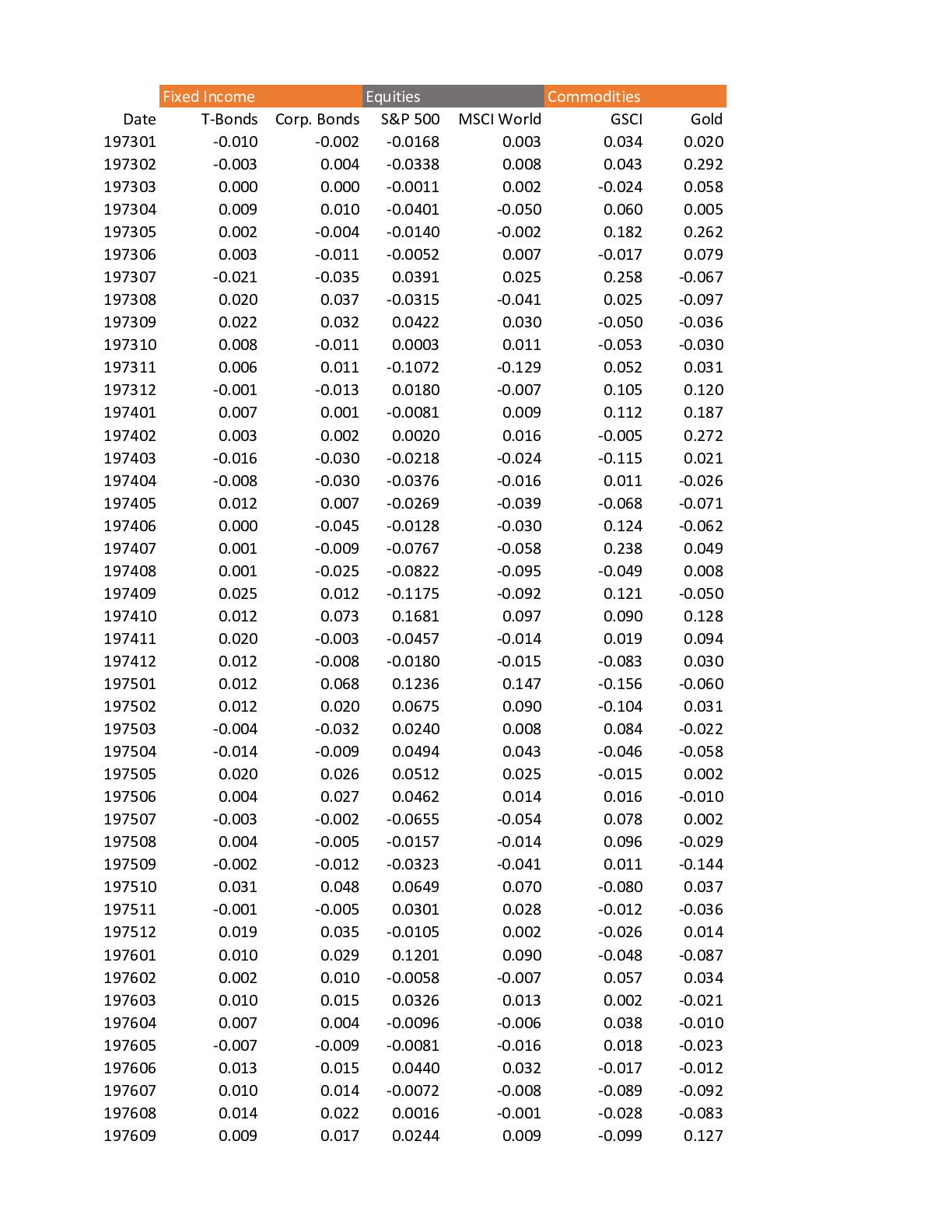

Assume you are a portfolio manager for a large pension fund and in charge of allocating funds across major asset classes. Specifically, today is 12/31/2014 and you are assembling a portfolio for January of 2015. Your investment universe consists of T-bonds (Barclays U.S. Treasury index), investment grade corporate bonds (Barclays U.S. Corp index), domestic stocks (S&P 500), international stocks (MSCI World index), commodities (Goldman Sachs Commodity In- dex), and gold. Asset allocation decisions are made based on mean variance analysis.

On Canvas, you will find an Excel file containing historical monthly net returns for these assets. Assume that the risk-free rate for 1/2015 equals 25 basis points per month.

QUESTIONS:

A Report the mean and variance-covariance matrix for all assets.

B Based on the moments you estimated in A, find the tangency portfolio and the minimum variance portfolio. Report the mean, standard deviation, and portfolio weights for both portfolios.

C Compute the optimal share invested in risky assets for an investor with the utility function U = μ − ασ2 and values for risk aversion, α, between 10 and 40.1 Plot the optimal risky asset share as a function of α. Is the function increasing or decreasing? Explain economically why you find the slope that you do.

D Plot the frontier of risky assets. To do so, use the minimum variance portfolio and the tangency portfolio found above, along with the two fund separation property. Use weights between -25 and 15 on the minimum variance portfolio (i.e. -2500% to 1500%). Add the individual assets as ’dots’ to the plot.

E Suppose you form a portfolio that invests in both the minimum variance portfolio and the tangency portfolio. If the weight on the minimum variance portfolio equals 40%, what are the weights on the individual assets (T-bonds, corporate bonds, etc.)?

1Start by computing the optimal share in risky assets for a value of α = 10. Repeat for α = 11, α = 12 etc.

[Show More]

.png)

midterm help.png)