healthcare > EXAM > LO 3: Briefly describe the differences between FSA, HRA and HSA tax advantaged accounts,100% CORRECT (All)

LO 3: Briefly describe the differences between FSA, HRA and HSA tax advantaged accounts,100% CORRECT

Document Content and Description Below

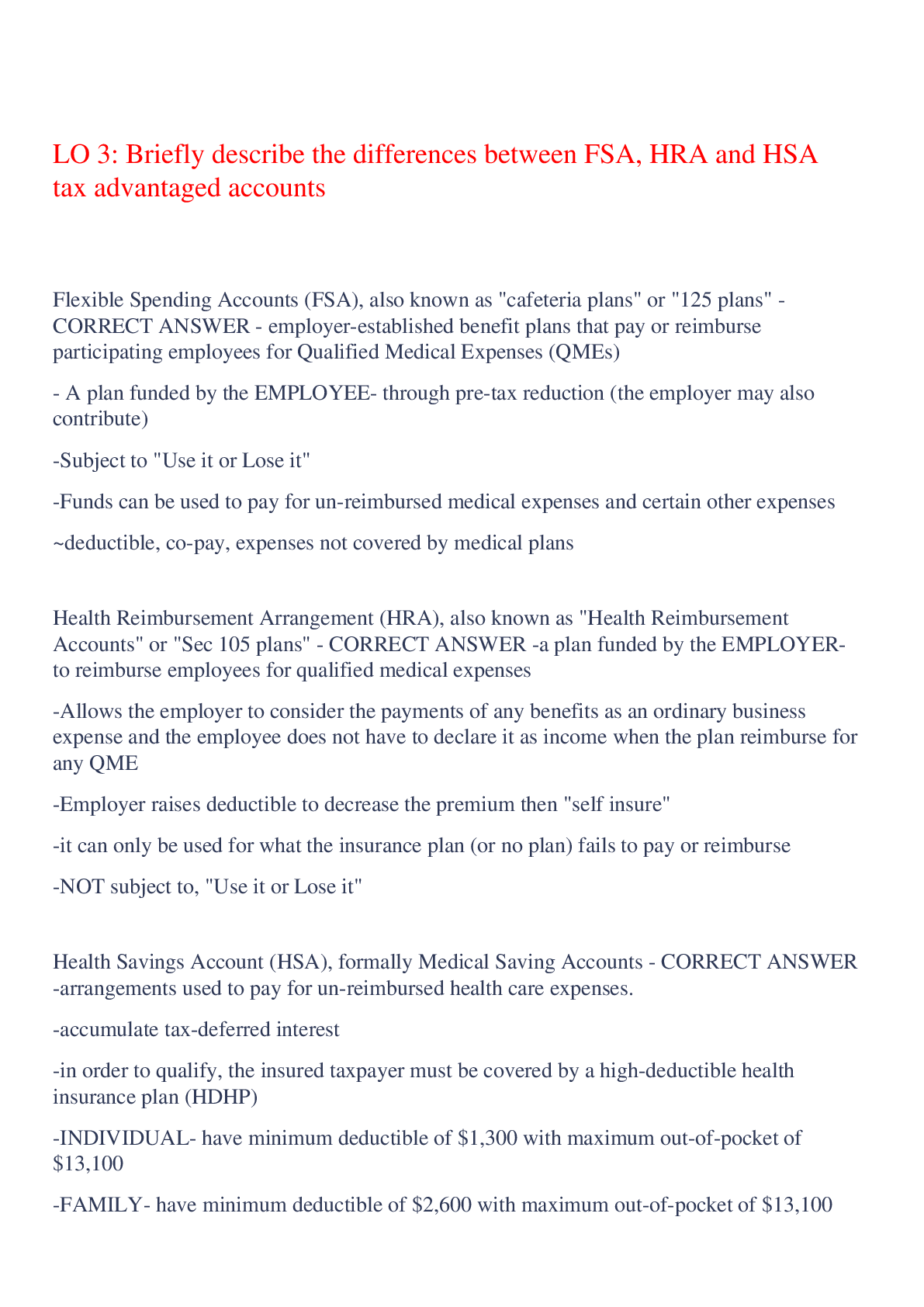

LO 3: Briefly describe the differences between FSA, HRA and HSA tax advantaged accounts Flexible Spending Accounts (FSA), also known as "cafeteria plans" or "125 plans" - CORRECT ANSWER - employe ... r-established benefit plans that pay or reimburse participating employees for Qualified Medical Expenses (QMEs) - A plan funded by the EMPLOYEE- through pre-tax reduction (the employer may also contribute) -Subject to "Use it or Lose it" -Funds can be used to pay for un-reimbursed medical expenses and certain other expenses ~deductible, co-pay, expenses not covered by medical plans Health Reimbursement Arrangement (HRA), also known as "Health Reimbursement Accounts" or "Sec 105 plans" - CORRECT ANSWER -a plan funded by the EMPLOYER- to reimburse employees for qualified medical expenses -Allows the employer to consider the payments of any benefits as an ordinary business expense and the employee does not have to declare it as income when the plan reimburse for any QME -Employer raises deductible to decrease the premium then "self insure" -it can only be used for what the insurance plan (or no plan) fails to pay or reimburse -NOT subject to, "Use it or Lose it" Health Savings Account (HSA), formally Medical Saving Accounts - CORRECT ANSWER -arrangements used to pay for un-reimbursed health care expenses. -accumulate tax-deferred interest -in order to qualify, the insured taxpayer must be covered by a high-deductible health insurance plan (HDHP) -INDIVIDUAL- have minimum deductible of $1,300 with maximum out-of-pocket of $13,100 -FAMILY- have minimum deductible of $2,600 with maximum out-of-pocket of $13,100 -Not subject to "Use it or Lose it" -Fund can accumulate earnings, which are not taxed unless funds are used for non-medical expenses -allows the account holder the flexibility of choosing their own medical providers -Does not require the employer to provide a plan Effective date: FSA - CORRECT ANSWER -January 1, 1979 Effective date: HSA - CORRECT ANSWER -January 1, 1996 Effective date: HRA - CORRECT ANSWER -June 26, 2002 Eligibility: FSA - CORRECT ANSWER -All Employees Eligibility: HSA - CORRECT ANSWER -Anyone who is not otherwise covered by a medical expense health insurance plan -Must be covered by high-deductible health insurance plan in order to open account and make deposits in the HSA: once no longer covered by HDHP no more deposits can be made Eligibility: HRA - CORRECT ANSWER All employees QME :FSA - CORRECT ANSWER Un-reimbursed medical care expenses such as deductibles, co-pay, and expenses not covered by medical plans QME: HSA - CORRECT ANSWER -Un-reimbursed medical care expenses such as deductibles, co-pay, and expenses not covered by medical plans -Health insurance premiums under a continuation of coverage arrangement (such as COBRA) -Health insurance premiums when receiving unemployment compensation -Qualified long-term care insurance premiums QME: HRA - CORRECT ANSWER Un-reimbursed medical care expenses such as deductibles, co-pay, and expenses not covered by medical plans Non-QMEs: FSA - CORRECT ANSWER -Health insurance premiums under a continuation of coverage arrangement (such as COBRA) -Health insurance premiums when receiving unemployment compensation -Qualified long-term care insurance premiums Must be covered by a health plan? FSA - CORRECT ANSWER no Must be covered by a health plan? HSA - CORRECT ANSWER yes Must be covered by a health plan? HRA - CORRECT ANSWER no Contributor: FSA - CORRECT ANSWER employee, employer, or both Contributor: HSA - CORRECT ANSWER Employee, Employer, or both Contributor: HRA - CORRECT ANSWER Employer only Contribution limits: FSA - CORRECT ANSWER Annual limits may be set by employer, but a maximum is established each year by the IRS Contribution limits: HSA - CORRECT ANSWER Contributions are not requires- if made, the maximum is a statutory limit set by the Fed. Gov. each year Can funds be carried over to next year: FSA - CORRECT ANSWER up to $500 can be carried over Can funds be carried over to next year: HSA - CORRECT ANSWER yes Can funds be carried over to next year: HRA - CORRECT ANSWER yes; at employer discretion Portability: FSA - CORRECT ANSWER account cannot be maintained if the employer is no longer working for the employer Portability:HSA - CORRECT ANSWER -Continued access to unused account balance if the employee is no longer is working there -withdrawals for non-medical purposes are subject to income tax and a 20% penalty tax -Once the account holder reaches age 65, becomes disabled, or dies, withdrawals for non-medical purposes are subject to income tax only with no penalty Portability:HRA - CORRECT ANSWER at employer discrection [Show More]

Last updated: 2 years ago

Preview 1 out of 4 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

Reviews( 0 )

$7.50

Can't find what you want? Try our AI powered Search

Document information

Connected school, study & course

About the document

Uploaded On

Aug 27, 2023

Number of pages

4

Written in

All

Additional information

This document has been written for:

Uploaded

Aug 27, 2023

Downloads

0

Views

62