TAX 655: Final Exam

Notes

Complete the problems as presented in this document. You may create a new document and/or spreadsheet as needed. Any memo should be no more than 3 pages in length. Please state any assumptions

...

TAX 655: Final Exam

Notes

Complete the problems as presented in this document. You may create a new document and/or spreadsheet as needed. Any memo should be no more than 3 pages in length. Please state any assumptions used if problems are not clear.

Problem 1

Your client, a physician, recently purchased a yacht on which he flies a pennant with a medical emblem on it. He recently informed you that he purchased the yacht and flies the pennant to advertise his occupation and thus attract new patients. He has asked you if he may deduct as ordinary and necessary business expenses the costs of insuring and maintaining the yacht. In search of an answer, consult RIA’s CHECKPOINT TAX available on-line through the SNHU Shapiro Library. Explain the steps taken to find your answer.

Step one to find my answer would be when search RIA’s Checkpoint tax is to look for information under yachts and advertising expenses. I also would look under IRC section to look up what section qualifies to help answer this questions. With this I would find out it is IRC section 162. Also with looking under yachts I find out there was a similarly case in 1961 about a yacht. To look for IRC Section 162 I would look under Find Federal Code & Regs and section for 162, which would come up and be the trade or business expense under the internal revenue code. To look up the case I would look under find case and search for 36 TC 879.

In IRC section 162 expense are deductible when they are “ordinary and necessary” for conducting a trade or business. While advertising might be considered a legitimate expense for many businesses deducting the cost of insurance or maintenance of a yacht merely because fly, a pennant with a medical emblem would not be considered ordinary and necessary.

The court case Robert Lee Henry 36 TC 879 he tried to deduct the cost of insuring and maintain a yacht on which he flew a pennant with the numerals 1040. In this case, he was found that these expenses were not deductible.

Problem 2

Stacey Small has a small salon that she has run for a few years as a sole proprietorship. The proprietorship uses the cash method of accounting and the calendar year as its tax year. Stacey needs additional capital for expansion and knows two people who might be interested in investing. One would like to practice hairdressing in the salon. The other would only invest.

Stacey wants to know the tax consequences of incorporating the business. Her business assets include a building, equipment, accounts receivable, and cash. Liabilities include a mortgage on the building and a few accounts payable, which are deductible when paid.

Write a memo to Stacey explaining the tax consequences of the incorporation. As part of your memo, examine the possibility of having the corporation issue common, preferred stock, and debt for the shareholders’ property and money.

Date: January 26, 2015 From: Courtney Dobek

Re: Tax Consequences of the Incorporation

Facts:

Stacey small has a small salon that she has been running for a few years now as a sole proprietorship. The proprietorship uses the cash method of accounting and the calendar year as its tax year. Stacey needs addition capital for expansion and knows two people who might be interest in investing. One would like to practice hair dressing in the salon. The other would only invest. Her business assets include building, equipment, accounts receivable, and cash.

Liabilities include a mortgage on the building and a few accounts payable, which are deductible when paid.

Issues:

Issues are tax advantages and disadvantages of incorporating. Another thing is the business forms what type should she take on. In addition, should she possibly adopt a check the box regulation means that C corporation tax treatment is not limited to the incorporated entities?

Applicable Law:

Section 351 (a) provides that transferors recognize no gain or loss when they transfer property t a corporation solely in exchange for the corporation’s stock provided that immediately after the exchange the transferors are in control of the corporation. This section does not apply to a transfer of property to an investment company nor does it apply in certain bankruptcy cases.

Section 351 does not define the term property but the courts and the IRS have defined property to include cash and almost any other asset. The specific requirements for deferral of gain and loss under section 351 as are the transferors must transfer property to the corporation. They must receive stock of the transferee corporation in exchange for their property. They must be in control of the corporation immediately after the exchange. Under section, 3541 transferors who exchange property solely for transferred corporation stock recognize no gain or loss if they control the corporation immediately after the exchange. Section 1244 permits an ordinary loss to be claimed on the sale exchange or worthlessness of the stock. IF a corporation issues sec, 1244 stock for property whose adjusted basis exceeds it Fair Market Value immediately before the exchange the stock basis is reduced to the property is Fair Market Value for the purpose of determine the ordinary loss amount. Section 1244 permits a shareholder to claim an ordinary loss if qualifying stock issued by a small business corporation is sold or exchange or becomes worthless. This treatment is available only to an individual who was issued the qualifying stock or who was a partner in a partnership at the time the partnership acquired the qualifying stock.

Analysis:

Stacey with a corporate formation that she receives stock only is nontaxable. She will recognize no gain or loss on the asset transfer. The transfer of property by either of the new investors should be properly timed since nontaxable transfer to existing corporations are difficult to accomplish because they need meet the 80% control requirement. The depreciation of the building and equipment recapture potential carries over from the proprietorship to the corporation. Depreciation for the year of transfer should be divided between Stacey and corporation. The income from collecting the accounts receivable and accounts payable items that represent deductibles expense will be reported by the corporation. The income is recognized when the corporation collects the receivables. The expenses are deducted then the corporations pay the liability. Some options for Stacey are to go with an S corporation or C corporation. With the C corporations, she will have a tax savings of 75,000 of corporate taxable income but this could lead to double taxation if the earnings are distributed as dividends even though the dividends will be tax at the applicable capital gain rate. The s corporation election will permit all the earnings to be taxes at the individual tax rate and avoid the possibility of double taxation. If Stacey chooses to go with C Corporation, she would be permitted to exclude 50-100% of the gain recognized on the sale or exchange of qualified small business corporation stock that has been held for more than five years. Common stock may be attractive to individuals who desire to be active in the business. Preferred stock could provide a guaranteed dividend payment for the investor. With preferred stock, Stacey needs to be carefully if she takes on S corporation because this may prevent an S corporation election. The use of debt will permit the payments of a deductible interest payment to the debt holder. The receipt of debt as part of the incorporation

transaction will trigger the recognition of part or all of the transferors realized gain. The use of debt will permit the repayment to be partially or totally, nontaxable unlike stock, which need not be retired debt usually, is retied at a maturity date. She should consider whether she should transfer the building and equipment to the corporation as part of the incorporation transaction.

This comes with advantages with Stacey retain title to the property and leasing it to the corporation also prevents the possible taking of the property by the corporations creditors if financial difficulties were to come about.

Conclusion:

Stacey will be able to keep the same tax year plan has she now with using the calendar year as the corporations tax year since there appears to be little advantage of her changing the tax year. She will also continue the cash method of accounting as the hair salons overall method of accounting because of its simplicity. In addition, she will use the same depreciation method and convention once she has transferred the building and equipment to the corporation. She should looking into her salary and make sure it is reasonable. The employment taxes paid on the salary are about the same as the self-employment tax liability incurred with the sole proprietorship. She should also look into retirement plan such has making deductible contributions to an IRA or perhaps even establish a qualified plan if she makes the S corporation election. A simple Capital structure for Stacey to use is to have solely common stock issued to her and either of the other individuals who are interested in investing in the business. Stacey could prefer to issue preferred stock or debt to the individuals who are interested only investing in the business. Even If she went, the LLC route they can be taxes as a C corporation under the check the box regulations.

This could provide greater flexibility for selecting the business entity form.

Problem 3

Five years ago, Lacey, Kaylee, and Doug organized a software corporation, DLK, which develops and sells Online Meetings software for businesses. DLK is a C corporation. Each individual contributed $10,000 to the company in exchange for 1,000 shares of DLK stock (for 3,000 shares). The corporation also borrowed $250,000 from ACME Venture Capital to finance operating costs and capital expenditures.

Because of intense competition, DLK struggled for the first few years of operation and the corporation sustained chronic losses. This year, Lacey, DLK’s president, decided to seek additional funds to finance DLK’s working capital.

CME declined to extend additional funds because of the money already invested in DLK. High Tech Venture Capital Inc. proposed to lend DLK $100,000, but at a 10% premium over the prime rate. (Other software manufacturers in the same market can borrow at a 3% premium.) First Round Capital proposed to invest $50,000 of equity capital into DLK, but on the condition that the investment firm be granted the right to elect five members to DLK’s board of directors.

Discouraged by the “high cost” of external borrowing, Lacey decides to approach Kaylee and Doug.

Lacey suggests to Kaylee and Doug that each of the three original investors contribute an additional $25,000 to DLK in exchange for five 20-year debentures. The debentures will be unsecured and subordinate to ACME’s debt. Annual interest on the debentures will accrue at a floating 5% premium over the prime rate. The right to receive interest payments will be cumulative; that is each debenture holder is entitled to past and current interest payments before DLK’s board can declare a common stock dividend. The debentures would be both nontransferable and noncallable. Lacey, Kaylee and Doug have asked you, their tax accountant, to advise them on the tax implications of the proposed financing agreement. After researching the issue, issue your advice in a tax research memo. At a minimum, you should consult the following authorities:

• IRC. Sec 385

• Rudolph A. Hardman, 60 AFTR 2d 87-5651, 82-7 USTC ¶9523 (9th Cir., 1987)

• Tomlinson v. The 1661 Corporation, 19 AFTR 2d 1413, 67-1 USTC ¶9438 (5th Cir., 1967)

Date: January 26, 2015 From: Courtney Dobek Re: Tax implications

Facts:

Lacey, Kaylee, and Doug organized a software corporation DLK. DLK is a C corporation. Each of the individuals contributed 10,000 to the company in exchange for 1000 shares of DLK stock. They also borrowed 250,000 forms ACME Venture Capital to finance operating costs and capital expenditures. CME declined to extend addition funds. High tech Venture capital proposed to lend DLK 100,000 but at 10% premium over the prime rate. First round capital proposed to invest 50,000 of equity capital into DLK but on the condition that the investment firm be granted the right to elect five members to DLK board of directors. Lacey suggest that each of the three original investors contribute an additional 25,000 to DLK in exchange for five 20-year debentures. Debentures will be unsecured and subordinate to ACME debt. Annual interest on the debentures will accrue at a floating 5% premium over the prime rate. The right to receive interest payments will be cumulative that is each debenture holder is entitled to past and current interest payments before DLK board can declare a common stock dividend. The debentures would be both nontransferable and noncallable.

Issue:

Will the advance be characterized as equity instead of debt? Will the unavailability of alternative financing at reasonable rates be significant in any decision to re characterized?

Applicable Law:

IRC section 385 the secretary is authorized to prescribe such regulations as may be necessary or appropriate to determine whether an interest in corporation is to be treated for purposes of this title as stock or indebtedness. The factors that should be taking into consideration in determining with respect to a particular factual situation whether a debt creditor relationship exists or a corporation shareholder relationship exists. The factors are:

1.) Whether there is a written unconditional promise to pay on demand or on a specified date a sum certain in money in return for an adequate consideration in money or moneys with and to pay a fixed rate of interest.

2.) Whether this is subordination to or preference over any indebtedness of the corporation. 3.) The ratio of debt to equation of the corporation

4.) Whether there is convertibility into the stock of the corporation.

5.) The relationship between holdings of stock in the corporation and holdings of the interest in question.

There was a Case Tomlinson v. The 1661 Corporation, 19 AFTR 2d 1413, 67-1 USTC ¶9438 (5th Cir., 1967) the corporation tried to procure financing from outside lender but because of prohibitive interest rates. The advances were represented by promissory notes bearing interest at 7% per annum and payable on or before 15 years after date of issuance. This was in exchange for cash advances of $138,400. This debt was subordinate to other corporate obligations. They were not entitled to pay dividends on its stock until it had paid all the past-accrued interest on the notes. The corporation had issued the notes on a pro rate basis and was thinly capitalized. The corporation on its tax return deducted interest payments on the notes but the IRS disputed this tax treatment. The IRS was arguing that based on all the facts the capital advanced by the

shareholders was equity and not debt. Payments on the securities were dividends and nondeductible.

Another case that should be noted is Rudolph A. Hardman, 60 AFTR 2d 87-5651, 82-7 USTC

¶9523 (9th Cir., 1987). In this case, the ninth circuit court of appeals cited 11 factors for distinguishing debt from equity for purposes of sec 385. These factors were:

1.) The names given to the certificates evidencing the indebtedness 2.) The presence or absence of a maturity date

3.) The source of the payments

4.) The right to enforce payments of principal and interest 5.) Participation and management

6.) A status equal to or inferior to that of regular corporate creditors 7.) The intent of the parties

8.) Thin or adequate capitalization

9.) Identify of interest between creditor and stock holder 10.) Payment of interest only out of dividend money

11.) The ability of the corporation to obtain loans from outside lending institutions

Analysis:

Based on the factors from Sec. 385 especially factors 2,3, and 5 the three investors interest in DLK are more like equity rather than debt. For DLK the in test is subordinate to other DLK

obligations. When looking at the company’s debt to equity ratio it is very high. The relationship between the interest in question and investor preexisting stockholdings is proportionate. Then when you look at the other two factors, one and four the three investor’s interest resembles debt more than equity as well. The interest is evidence by a note and it is not convertible into the DLK stock. Under the authorized that was granted by sec. 385 the treasury secretary issued regulation in 1980 but they were lasted taken away in 1983. This is why the court cases help brings a clear guidance to what needs to be done by DLK. The IRS and the two courts had re characterized the advance as equity the IRS and the courts would need to treat any interest paid to the three investors as dividends that are nondeductible by DLK. The IRS and the Courts court treat the advance as nonbusiness related stating that it was intendant to safeguard the investor’s initial equity investment. If in the case that DLK become insolvent and the three investors could not recoup the full amount of the advance that was given to them by the venture capital firms there would be treated as nonbusiness bad debt. Since the loss would be capital in character, it would be deductible only to the extent of the 3000 per year in excess of any capital gain. There would be no relief for partial losses would be afforded by the investors.

Conclusion:

In conclusion they would need make sure they under stated sec. 385 and the court cases and that there interest would paid to the investor would be treated as dividends and nondeductible by DLK. They may also treat the advance as nonbusiness related which still wouldn’t help them.

This would be intended to safeguard the investor’s initial equity investment. IF the three investors weren’t able to recoup the full amount of the advance, these losses would be treated as nonbusiness bad debt. There would be no relief for partial losses.

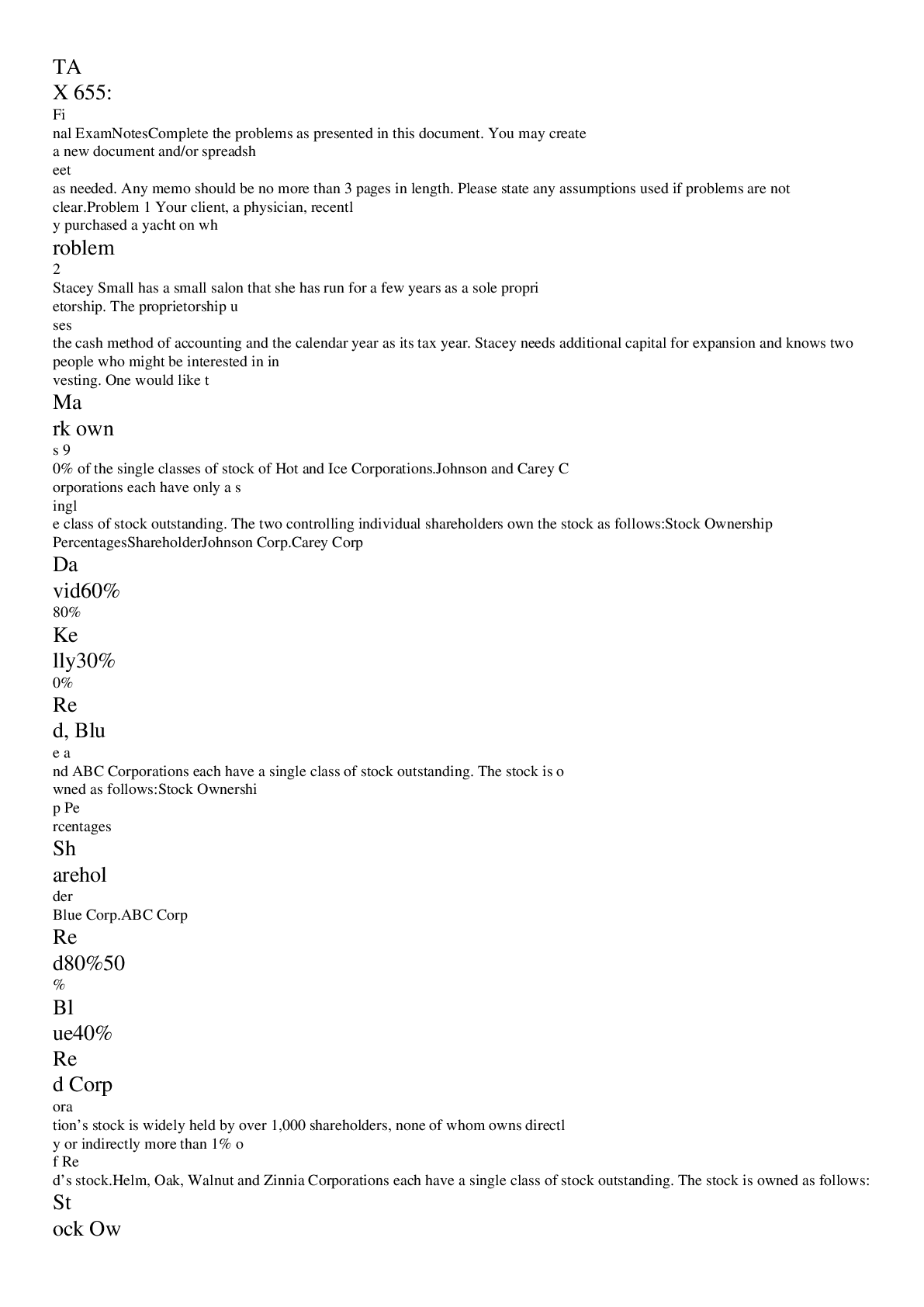

Problem 4

Which of the following groups constitute a controlled group? (Any stock not listed below is held by unrelated individuals each owning less than 1% of the outstanding stock.) For brother-sister corporations, which definition applies?

a. Mark owns 90% of the single classes of stock of Hot and Ice Corporations.

b. Johnson and Carey Corporations each have only a single class of stock outstanding. The two controlling individual shareholders own the stock as follows:

Stock Ownership Percentages

Shareholde

r Johnson Corp. Carey Corp

David 60% 80%

Kelly 30% 0%

c. Red, Blue, and ABC Corporations each have a single class of stock outstanding. The stock is owned as follows:

Stock Ownership Percentages

Shareholde

r Blue Corp. ABC Corp

Red 80% 50%

Blue 40%

Red Corporation’s stock is widely held by over 1,000 shareholders, none of whom owns directly or indirectly more than 1% of Red’s stock.

d. Helm, Oak, Walnut and Zinnia Corporations each have a single class of stock outstanding. The stock is owned as follows:

Stock Ownership Percentages

Shareholder Helm Corp. Oak Corp Walnut Corp Zinnia Corp

James 100% 90%

Helm 80% 30%

Walnut 60%

Problem 5

Eric and Denise are partners in ED Partnership. Eric owns a 60% capital, profits, and loss interest. Denise owns the remaining interest. Both materially participate in the partnership activities. At the beginning of the current year, ED’s only liabilities are $50,000 in accounts payable, which remain outstanding at year-end. In August, ED borrowed $120,000 on a nonrecourse basis from Delta Bank. The loan is secured by property with a $230,000 FMV. These are ED’s only liabilities at year-end. Basis for the partnership interest at the beginning of the year is $40,000 for Denise and $60,000 for Eric before considering the impact of liabilities and operations. ED has a $200,000 ordinary loss during the current year. How much loss can Eric and Denise recognize?

Eric Denise

Beginning without debt 42,000 28,000

Account Payable 30,000 20,000

Basis from loss 72,000 48,000

Problem 6

Linda pays $100,000 cash for Jerry’s ¼ interest in the JILL Partnership. The partnership has a Sec. 754 election effect. Just before the sale of Jerry’s interest, JILL’s balance sheet appears as follows:

Partnership’s

Basis FMV

Assets:

Cash $75,000 $75,000

Land $225,000 $325,000

Total $300,000 $400,000

Partners' capital

Jerry $75,000 $100,000

Instrument Corp $75,000 $100,000

Logo Corp $75,000 $100,000

Lighthouse Corp $75,000 $100,000

Total $300,000 $400,000

a. What is Linda’s total optional basis adjustment?

b. If JILL Partnership sells the land for its $325,000 FMV immediately after Linda purchases her interest, how much gain, or loss will the partnership recognize?

c. How much gain will Linda report because of the sale?

Problem 7

Monte and Allie each own 50% of Raider Corporation, an S corporation. Both individuals actively participate in Raider’s business. On January 1, Monte and Allie have adjusted bases for their Raider stock of $80,000 and

$90,000 respectively. During the current year, Raider reports the following results:

Ordinary loss $175,000

Tax-exempt interest income 20,000

Long-term capital loss 32,000

Raider’s balance sheet at year-end shows the following liabilities: accounts payable, $90,000; mortgage payable, $30,000; and note payable to Allie, $10,000.

a. What income and deductions will Monte and Allie report from Raider’s current year activities?

a.)

Allocation to Shareholders Monte Allie

Ordinary Loss: 87,500 87,500

Tax-Exempt Interest Income 10,000 10,000

Longer Term Capital Loss 16,000 16,000

Loss Limitation:

Beginning Stock Basis

80,000

90,000

Plus: Tax exempt Interest 10,000 10,000 Stock Basis Before Losses 90,000 100,000

Plus: Debt Basis - 10,000

Loss Limitation:

Loss Deduction 90,000 110,000

Ordinary Loss: 76,087 87,500

capital Loss 13,913.04 16,000

b. What is Monte’s stock basis on December 31?

c. What are Allie’s stock basis and debt basis on December 31?

d. What loss carryovers are available for Monte and Allie?

e. Explain how the use of the losses in Part a would change if instead Raider were a partnership and Monte and Allie were partners who shared profits, losses and liabilities equally.

e.)

Allocation to Shareholders Monte Allie

Ordinary Loss: 87,500 87,500

Tax-Exempt Interest Income 10,000 10,000

Longer Term Capital Loss 16,000 16,000

Loss Limitation: Beginning basis in partnership

80,000

90,000

Plus: Tax exempt Interest 10,000 10,000

Note payable to allie - 10,000

accounts payable 45,000 45,000

Mortgage payable 15,000 15,000

Total

150,000

170,000

Deduction

Ordinary Loss 87,500 87,500

Capital Loss 16,000 16,000

In a partnership, they are allowed to deduct ordinary and capital losses in full.

Problem 8

Tom Hughes died in 2009 with a gross estate of $3.9 million and debt of $30,000. He made post- 1976 taxable gifts of $100,000, valued at $80,000 when he died. His estate paid state death taxes of $110,200. What is his estate tax base?

Estate Tax Base:

Gross Estate: 3,900,000

Minus: Debts (30,000)

State Death Taxes (110,200)

Taxable estate: 3,759,800

Plus: Adjusted Taxable

Gifts:

100,000

[Show More]

.png)

.png)

.png)

.png)

.png)