Financial Accounting > QUESTIONS & ANSWERS > Risk-Based Approach to Conducting a Quality Audit (All)

Risk-Based Approach to Conducting a Quality Audit

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 6 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

May 16, 2021

Number of pages

6

Written in

All

Additional information

This document has been written for:

Uploaded

May 16, 2021

Downloads

0

Views

93

Document Keyword Tags

Recommended For You

Get more on QUESTIONS & ANSWERS »

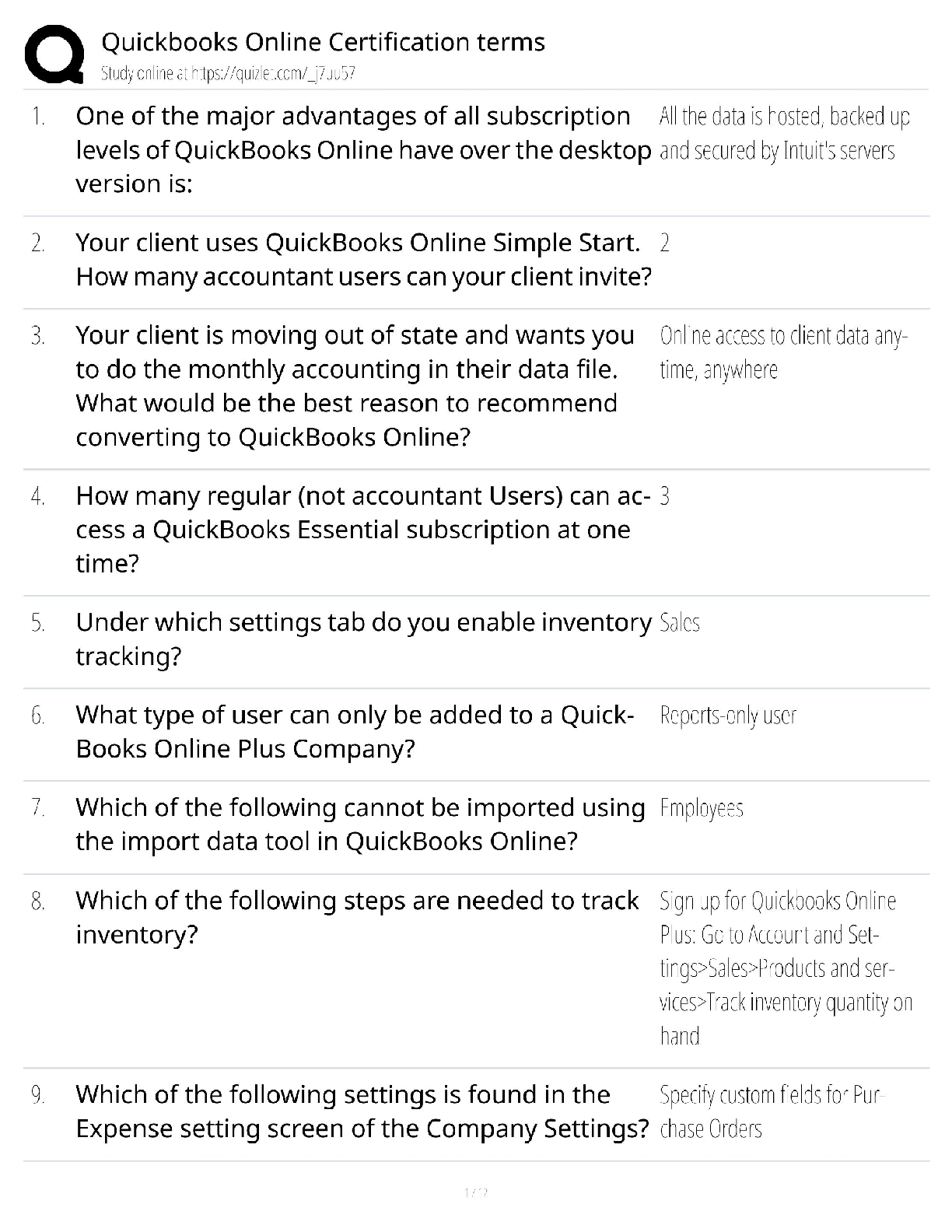

Auditing A Risk Based Approach To Conducting A Quality Audit 1...

Test Bank for Advanced Accounting 4th Edition By Jeter Cheny

Solutions Manual For Commercial Bank Management 5th Edition BY...

Solutions Manual For Advanced Accounting 11th Edition By Joe...

Financial Accounting for Decision Makers 10th Edition By Peter...

Financial Accounting for Decision Makers 10th Edition, By Pete...