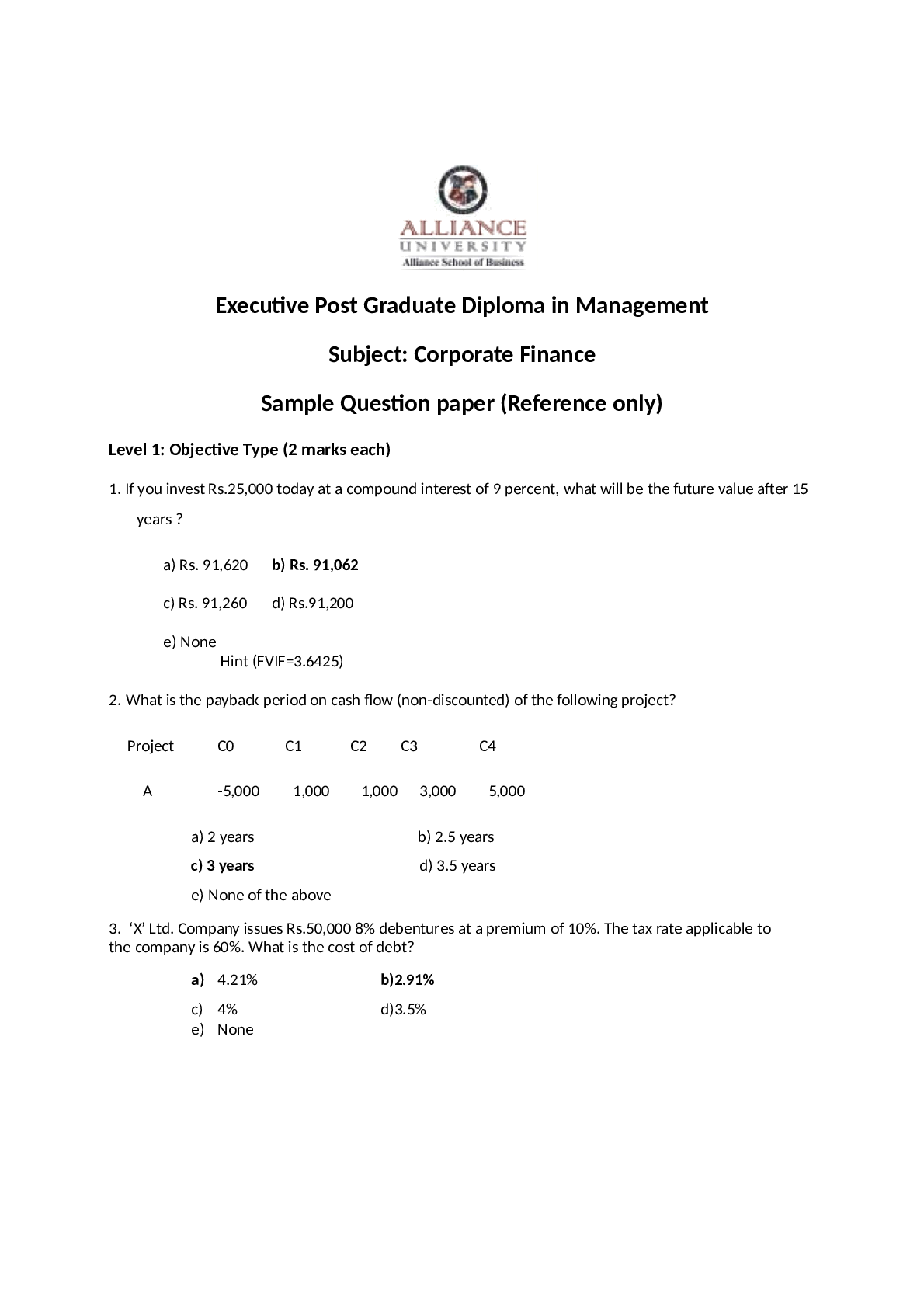

Executive Post Graduate Diploma in Management

Subject: Corporate Finance

Sample Question paper (Reference only)

Level 1: Objective Type (2 marks each)

1. If you invest Rs.25,000 today at a compound interest of 9 perc

...

Executive Post Graduate Diploma in Management

Subject: Corporate Finance

Sample Question paper (Reference only)

Level 1: Objective Type (2 marks each)

1. If you invest Rs.25,000 today at a compound interest of 9 percent, what will be the future value after 15

years ?

a) Rs. 91,620 b) Rs. 91,062

c) Rs. 91,260 d) Rs.91,200

e) None

Hint (FVIF=3.6425)

2. What is the payback period on cash flow (non-discounted) of the following project?

Project C0 C1 C2 C3 C4

A -5,000 1,000 1,000 3,000 5,000

a) 2 years b) 2.5 years

c) 3 years d) 3.5 years

e) None of the above

3. ‘X’ Ltd. Company issues Rs.50,000 8% debentures at a premium of 10%. The tax rate applicable to

the company is 60%. What is the cost of debt?

a) 4.21% b)2.91%

c) 4% d)3.5%

e) None4. What is the NPV (approximate) if cost of capital is 10 percent on cash flow of the following project?

Project C0 C1 C2 C3 C4

A -10,000 3,000 3,000 3,000 3,000

a) Rs. - 493.40

b) Rs. 493.40

c) Rs. 9507.60

d) Rs.-9507.60

e) None

5. What is the risk premium of a security, if the market return is 15%, Beta 0.8 and risk-free rate of

return is 9%.

a) 7.2%

b) 4.8%

c) 6.0%

d) 8.4%

e) None (Hint Beta*(Rm-Rrf)

6. If you 20,000, what will be the future value after 15 years ?

a) Rs.75,930

b) Rs.75,960

c) Rs.75,396

d) Rs.75,460

e) None (Hint 20000*1.0925˄15

7. What is the NPV if cost of capital is 10 percent on cash flow of the following project?

Project C0 C1 C2 C3 C4

A -5,000 1,000 1,000 3,000 5,000

a) Rs.2,340

b) Rs.2,404

c) Rs.2,450

d) Rs.2,400

e) None8. Compute the cost of equity using CAPM where risk-free rate of return is 11%, Beta co-efficient of the

firm is 1.25 and assuming a market return of 15 percent next year.

a) 16%

b) 15%

c) 16.5%

d) 16.3%

e) None Ke=RRF+Ba(Rm-Rrf)=11+1.25(15-11)=11+5=16

9. Find out the weighted average cost of capital from the following data:

Securities Book value After tax cost

Equity 5,00,000 13%

Retained earnings 2,00,000 8%

Preference capital 2,00,000 14%

Debentures 4,00,000 5%

--------------

13,00,000

========

a) 8.0%

b) 7.5%

c) 8.11 (500000*.13+200000*.08+20000*0.14+40000*.05)/1300000=9.92% (check

answer)

d) 8.2%

e) None of the above

10. From the following information;

Interest Rs. 5,000

Sales Rs.50,000

Variable cost Rs.25,000

Fixed cost Rs.15,000

Find out,

(a) Operating Leverage & Financial Leverage

a) 3.0 & 2.0b) 2.5 & 2.0 (O.L.=cont/ebit=sales-v.c/ sales-v.c.-f.c)=25000/10000=2.5)

(DOFL=ebit/ebt=10000/5000=2.0)

c)

d) 3.5 & 2.5

e) 3.0 & 2.5

f) none of the above

11. If you invest Rs.30,000 today at a compound interest of 9.50 percent, what will be the future value

after 10 years ?

a) Rs.74,934

b) Rs.74,347

c) Rs.74,734

d) Rs.74,897

d) None

12. What is the NPV if cost of capital is 12 percent on cash flow of the following project?

Project C0 C1 C2 C3 C4

A -100,000 20,000 35,000 43,000 36,000

a) Rs.567

b) Rs.657

c) Rs.-756

d) Rs.-765

e) None of the above

13. Compute the cost of equity using CAPM where risk-free rate of return is 9%, Beta co-efficient of the

firm is 1.1 and assuming a market return of 15 percent next year.

a) 16.6%

b) 15.6%

c) 16.5%

d) 15.8%

e) None of the above Ke=9+1.1(15-9)=9+6.6=15.6

14. Find out the weighted average cost of capital from the following data:

Securities Book value After tax cost

Equity 10,00,000 12%

Retained earnings 4,00,000 11%

Preference capital 4,00,000 12%

Debentures 8,00,000 7%26,00,000

a) 10.3%

(Hint: 1000000*0.12+40000*0.11+400000*0.12+800000*0.07=268000) Divide by 2600000

and it would be 10.3%

b) 12.0%

c) 11.15

d) 9.26%

e) None of the above

15. Equity shares of Phonex Ltd. are quoted in the market at Rs.17.00. The dividend expected a year

hence is Rs.1.50. The expected rate of dividend growth is 8%. The cost of equity capital to the company is;

a. 11.08%

b. 13.88%

c. 15.46%

d. 16.82%

e. None of the above

(Hint: Ke= D1/P0+g = 1.5/17+.08=0.1682 or 16.82%)

16. If the cost of equity is 18%, and the cost of debt is 15% what would be the cost of capital, at a tax rate

of 35% and a debt-equity ratio of 2:1?

a. 13.50%

b. 13.25%

c. 12.48%

d. 16.0%

e. None of the above (Hint WCOC= 1/3 *0.18+2/3 *0.15(1-0.35)=0.06+0.065=.125 or 12.5%

17. If the interest rate on long-term debt is 18% p.a. and the tax rate of the company is 35%, the cost of

debt is

a. 10.70%

b. 11.70%

c. 12.85%

d. 12.70%

e. None of the above (Hint : Kd= YTM(1-Tax Rate)=0.18(1-.35)=0.18*0.65=0.117 or 11.70%

18. Ravi & Co. issues 10% irredeemable preference shares. The face value of each share is Rs.100 and net

amount realized share is Rs.96. The cost of the preference capital is

a. 9.6%

b. 10%c. 10.42%

d. 14.32%

e. None (Hint Cost of preference Share= Preference Dividend/ Market Value of Preference share=

10/96=.10416 or 10.42%

19. The future value of a regular annuity of Rs.1000 earning a rate of interest of 12% p.a. for 5 years is

equal to

a. Rs.6,250

b. Rs.6,353

c. Rs.6,425

d. Rs.6,538

e. None Hint (Use Table 2: Multiplying factor = 6.3528 Therefore Ans=6.3528*1000=6353

20. How much is a Rupee worth today, if you can expect to receive it a year from now, with no risk of

default?

a. Less than Rs.1

b. Rs. 1

c. More than Rs.1

d. Zero

None (UGC-NET/SET: Commerce (Paper II & III) JRF and Assistant Professor Exam)

21. The present value of Rs.10,00,000 receivable after 60 years, at a discount rate of 10% is

a. Rs.3,284

b. Rs.6,898

c. Rs.18,649

d. Rs.39,440

e. Rs.48,376 (Use Table 1 FD FVIF=PxCVF Therefore P=FVIF/ CVF=1000000/304.4816=3284

22. How much should a company invest at the beginning of each year at 14% so that it can redeem

debentures of Rs.10 lakh at the end of year 10?

a. Rs. 48,195

b. Rs.45,363

c. Rs.51,714

d. Rs. 65,236

e. Rs.71,535

(Hint : Case of Future value of annuity due FVAD=P*(FVIFA)14%,10Yr * (1+i)

1000000=P*19.3373*1.14 Therefore P=1000000/(19.3373*1.14)=45362.74 Ans23. Alpha company paid a dividend of Rs.4.50. The current market price of an equity share is Rs.90.

Dividend are expected to grow at the rate of 7%, the cost of equity capital is

a. 11.5%

b. 12.35%

c. 14.25%

d. 16%

e. 18.5% Hint Ke=D1/P0 + g = {D0(1+g)/ P0} + g = {4.5(1+0.07) / 90} +0.07 = 12.35%

24. Consider the following data:

Source Market Value (Rs.) Cost (%)

Equity 10,00,000 18

Debt 5,00,000 13

If the tax rate is 35%, the weighted-average cost of funds taking market value as weights is

a. 13.00%

b. 13.82%

c. 14.00%

d 14.82%

e. 14.62%

25. If the cost of equity is 20%, and the cost of debt is 13% what would be the cost of capital, at a tax rate

of 30% and a debt-equity ratio of 1:3?

a. 18.50%

b. 15.25%

c. 17.28%

d. 20.0%

e. None of the above

26. What is the risk premium of a security, if the market return is 18%, Beta 1.25 and risk-free rate of

return is 10.5%.

a) 9.38%

b) 10.50%

c) 19.87%

d) 12.76%

e) None of the above

Hint : Risk Premium = Beta(Market rate-risk free rate)=1.25*(18-10.5)=1.25*7.5=9.3827. If the interest rate on long-term debt is 19% p.a. and the tax rate of the company is 33%, the cost of

debt is

a. 14.72%

b. 12.73%

c. 6.27%

d. 13.33%

e. None of the above

28. What is the payback period on cash flow (non-discounted) of the following project?

Project C0 C1 C2 C3 C4

A -50,000 10,000 25,000 35,000 15,000

a. 2 years

a. 2.5 years

b. 3 years

c. 3.5 years

e. None

29. A company has retained earnings of Rs.72 lakh and equity capital of Rs.38 lakh. If the equity

investors expect a rate of return of 17% and the cost of issuing fresh equity is 6%, the cost of the

external equity is

a. 16.4%

b. 17.4%

c. 17.7%

d. 18.10%

e. 19.1% (cost of external equity=Dividend expected/ Market price of share= 17/

(1-.06)=18.08%

30. The future value of a regular annuity of Rs.6000 earning a rate of interest of 9% p.a. for years is equal

to

a. Rs.75,048

b. Rs.78,480

c. Rs.74,480

d. Rs.78,840

e. None of the above

(Qustion is wrong – no time duration given)31. The primary objective of corporate management is;

a) Maximization of EBIT

b) Maximization of EPS

c) Maximization of market share price

d) Maximization of wealth of share holders

e) All of them

32. Which of the following statements is/are true for the given values of interest and time?

a. Present Value Interest Factor is the reciprocal of Future Value Interest Factor.

b. Future Value Interest Factor Annuity is the reciprocal of Present Value Interest Factor

Annuity.

c. Capital recovery factor is a product of Future Value Interest Factor and reciprocal of Future

Value Annuity Factor.

d. Both (a) and (c) above.

e. None of the above

33. Which of the following statements is/are not true?

a. The more frequent the compounding, the higher the future value, other things being equal.

b. For a given amount, greater the discount rate, lesser is the present value.

c. Converting an annuity to an annuity due decreases the present value.

d. Converting an annuity to an annuity due increases the present value.

e. None of the above Hint : FVADn=P(FVIFA i,n)(1+i) hence P=FVADn/FVIFA*(1+i)

34. Money has a time value because

a. the individuals prefer future consumption to present consumption

b. a rupee today is worth more than a rupee tomorrow in terms of purchasing power

c. a rupee today can be productively deployed to generate real returns tomorrowd. both (b) and (c)

e. All of them

35. Cash flows occurring in different periods should not be compared unless

a. interest rates are expected to be stable

b. the flows occur no more than one year from each other

c. high rates of interest can be earned on the flows

d. the flows have been discounted to a common date

e. All of them

36. Sinking fund factor is the reciprocal of

a. future value interest factor

b. present value interest factor

c. future value interest factor of annuity

d. present value interest factor of annuity

e. None of them

37. You have determined the profitability of a planned project by finding the present value of all the

cash flows from that project. Which of the following would cause the project to look more

appealing in terms of the present value of those cash flows?

a. The discount rate decreases.

b. The cash flows are extended over a longer period of time, but the total amount of the cash

flows remains the same.

c. The discount rate increases.

d. Answers b and c above.

e. None of them38. Which of the following statements is most correct?

a. A 5-year $100 annuity due will have a higher present value than a 5- year $100 ordinary

annuity.

b. A 15-year mortgage will have larger monthly payments than a 30-year mortgage of the same

amount and same interest rate.

c. If an investment pays 10 percent interest compounded annually, its effective rate will also be

10 percent.

d. All of the statements above are correct.

e. None of the above

39. Which of the following statements is most correct?

a. An investment which compounds interest semiannually, and has a nominal rate of 10 percent,

will have an effective rate less than 10 percent.

b. The present value of a three-year $100 annuity due is less than the present value of a threeyear $100 ordinary annuity.

c. The proportion of the payment of a fully amortized loan which goes toward interest declines

over time.

d. None of the answers above is correct.

e. All of them

40. Which of the following bank accounts has the highest effective annual return?

a. An account which pays 10 percent nominal interest with monthly com-pounding.

b. An account which pays 10 percent nominal interest with daily com-pounding.

c. An account which pays 10 percent nominal interest with annual com-pounding.

d. An account which pays 9 percent nominal interest with daily com-pounding.

e. None of the above

1. Corporate Finance

1. If you invest Rs.25,000/- today at a compound interest of 9%, what will be the future value

after 15 years?

(a) Rs.91,062/-

(b) Rs.91,260/-

(c) Rs.91,620/-

(d) Rs.91,200/-

(e) None of the above

If choice a is selected set score to 2.2. Finance function involves:-

(a) Safe custody of funds only

(b) Expenditure of funds only

(c) Procurement of finance only

(d) Procurement and effective utilization of funds

(e) None of the above

If choice d is selected set score to 2.

3. The primary objective of corporate management is:-

(a) Maximization of wealth of shareholders

(b) Maximization of EBIT

(c) Maximization of market share price

(d) Maximization of EPS

(e) All of the above

If choice e is selected set score to 2.

4. What is the payback period on cash flow (non discounted) of the following project?

(a) 2.5 years

(b) 3 years

(c) 3.5 years

(d) 2 years

(e) None of the above

If choice b is selected set score to 2.

5. The goal of wealth maximization takes into consideration:-

(a) Risk related to uncertainty of returns

(b) Timing of expected returns

(c) Amount of returns expected

(d) All of the above

(e) None of the above

If choice e is selected set score to 2.

6. Time value of money facilitates comparison of cash flows occurring at different time periods

by:-

(a) a) Compounding all cash flows to a common point of time

(b) b) Discounting all cash flows to a common point of time

(c) c) Using either (a) or (b)

(d) d) Neither (a) nor (b)

(e) e) None of the above

If choice c is selected set score to 2.7. 'X' Ltd. Company issues Rs.50,000/-, 8% debentures at a premium of 10%. The tax rate

applicable to the company is 60%. What is the cost of debt?

(a) 3.5%

(b) 4.21%

(c) 2.91%

(d) 4%

(e) None of the above

If choice c is selected set score to 2.

8. What is the NPV (approximate), if cost of capital is 10% on cash flow of the following

project?

(a) Rs.493.40/-

(b) Rs.-9507.60/-

(c) Rs.9507.60/-

(d) Rs.-493.40/-

(e) None of the above

If choice d is selected set score to 2.

9. Money has a time value because:-

(a) a) The individuals prefer future consumption to present consumption

(b) b) A rupee today is worth more than a rupee tomorrow in terms of purchasing power

(c) c) A rupee today can be productively deployed to generate real returns tomorrow

(d) Both (b) and (c)

(e) All of the above

If choice d is selected set score to 2.

10. Cash flows occurring in different periods should not be compared unless:-

(a) The flows occur no more than one year from each other

(b) The flows have been discounted to a common date

(c) High rates of interest can be earned on the flows

(d) Interest rates are expected to be stable

(e) All of the above

If choice b is selected set score to 2.

11. What is the risk premium of a security, if the market return is 15%, Beta 0.8 and risk-free rate

of return is 9%.

(a) 6.0%

(b) 4.8%

(c) 8.4%

(d) 7.2%

(e) None of the above

If choice b is selected set score to 2.12. Relationship between annual effective rate of interest and annual nominal rate of interest is,

if frequency of compounding is more than 1:-

(a) Effective Rate ‹ Nominal rate

(b) Effective rate › Nominal rate

(c) Effective Rate = Nominal rate

(d) All of the above

(e) None of the above

If choice b is selected set score to 2.

13. If you invest Rs.20,000/- today at a compound interest of 9.25%, what will be the future value

after 15 years?

(a) Rs.75,396/-

(b) Rs.75,960/-

(c) Rs.75,930/-

(d) Rs.75,460/-

(e) None of the above

If choice a is selected set score to 2.

14. What is the NPV if cost of capital is 10% on cash flow of the following project?

(a) Rs.2,340/-

(b) Rs.2,400/-

(c) Rs.2,450/-

(d) Rs.2,404/-

(e) None of the above

If choice d is selected set score to 2.

15. A student takes a loan of Rs.50,000/- from SBI. The rate of interest being charged by SBI is

10 percent per annum. What would be the amount of equal annual installment if he wishes to

pay it back in five installments at the end of every year ( PVIF 10%, 5 Years is 0.621 and

PVIFA is 3.791 )?

(a) Approx. Rs.15,620/-

(b) Approx. Rs.15,450/-

(c) Approx. Rs.13,190/-

(d) Approx. Rs.11,000/-

(e) None of the above

If choice c is selected set score to 2.16. You have determined the profitability of a planned project by finding the present value of all

the cash flows from that project. Which of the following would cause the project to look more

appealing in terms of the present value of those cash flows?

(a) The discount rate decreases

(b) The cash flows are extended over a longer period of time, but total amount of the cash

flows remains the same

(c) The discount rate increases

(d) All of the above

(e) None of the above

If choice a is selected set score to 2.

17. Which of the following statements is correct?

(a) An investment which compounds interest semiannually, and has a nominal rate of 10 p

ercent, will have an effective rate less than 10 percent

(b) The present value of a 3-year $100 annuity due is less than the present value of a 3-

year $100 ordinary annuity

(c) The proportion of the payment of a fully amortized loan which goes toward interest dec

lines over time

(d) All of the above

(e) None of the above

If choice c is selected set score to 2.

18. A company wants to retire a loan Rs.5,00,000/-, 10 years from today. What amount should it

invest each year for 10 years if the funds can earn 8 percent per annum. The first investment

will be made at the beginning of this year ( FVIF 10%, 10 Years is 2.594 and FVIFA is

15.937.

(a) Approx. Rs.31,950/-

(b) Approx. Rs.40,000/-

(c) Approx. Rs.34,000/-

(d) Approx. Rs.28,000/-

(e) None of the above

If choice e is selected set score to 2.

19. Find out the weighted average cost of capital from the following data:-

(a) 8.0%

(b) 8.11%

(c) 8.2%

(d) 7.5%

(e) None of the above

If choice b is selected set score to 2.20. A company has 10 percent perpetual debt of Rs.1,00,000/-. The tax rate is 35 percent.

Determine the cost of debt if the company issued at discount of 10 percent.

(a) 5.0 percent

(b) 5.91 percent

(c) 7.22 percent

(d) 6.5 percent

(e) None of the above

If choice c is selected set score to 2.

21. Which of the following bank accounts has the highest effective annual return?

(a) An account which pays 9 percent nominal interest with daily compounding

(b) An account which pays 10 percent nominal interest with daily compounding

(c) An account which pays 10 percent nominal interest with annual compounding

(d) An account which pays 10 percent nominal interest with monthly compounding

(e) None of the above

If choice b is selected set score to 2.

22. What is the NPV (approximate), if cost of capital is 10% on cash flow of the following

project?

(a) Approx. Rs.-5,500/-

(b) Approx. Rs.5,500/-

(c) Approx. Rs. 4,600/-

(d) Approx. Rs.4,600/-

(e) None of the above

If choice c is selected set score to 2.

23. If you invest Rs.30,000/- today at a compound interest of 9.50%, what will be the future value

after 10 years?

(a) Rs.74,734/-

(b) Rs.74,897/-

(c) Rs.74,347/-

(d) Rs.74,934/-

(e) None of the above

If choice c is selected set score to 2.

24. You are interested in investing your money in a bank account. Which of the following banks

provides you with the highest effective rate of interest?

(a) Bank 1; 8 percent with monthly compounding

(b) Bank 2; 8 percent with annual compounding

(c) Bank 4; 8 percent with daily (365-day) compounding

(d) Bank 3; 8 percent with quarterly compounding

(e) None of the above

If choice c is selected set score to 2.25. What is the NPV if cost of capital is 12% on cash flow of the following project?

(a) Rs.657/-

(b) Rs.-765/-

(c) Rs.567/-

(d) Rs.-756/-

(e) None of the above

If choice d is selected set score to 2.

26. Which of the following is not considered a capital component for the purpose of calculating

the weighted average cost of capital as it applies to capital budgeting?

(a) Accounts payable

(b) Long term debt

(c) Common stock

(d) Preferred stock

(e) None of the above

If choice a is selected set score to 2.

27. A company has determined that its optimal capital structure consists of 40 percent debt and

60 percent equity. Given the following information, calculate the firm's weighted average cost

of capital, where rd = 6%, Tax rate = 40%, Share Price = $25, Growth = 0%, Dividend =

$2.00.

(a) 7.2%

(b) 7%

(c) 6.2%

(d) 6%

(e) 8%

If choice c is selected set score to 2.

28. Find out the weighted average cost of capital from the following data:-

(a) 9.26%

(b) 12.0%

(c) 11.15%

(d) 10.3%

(e) None of the above

If choice d is selected set score to 2.29. Which of the following is not considered a capital component?

(a) Long term debt

(b) Common stock

(c) Permanent short term debt

(d) All of the above are considered capital components

(e) None of the above

If choice d is selected set score to 2.

30. The common stock of Anthony Steel has a beta of 1.20. The risk-free rate is 5 percent and

the market risk premium (rM - rRF) is 6 percent. What is the companys cost of common stock,

rs?

(a) 7%

(b) 12.4%

(c) 7.2%

(d) 12.2%

(e) 11%

If choice d is selected set score to 2.

31. Equity shares of Phonex Ltd. are quoted in the market at Rs.17.00/-. The dividend expected

a year hence is Rs.1.50/-. The expected rate of dividend growth is 8%. The cost of equity

capital to the company is:-

(a) 13.88%

(b) 16.82%

(c) 15.46%

(d) 11.08%

(e) None of the above

If choice b is selected set score to 2.

32. Which of the following statements is correct?

(a) a) If a company's tax rate increases but the yield to maturity of its non callable bonds r

emains the same, the company's marginal cost of debt capital used to calculate its weighted

average cost of capital will fall

(b) b) All else equal, an increase in a company's stock price will increase the marginal cos

t of common stock,re.

(c) c) All else equal, an increase in interest rates will decrease the marginal cost of comm

on stock, re.

(d) d) Both (a) and (b)

(e) e) None of the above

If choice a is selected set score to 2.

33. A stock split will cause a change in the total rupee amounts shown in which of the following

balance sheet accounts?

(a) Cash

(b) Common stock

(c) Paid-in capital

(d) Retained earnings

(e) None of the above

If choice e is selected set score to 2.34. Which of the following statements is correct?

(a) a) The WACC is a measure of the before-tax cost of capital

(b) b) Typically the after-tax cost of debt financing exceeds the after-tax cost of equity fina

ncing

(c) c) The WACC measures the marginal after-tax cost of capital

(d) d) Both (a) and (b)

(e) e) None of the above

If choice c is selected set score to 2.

35. Which of the following actions will enable a company to raise additional equity capital (that is,

which of the following will raise the total book value of equity)?

(a) a) The establishment of a new-stock dividend reinvestment plan

(b) b) A stock split

(c) c) The establishment of an open-market purchase dividend reinvestment plan

(d) d) A stock repurchase

(e) e) Both (a) and (d)

If choice a is selected set score to 2.

36. A company has a capital structure which consists of 50 percent debt and 50 percent equity.

Which of the following statements is correct?

(a) The WACC represents the cost of capital based on historical averages. In that sense, i

t does not represent the marginal cost of capital

(b) The cost of equity financing is greater than or equal to the cost of debt financing

(c) The WACC exceeds the cost of equity financing

(d) The WACC is calculated on a before-tax basis

(e) None of the above

If choice b is selected set score to 2.

37. Which of the following statements is correct?

(a) a) The weighted average cost of capital for a given capital budget level is a weighted a

verage of the marginal cost of each relevant capital component which makes up the firm's tar

get capital structure

(b) b) The weighted average cost of capital is calculated on a before-tax basis

(c) c) An increase in the risk-free rate is likely to increase the marginal costs of both debt

and equity financing

(d) d) Both (a) and (c)

(e) e) All of the above

If choice d is selected set score to 2.

38. Which of the following is not an advantage of using book value weights for computing the

cost of capital?

(a) The calculation of the weights is very simple

(b) Book value weights are likely to fluctuate less over a period as these are not affected b

y the fluctuations in market prices

(c) Book value weights are consistent with the concept of cost of capital

(d) Book value weights are the only usable basis when market values are not obtainable o

r reliable

(e) None of the above

If choice d is selected set score to 2.39. Which of the following are examples of a primary market transaction?

(a) a) A company issues new common stock

(b) b) A company issues new bonds

(c) c) An investor asks his broker to purchase 1,000 shares of Microsoft common stock

(d) d) All of the above

(e) e) Both (a) and (b)

If choice e is selected set score to 2.

40. If the expected rate of return on a stock exceeds the required rate:-

(a) The company is probably not trying to maximize price per share

(b) The stock is a good buy

(c) The stock should be sold

(d) Dividends are not being declared

(e) The stock is experiencing supernormal growth

If choice b is selected set score to 2.

41. Which of the following is/are true about NPV?

(a) a) It considers all the cash flows

(b) b) It gives more weightage to distant flows than to near-term flows

(c) c) It considers time value of money

(d) Both (a) and (c)

(e) None of the above

If choice d is selected set score to 2.

42. Cash flows occurring from a project in different period are comparable unless:-if:

(a) Interest rates are expected to be stable

(b) The flows have been discounted to a single date

(c) The flows occur periodically every year

(d) Interest can be earned on the cash flows

(e) None of the above

If choice b is selected set score to 2.

43. Consider the following data:

If the tax rate is 35%, the weighted average cost of funds taking market value as weights is:-

(a) 14.00%

(b) 15.82%

(c) 14.96%

(d) 15.00%

(e) 16.62%

If choice c is selected set score to 2.44. The _________ is the time period that elapses from the point when the firm sells a finished

good on account to the point when the receivable is collected..

(a) cash conversion cycle

(b) average payment period

(c ) average collection period

(d) average age of inventory

(e) None of the above

If choice c is selected set score to 2.

45. Conflicts in ranking of projects on the basis of NPV and IRR arise due to:-

(a) a) Disparity in the timing of cash inflows

(b) b) Disparity in the size of cash inflows

(c) c) Disparity in the life of cash flows

(d) Both (a) and (b)

(e) None of the above

If choice d is selected set score to 2.

46. _________ projects do not compete with each other; the acceptance of one _________ the

others from consideration.

(a) Independent; does not eliminate

(b) Capital; eliminates

(c) Replacement; does not eliminate

(d) Mutually exclusive; eliminates

(e) None of the above

If choice a is selected set score to 2.

47. The rationale for not including sunk costs in capital budgeting decisions is that they:-

(a) Revert at the end of the investment

(b) Represent nominal, not real, outflows

(c) Are usually small in magnitude

(d) Are historical costs

(e) None of the above

If choice d is selected set score to 2.

48. Which of the following events is likely to encourage a company to raise its target debt ratio?

(a) a) An increase in the corporate tax rate

(b) b) An increase in the personal tax rate

(c) c) An increase in the company's operating leverage

(d) Both (a) and (c)

(e) All of the above

If choice a is selected set score to 2.49. Which of the following would increase the likelihood that a company would increase its debt

ratio in its capital structure?

(a) a) An increase in costs incurred when filing for bankruptcy

(b) b) An increase in the corporate tax rate

(c) c) A decrease in the firm's business risk

(d) Both (b) and (c)

(e) None of the above

If choice b is selected set score to 2.

50. The aggressive financing strategy results in the firm financing its short-term needs with

_________ funds and its long-term needs with _________ funds.

(a) long-term; short-term

(b) short-term; long-term

(c) Permanent; seasonal

(d) seasonal; permanent

(e) None of the above

If choice b is selected set score to 2.

51. Which of the following statements is correct?

(a) a) A firm can use retained earnings without paying a flotation cost. Therefore, while the

cost of retained earnings is not zero, the cost of retained earnings is generally lower than the

after-tax cost of debt financing

(b) b) The capital structure that minimizes the firm's cost of capital is also the capital struct

ure that maximizes the firm's stock price

(c) c) The capital structure that minimizes the firm's cost of capital is also the capital struct

ure that maximizes the firm's earnings per share

(d) d) If a firm finds that the cost of debt financing is currently less than the cost of equity fi

nancing, an increase in its debt ratio will always reduce its cost of capital

(e) Both (a) and (b)

If choice b is selected set score to 2.

52. Which of the following statements is correct?

(a) a) Since debt financing raises the firm's financial risk, raising a company's debt ratio wi

ll always increase the company's WACC

(b) b) Since debt financing is cheaper than equity financing, raising a company's debt ratio

will always reduce the company's WACC

(c) c) Increasing a company's debt ratio will typically reduce the marginal cost of both debt

and equity financing; however, it still may raise the company's WACC

(d) Both (a) and (c)

(e) None of the above

If choice e is selected set score to 2.

53. According to NI approach:-

(a) a) The total market value of a firm and the cost of capital are dependent on the capital

structure

(b) b) The total market value of a firm and the cost of capital are independent of capital str

ucture

(c) c) The capital structure has no relevance

(d) Both (a) and (c)

(e) None of the above

If choice a is selected set score to 2.54. Under Net Income Approach (NIA), change in the capital structure of a company:-

(a) Does not cause any change either in the overall cost of capital or in the total value of a

firm

(b) No changes in overall cost of capital

(c) Causes corresponding change in the overall cost of capital as well as the total value of

a firm

(d) Causes corresponding change in the overall cost of capital only

(e) None of the above

If choice c is selected set score to 2.

55. In Net Operating Income (NOI) approach, market value of a firm:-

(a) Is sometimes affected by capital structure changes

(b) Is affected by capital structure changes

(c) Is affected proportionately

(d) Is not at all affected by capital structure changes

(e) None of the above

If choice d is selected set score to 2.

56. Financial structure includes:-

(a) Long term as well as short term sources of funds

(b) Equity share capital of the company

(c) Long term sources of funds

(d) Medium term source of funds

(e) None of the above

If choice a is selected set score to 2.

57. The term capital structure:-

(a) Is not part of financial structure

(b) Is part of financial structure

(c) Is part of appropriation account

(d) Is part of profit & loss account

(e) None of the above

If choice b is selected set score to 2.

58. Which of the following statement(s) is true?

(a) Risk that can be eliminated by diversification is called specific risk

(b) Risk that cannot be avoided, regardless of how much you diversity is known as market

risk

(c) The variability of earnings before interest and taxes is referred to as business risk

(d) All of the above

(e) None of the above

If choice d is selected set score to 2.

59. Which of the following is not a feature of debt finance?

(a) a) Dilution of control

(b) b) Low cost

(c) c) Financial risk

(d) Both (b) and (c)

(e) None of the above

If choice a is selected set score to 2.60. Which of the following factors has an effect on business risk?

(a) Demand for products manufactured by the firm

(b) Volatility in prices of the products manufactured by the firm

(c) Variability in input prices

(d) All of the above

(e) None of the above

If choice d is selected set score to 2.

61. The Modigliani-Miller argument is that:-

(a) a) The value of the levered firm will be more than that of unlevered firm

(b) b) The value of the unlevered firm will be more than the levered firm

(c) c) Levered firms cannot enjoy a premium over unlevered firms as the investors will abo

lish the difference through personal leverage

(d) Either (a) or (b) may be true depending on other circumstances

(e) None of the above

If choice c is selected set score to 2.

62. Business risk refers to:-

(a) a) Variability of sales

(b) b) Variability of the market value of the firm

(c) c) Variability of cost of raw materials

(d) Both (a) and (c)

(e) None of the above

If choice d is selected set score to 2.

63. Which of the following is true?

(a) Operating leverage measures the sensitivity of EBT to changes in the quantity produce

d and sold

(b) Operating leverage measures the sensitivity of EBIT to changes in quantity produced a

nd sold

(c) Operating leverage measures the sensitivity of PAT to changes in quantity produced a

nd sold

(d) Operating leverage measures the sensitivity of PBDT to changes in quantity produced

and sold

(e) None of the above

If choice b is selected set score to 2.

64. Total or Combined leverage measures the relationship between:-

(a) PAT and sales

(b) Sales and EPS

(c) EBIT and sales

(d) EPS and EBIT

(e) None of the above

If choice b is selected set score to 2.

65. Which of the following is/are correct?

(a) a) Value of the firm and cost of capital are directly related

(b) b) Value of the firm and cost of capital are inversely related

(c) c) The claim of preference shareholders is prior to that of equity shareholders

(d) Both (b) and (c)

(e) None of the above

If choice d is selected set score to 2.66. The ultimate objective of any company is:-

(a) Wealth maximization

(b) Sale maximization

(c) Profit maximization

(d) Improving its reputation

(e) None of the above

If choice a is selected set score to 2.

67. Which of the following best describes a firm's cost of capital?

(a) a) It is the weighted arithmetic average of the cost of various sources of long term fina

nce used by it

(b) b) The rate of return the firm must earn on its investments in order to satisfy the expect

ations of investors who provide long term funds to it

(c) c) It is the weighted arithmetic average of the cost of various sources of long term finan

ce and short term finance used by it

(d) Both (a) and (b)

(e) None of the above

If choice d is selected set score to 2.

68. Which of the following statements is true?

(a) Retained earnings is the only principal source of finance for growing firms

(b) Retained earnings represent the profits ploughed back into the business

(c) Retained earnings represent the extent to which the firm has invested in liquid assets o

ut of its profits

(d) Retained earnings are given lesser importance when a firm follows a residual dividend

policy

(e) None of the above

If choice b is selected set score to 2.

69. Which of the following long term sources of finance puts maximum restraint on managerial

freedom?

(a) Retained earnings

(b) Preference capital

(c) Equity capital

(d) Term loans

(e) None of the above

If choice d is selected set score to 2.

70. The cost of debt remains more or less constant up to a certain degree of leverage but rises

thereafter at an increasing rate. This proposition is based on:-

(a) Net income approach on capital structure

(b) Miller-Modigliani approach

(c) Net operating income approach on capital structure

(d) Traditional position/Traditional approach on capital structure

(e) None of the above

If choice d is selected set score to 2.71. Which of the following is true regarding sound capital market structure of a company?

(a) The capital structure should be determined within the debt capacity of the company an

d this capacity should not be exceeded

(b) Use of debt should be avoided as it adds to financial risk of the company

(c) Minimum use of leverage at minimum cost

(d) The risk of loss of control of the company due to capital structure is a major concern in

a closely held company

(e) The capital structure should not change over a period of time

If choice a is selected set score to 2.

72. Which of the following concepts explains the relationship between shareholders and

Managers?

(a) Valuation

(b) Value based management

(c) Agency consideration

(d) Shareholder wealth maximization

(e) Miller-Modigliani

If choice c is selected set score to 2.

73. A significant assumption of the net operating income is that:-

(a) Debt and equity levels do not change

(b) Dividend increase at a constant rate

(c) It remains constant regardless of changes in leverage

(d) Interest expense and taxes are included in the calculation

(e) It decreases up to a certain point of time, and then increases at an increasing rate, wit

h increasing levels of leverage

If choice c is selected set score to 2.

74. Which of he following best describes the situation in which a firm is having problem meeting

its financial obligations?

(a) Business risk

(b) Legal bankruptcy

(c) Technical bankruptcy

(d) Financial risk

(e) Financial distress

If choice e is selected set score to 2.

75. Which of the following risks is revealed by capital structure ?

(a) a) Liquidity risk

(b) b) Financial risk

(c) c) Market risk

(d) d) Firm's total risk

(e) Both (b) and (d)

If choice a is selected set score to 2.

76. Trade creditors of a company are mostly interested in the company's:-

(a) Activity ratios

(b) Liquidity ratio

(c) Profitability ratios

(d) Valuation ratios

(e) Leverage ratios

If choice b is selected set score to 2.77. A decrease in a firm's willingness to pay dividends is likely to result from an increase in its:-

(a) Profitable investment opportunities

(b) Stock price

(c) Access to capital markets

(d) Earnings stability

(e) None of the above

If choice a is selected set score to 2.

78. A stock split will cause a change in the total dollar amounts shown in which of the following

balance sheet accounts?

(a) Cash

(b) Common stock

(c) Paid in capital

(d) All of the above

(e) None of the above

If choice e is selected set score to 2.

79. Which of the following statements is correct?

(a) a) If a company puts in place a 2-for-1 stock split, its stock price should roughly double

(b) b) Share repurchases are taxed less favorably than dividends; this explains why comp

anies typically pay dividends and avoid share repurchases

(c) c) On average, a company's stock price tends to rise when it announces that it is initiati

ng a share repurchase program

(d) Both (a) and (b)

If choice c is selected set score to 2.

80. Longer the manufacturing period

(a) Greater is the requirement of working capital

(b) There is no change in the operating cycle

(c) Shorter is the requirements of working capital

(d) Lesser is the requirement of working capital

(e) None of the above

If choice a is selected set score to 2.

81. Which of the following factors influence the pay out ratio of a firm?

(a) a) Funds requirement

(b) b) Liquidity position of the firm

(c) c) Access to external sources of financing

(d) All of the above

(e) Both (a) and (b)

If choice d is selected set score to 2.

82. Which of the following sources cannot be used for payment of dividend?

(a) a) Current profits after providing for depreciation

(b) b) Profits for any previous financial year to years

(c) c) Capital

(d) Both (b) and (c)

(e) Either (b) or (c)

If choice c is selected set score to 2.83. Net working capital denotes:-

(a) Total liabilities

(b) Excess of fixed assets over current assets

(c) Excess of current liabilities over current assets

(d) Excess of current assets over current liabilities

(e) None of the above

If choice d is selected set score to 2.

84. Other things held constant, which of the following will cause an increase in working capital?

(a) Merchandize is sold at a profit, but the sale is on credit

(b) A cash dividend is declared and paid

(c) Cash is used to buy marketable securities

(d) Long term bonds are retired with the proceeds of a preferred stock issue

(e) None of the above

If choice a is selected set score to 2.

85. Which of the following statements is correct?

(a) Trade credit is provided to a business only when purchases are made

(b) Commercial paper is a form of short term financing that is primarily used by large, fina

ncially stable companies

(c) Short term debt, while often cheaper than long term debt, exposes a firm to the potenti

al problems associated with rolling over loans

(d) All of the above

(e) None of the above

If choice d is selected set score to 2.

86. Which of the following is not a current asset?

(a) a) Prepaid expenses

(b) b) Short term loans and advances

(c) c) Marketable securities

(d) Both (a) and (b)

(e) None of the above

If choice b is selected set score to 2.

87. Which of the following is the least liquid among current assets?

(a) Inventories

(b) Prepaid expenses

(c) Cash

(d) Short term securities

(e) Debtors

If choice a is selected set score to 2.

88. The current ratio is obtained by:-

(a) Dividing quick assets by total liabilities

(b) Dividing quick assets by long term liabilities

(c) Dividing current assets by current liabilities

(d) Dividing current assets by total liabilities

(e) Dividing quick assets by current liabilities

If choice c is selected set score to 2.89. Which of the following best describes working capital gap?

(a) Quick assets less current liabilities other than bank

(b) Current assets less short term bank borrowings

(c) Current assets less current liabilities other than bank borrowings

(d) Quick assets less current liabilities

(e) Current assets less current liabilities

If choice c is selected set score to 2.

90. Financial risk involves:-

(a) a) Fluctuations in exchange rates

(b) b) Different interest and inflation rates

(c) c) Balance of payments position

(d) All of the above

(e) Both (a) and (b)

If choice d is selected set score to 2.

91. Which of the following features of preference shares is/are similar to those of equity shares?

(a) a) Redeemability

(b) b) No obligation to pay dividend

(c) c) Voting rights

(d) d) Charge over assets

(e) e) Both (b) and (c)

If choice b is selected set score to 2.

92. Euro-Convertible Bonds (ECBs) issued by Indian Companies refer to bonds issued in foreign

currency in:-

(a) India and any country in Europe

(b) European countries only

(c) Europe and North America

(d) India or any country outside India

(e) Any country other than India

If choice e is selected set score to 2.

93. Which of the following is a/are feature(s) of equity capital?

(a) a) The payment of dividend is compulsory, irrespective of the company's financial perf

ormance

(b) b) The dividend, if not paid during a year, becomes payable in the next year

(c) c) Dividend becomes payable only if recommended by the BoD and passed by the co

mpany in the AGM

(d) d) Both (a) and (b)

(e) e) None of the above

If choice c is selected set score to 2.

94. The major advantages of privately placing the securities are:-

(a) Faster access to funds

(b) Fewer procedural formalities

(c) Lower issue cost

(d) Easy access for any company

(e) All of the above

If choice e is selected set score to 2.95. Which of the following is not a source of long term finance?

(a) Equity capital

(b) Term loan

(c) Debenture capital

(d) Commercial paper

(e) Preference capital

If choice d is selected set score to 2.

96. Which of the following statements is true?

(a) Equity shareholders enjoy the rewards of ownership and bear the risks of the ownershi

p

(b) Post-tax cost of debentures is always less than the post-tax cost of the term loans

(c) The par value and issue price of an equity share are always capital

(d) All outstanding issues of shares are traded in the primary markets

(e) None of the above

If choice a is selected set score to 2.

97. The costliest of long term source of finance is:-

(a) Preference share capital

(b) Equity share capital

(c) Debentures

(d) Retained earnings

(e) Capital raised through private placement

If choice b is selected set score to 2.

98. Which of the following statements is/are true? With the commencement of the Companies

Act, 1956, the issue of preference shares with voting rights has been restricted only to the

following cases:-

(a) There are arrears in dividends for two or more years incase of cumulative preference s

hares

(b) Preference dividend is due for a period of two or more consecutive preceding years

(c) In the preceding six years including the immediately preceding financial year, if the co

mpany has not paid the preference dividend for a period of three or more years

(d) All of the above

(e) None of the above

If choice d is selected set score to 2.

99. A cumulative preference share is one:-

(a) In which all the unpaid dividends are carried forward and payable

(b) Which allows the issuing company the right to call the preference shares wholly or part

ly at a certain price

(c) Which can be redeemed

(d) Which can be converted into equity shares

(e) None of the above

If choice a is selected set score to 2.100. Which of the following is/are true about equity capital as a source of finance?

(a) a) Using equity capital to finance working capital may lead to a situation of 'technical in

solvency'

(b) b) Assessing the cost of equity capital is a difficult and complex task

(c) c) Equity capital provides tax benefits to the issuing company

(d) d) Cost of retained earnings is lesser than the cost of debt capital

(e) e) Both (b) and (d)

If choice b is selected set score to 2.

101. Rights issue is the method of raising funds:-

(a) a) In which secur

ities are simultaneously issued to the existing shareholders and the public

(b) b) Generally issued to the existing shareholders at a price lower than the current mark

et price

(c) c) Generally entailing lower costs of issue

(d) d) Generally made to high net worth individuals

(e) e) Both (b) and (c)

If choice e is selected set score to 2.

102. Which of the following, from the firm's point of view, can be considered as the

advantage(s) of using equity capital as a source of long term funds?

(a) a) It does not involve any fixed obligation for payment of dividends

(b) b) Equity dividends are payable from post-tax earnings. They are not tax deductible ex

penses

(c) c) It enhances the creditworthiness of the company

(d) d) Both (a) and (c)

(e) e) None of the above

If choice d is selected set score to 2.

103. Which of the following characteristics is/are true, with reference to preference capital?

(a) a) Preference dividend is payable only out of distributable profits

(b) b) Preference dividend is tax deductible

(c) c) The claim of preference shareholders is prior to the claim of equity shareholders

(d) d) Both (a) and (c)

(e) e) All of the above

If choice d is selected set score to 2.

104. What is/are the factor(s) which make(s) debentures attractive to investors?

(a) a) They enjoy a high order of priority in the event of liquidation

(b) b) Stable rate of return

(c) c) Protected by the provisions of Debenture Trust Deed

(d) d) All of the above

(e) e) Both (a) and (b)

If choice d is selected set score to 2.105. The major advantage(s) of entering into a Buy Out Deal (BOD) is/are:-

(a) An advantage accruing to the investor is that the issue price usually reflects the compa

ny's intrinsic value

(b) Companies, both existing and new, which do not satisfy conditions laid down by the S

EBI for premium issues, may issue at a premium through the BOD method

(c) There is less issue cost

(d) The procedural complexities are reduced considerably and the funds reach the firm up

front

(e) All of the above

If choice e is selected set score to 2.

1.

The present value interest factor of an (ordinary) annuity

(PVIFA) is the reciprocal of the future value interest factor

of an (ordinary) annuity (FVIFA).

Your Answer: True

Correct Answer: False

The reciprocal of the FVIF is the PVIF -- (1 + i)n = FVIF; 1/(1 + i)n = PVIF; but

this technique does not work with the annuity factors.

2.

If you would like to double your money in 6 years, the

approximate annual return you need is 12 percent (Rule of

72).

Your Answer: True

3.

A savings account at Bank A pays 6.2 percent interest,

compounded annually. Bank B's savings account pays 6

percent compounded semiannually. Bank B is paying less

total interest each year.

Your Answer: False

Correct Answer: True

Bank B is paying the equivalent of 3% twice a year. The effective annual rate

(EAR) is [ (1+.03)2 -1 ] or 6.09%. This is less than Bank A at 6.2% annually.

4.

All other things being equal, I'd rather have $10,000 in 10

years than to receive $10,000 today.

Your Answer: False5.

The rate of interest is used to express the time value of

money.

Your Answer: True

1. Finding the present value is simply the reverse of compounding.

Ans True

2. The present value interest factor (PVIF) is the reciprocal of the future value

interest factor (FVIF).

Ans True

3. If the discount rate decreases, the present value of a given future amount

decreases.

Ans False

4. The present value interest factor for a dollar on hand today is 0.

Ans False ( hint The PVIF at n = 0 is equal to one)

5. If you would like to double your money in 8 years, the approximate compound

annual return you need is 9 percent (Rule of 72).

Ans True

6. A saving account at Bank A pays 6 percent interest, compounded annually.

Bank B's savings account pays 6 percent compounded semiannually. Bank B is

paying twice as much interest.

Ans False (hint : Bank B is paying the equivalent of 3% twice a year. The effective

annual interest rate is (1+.03) ² - 1 or 6.09%. This is more than Bank A is paying,

but certainly not double.)

7. All other things being equal, I'd rather have $1,000 today than to receive $1,000

in 10 years.

Ans True

8. For a given nominal interest rate, the more numerous the compounding periods,

the less the effective annual interest rate.

Ans : False (As compounding periods increase, the effective annual interest rate

becomes LARGER.)

9. If money has a time value, then the future value will always be more than the

original amount invested.Ans : True

10. All other things remaining the same, an annuity received at the beginning of

each period has more present value than does one received at the end of each

period.

Ans : True

1. Question: Find present value of Rupees 80,000 to be received after five years when

required rate of return is 10%

Solution: PV = Cash flow/(1+r)t = 80,000/(1+0.10)5 = 80,000/1.61051 = Rupees 49,674

2. Find the present value of a series of cash flows occurred in different years when the

required rate of return is 10%

PERIOD FUTURE CASH FLOWS

1 RUPEES 80,000

2 RUPEES 70,000

3 RUPEES 50,000

4 RUPEES 30,000

As we know, PV = Future cash flow/(1+r)t S PV = {80,000/(1+0.10)1} + {70,000/(1+0.10)2} +

{50,000/(1+0.10)3} + {30,000/(1+0.10)4} = (80,000/1.10) + (70,000/1.21) + (50,000/1.331) +

(30,000/1.4641) = 72727 + 57851 + 37566 +20490 = Rupees 1,88,634

1. Interest paid (earned) on only the original principal borrowed

(lent) is often referred to as?

(a) Compound interest

(b) Future value

(c) Present value

(d) Simple interest

2. Treasury bills are?

(a) Issued on a premium basis and pay a fixed annual interest rate

(b) Issued on a discount basis and mature at par

(c) Issued on a premium basis and mature at par

(d) Issued on a discount basis and pay a fixed annual interest rate

3. Nominal Interest Rate is also known as?

(a) Annual percentage rate

(b) Effective interest Rate

(c) Periodic interest rate

(d) Coupon rate4. The concept of compound interest refers to?

(a) The process of gradually retiring a debt through periodic payments of

principal and interest

(b) The process of servicing a debt with regular interest payments,

followed lump sum payment of principal and interest at the end of the

loan term

(c) The process of converting future lump sums and annuities into present

values at a stated interest rate

(d) The process of earning interest on an original amount, plus interest on

interest previously earned

Correct!

5. The value of money to be received in the future is _______the

value of the same amount of money in hand today?

(a) Higher than

(b) Lower than

(c) The same as

(d) None of the above

6. The Time value of money must be considered in total outlay

decision because?

(a) Cash inflows and out flows occur at different point

(b) Inflation greatly reduce the outflows

(c) A dollar received in future is more value able than a dollar today

(d) Cash flows are not known with certainty

7. Interest paid (earned) on both the original principal borrowed

(lent) and previous interest allowed (earned) is often referred to

as __________?

(a) Compound interest

(b) Double interest

(c) Simple interest

(d) Present value

8. Money has time value because?

(a) Individuals prefer future consumption to present consumption

(b) Money today is worth more than money tomorrow in terms of

purchasing power(c) There is a possibility of earning risk free return on money invested

today

(d) B and C above

Correct!

9. The real rate of interest reflects compensation for?

(a) Present value

(b) Future value

(c) Time value of money

(d) None of above

10. Interest has 3 types?

(a) Fixed rate, current rate, market rate

(b) Market rate, combination rate, fixed rate

(c) Fixed rate, floating rate, current rate

(d) Fixed rate, floating rate, combination rate

MCQs 11-20

11. The basic rule of the time value of

money is?

(a) Investments will always be worth more tomorrow than they are today

(b) Its always wiser to save a dollar for tomorrow than to spend it today

(c) A dollar in hand today is worth more than a dollar promised at some time in the

future

(d) All of the above express an aspect of the basic rule of time value of money

Wrong!

12. A decrease in the supply for

loanable funds, holding demand

constant, will cause interest rates to?

(a) Increase

(b) Decrease

(c) Stay the same(d) Not enough information to tell

Wrong!

13. The value of money results from?

(a) Its backing

(b) Rates set by the State Bank

(c) Its purchasing power

(d) None of the above

Correct!

14. The basic price that equates the

demand for and supply of loanable

funds in the financial markets is the

_______?

(a) Interest rate

(b) yield curve

(c) Term structure

(d) Cash price

Correct!

15. If the interest rate is greater than

0%, then a dollar today is worth?

(a) Less than a dollar tomorrow

(b) The same as a dollar tomorrow

(c) More than a dollar tomorrow

(d) There is not sufficient information to tell

Correct!

16. In an inflationary period, interest

rates have a tendency to?

(a) Fall

(b) Rise

(c) Stay the same

(d) Act erratically

Correct!17. Which of the following is not a

determinant of market interest rates?

(a) The inflation premium

(b) The maturity risk premium

(c) The volatility risk premium

(d) The real rate of interest

Wrong!

18. An unexpected increase in inflation

should?

(a) Increase the demand for loanable funds

(b) Decrease the interest rate on loans

(c) Increase the interest rate on loans

(d) None of the above

Correct!

19. If the interest rate is less than 0%,

then a dollar today is worth?

(a) More than a dollar tomorrow

(b) The same as a dollar tomorrow

(c) Less than a dollar tomorrow

(d) There is not sufficient information to tell

Correct!

20. The risk-free interest rate is

composed of?

(a) An inflation premium and a default risk premium

(b) A default risk premium and a maturity risk premium

(c) A real rate of interest and a liquidity premium

(d) A real rate of interest and an inflation premium

Correct!Level 2: Descriptive Type (10 marks each)

1.“Working capital must be adequate, but at the same time not excessive”. Comment.

2.‘From an account keeper to strategic decision maker – the role of finance manager has undergone

a see change during recent times’. Explain.

3. ‘Wealth maximization is an operationally feasible criterion for evaluation of financial decisions’.

Comment.

4. Which working capital approach or finance policy do you recommend for profitability-solvency

tangle for the company? Comment.

5.“The credit policy of a company is criticized because the bad-debt period has also increased

considerably and the collection period has also increased”. Discuss under what conditions this

criticism may not be justified.

6. What do you understand by a Capital Structure? What basic principles will you advocate in the

matter of deciding on a proper pattern of capital structure for a company? Explain with one

illustration.

7. What are the various long-term sources are available to the Indian businessman for raising funds

to the business.

8. “Venture capital can provide a tremendous boost to the entrepreneurial activities in the

developing countries”. Comment.

9. Compare and contrast the features of equity shares, preference shares and debentures and

suggest which is better instrument to finance a new company.

10. What is the difference between primary market and secondary market?

Top 4 Sources of Finance

(With Formula and

Calculations)

This article throws light upon the top four sources

of finance. The sources are: 1. Cost of Debt 2. Cost

of Preference Capital 3. Cost of Equity Share

Capital 4. Cost of Retained Earnings.

Finance: Source # 1. Cost of Debt: i. Cost

Perpetual/Irredeemable Debt:The cost of debt is the rate of interest payable on debt.

For example, a company issues Rs. 1,00,000 10%

debentures at par; the before-tax cost of this debt

issue will also be 10% By way of a formula, beforetax cost of debt may be calculated as:

ADVERTISEMENTS:

(i) Kdb = I/P

where, K db = Before tax cost of debt

I = Interest

and P = Principal

In case the debt is raised at premium or discount, we

should consider P as the amount of net proceeds received

from the issue and not the face value of securities.

The formula may be changed to:

(ii) Kdb = I/NP (where, NP= Net Proceeds)

Further, when debt is used as a source of finance, the

firm saves a considerable amount in payment of tax as

interest is allowed as a deductible expense in

computation of tax. Hence, the effective cost of debt is

reduced.

The After-tax cost of debt may be calculated with

the help of following formula:

(iii) Kda= Kdb(1-t) = I/NP (1-t)

where, K da = After-tax cost of debt

t = Rate of tax.

Illustration 1:

(a) X Ltd. issues Rs. 50,000 8% debentures at par. The tax

rate applicable to the company is 50%. Compute the cost

of debt capital.

(b) Y Ltd. issues Rs. 50,000 8% debentures at a premium

of 10%. The tax rate applicable to the company is 60%.

Compute cost of debt capital.(c) A Ltd. issues Rs. 50,000 8% debentures at a discount

of 5%. The tax rate is 50%, Compute the cost of debt

capital.

(d) B Ltd. issues Rs. 1,00,000 9% debentures at a

premium of 10%. The costs of floatation are 2%. The tax

rate applicable is 60%. Compute cost of debt-capital.

Solution:

ii. Cost of Redeemable Debt:

Usually, the debt is issued to be redeemed after a certain

period during the life time of a firm. Such a debt is known

as redeemable debt. The cost of redeemable debt capital

may be computed by using yield to maturity, also called

internal rate of return or trial and error method. The

approximate cost of redeemable debt can also be

computed by using the simple shortcut method.

(a) Yield to Maturity or Trial and Error Method:

(i) Before tax cost of redeemable debt:where, V0 = Current value or the issue price of

debt/debenture

Vn = Redeemable value of debt

I, I2 …In = Amount of annual interest in period 1, 2

………………… , and so on

n = Number of years to redemption

kd = Yield to maturity or internal rate of return or cost of

debt/debenture

The value of kd (yield to maturity) can be found by trial

and error method using present value tables.

(ii) After tax cost of redeemable debt:

kda = kdb(1-t)

Where, kdb = After tax cost of debt

kdb = Before tax cost of debt

t = Tax Rate

Illustration 2:

A five year Rs. 100 debenture of a firm can be sold for a

net price of Rs. 95.90. The coupon rate of interest is 14

per cent per annum, and the debenture will be redeemed

at 5 per cent premium on maturity. The firm’s tax rate is

35 per cent. Compute the yield to maturity and the after

tax cost of debenture.

The present value factors at 15% and 17% per p.a.

are as given below:

Solution:(b) Shortcut Method to Compute Cost of

Redeemable Debt:

In order to avoid the complex calculations of hit and

trial method, we can compute the approximate cost

of redeemable debt by using the following simple

formula:

(i) Before-tax cost of redeemable debt,

where, I = Annual Interest

n = Number of years in which debt is to be redeemed

RV = Redeemable value of debt

NP = Net proceeds of debentures

(ii) After-tax cost of redeemable debtWhere, I = Annual interest

t = Tax rate

n = Number of years in which debt is to be redeemed

RV = Redeemable value of debt

NP = Net proceeds of debentures

Illustration 3:

A company issues Rs. 10,00,000 10% redeemable

debentures at a discount of 5%. The costs of floatation

amount to Rs. 30,000. The debentures are redeemable

after 5 years. Calculate before-tax and after-tax cost of

debt assuming a tax rate of 50%.

Solution:

Illustration 4:

A 5-year Rs. 100 debenture of a firm can be sold for a net

price of Rs. 96.50. The coupon rate of interest is 14 per

cent per annum, and the debenture will be redeemed at 5

per cent premium on maturity. The firm’s tax rate is 40

per cent. Compute the after-tax cost of debenture.

Solution:Illustration 5:

Assuming that a firm pays tax at 50% rate, compute

the after tax cost of debt capital in the following

cases:

(i) A perpetual bond sold at par, coupon rate of interest

being 7%;

(ii) A 10 year, 8% Rs. 1.000 per bond sold at Rs. 950 less

4% underwriting commission.

Solution:

iii. Cost of Debt Redeemable in Installments:Financial institutions generally require principal to be

amortised in installments. A company may also issue a

bond or debenture to be redeemed periodically. In such a

case, principal amount is repaid each period instead of a

lump sum at maturity and hence cash outflows each

period include interest and principal. The amount of

interest goes on decreasing each period as it is calculated

on the outstanding amount of debt.

The before-tax cost of such a debt can be calculated

as below:

Illustration 6:

A company is proposing to issue a 5-year debenture of Rs.

1000 at 14 per cent rate of interest per annum. The

debenture amount will be amortised equally over its life.

If the present value of the debenture for an investor is Rs.

1046.59, calculate the minimum required rate of return

or the cost of debt.

Solution:

iv. Cost of Existing Debt:If a firm wants to compute the current cost of its existing

debt, the current market yield of the debt should be

taken into consideration.

Suppose a firm has 10% debentures of Rs. 100 each

outstanding on January 1, 2006 to be redeemed on

December 31, 2012 and the new debentures could

be issued at a net realisable price of Rs. 90 in the

beginning of 2008, the current cost of existing debt

may be computed as:

v. Cost of Zero Coupon Bonds:

Sometimes companies issue bonds or debentures at a

discount from their eventual maturity value and having

zero interest rate. No interest is payable on such

debentures before their redemption and at the time of

redemption the maturity value of the bond is to be paid to

the investors.

The cost of such debt can be calculated by finding

the present values of cash flows as below:

(i) Prepare the cash flow table using an arbitrary

assumed discount rate to discount the cash flows to the

present value.

(ii) Find out the net present value by deducting the

present value of the outflows from the present value of

the inflows.

(iii) If the net present value is positive, apply higher rate

of discount.

(iv) If the higher discount rate still gives a positive net

present value, increase the discount rate further until the

NPV becomes negative.(v) If the NPV is negative at this higher rate, the cost of

debt must be between these two rates.

The following illustration explains the procedure of

determining the cost of zero coupon bonds.

Illustration 7:

X Ltd. has issued redeemable zero coupon bonds of Rs.

100 each at a discount rate of Rs. 60 repayable at the end

of fourth year. Calculate the cost of debt.

Solution:

vi. Floating or Variable Rate Debt:

The interest on floating rate debt changes depending

upon the market rate of interest payable on gilt edged

securities or the prime lending rate of the bank. For

example, suppose a company raises debt from external

sources on the terms of prime lending rate of the bank

plus four per cent.

If the prime lending rate of the bank is 8% p.a., the

company will have to pay interest at the rate of 12% p.a.

Further, if the prime lending rate falls to 6% p.a., the

company shall pay interest at only 10% p.a.

Illustration 8:

ABC Ltd. raised a debt of? 50 lakhs on the terms that

interest shall be payable at prime lending rate of bank

plus three percent. The prime lending rate of the bank is7 per cent. Calculate the cost of debt assuming that the

corporate rate of tax is 35%.

Solution:

vii. Real or Inflation Adjusted Cost of Debt:

In the days of inflation, the real cost of debt is much less

than the nominal cost as the fixed amount is payable

irrespective of the fall in the value of money because of

price level changes. The real cost of debt can be

calculated as below:

Real Cost of Debt = 1 + Nominal Cost of Debt/1 +

Inflation Rate

Illustration 9:

Excel Ltd. has issued 5000 10% Debentures of Rs. 100

each. The rate of inflation is 6%. Calculate the real cost

of debt.

Solution:

Finance: Source # 2. Cost of Preference Capital:

A fixed rate of divided is payable on preference shares.

Though dividend is payable at the discretion of the Board

of directors and there is no legal binding to pay dividend,

yet it does not mean that preference capital is cost free.

The cost of preference capital is a function of dividend

expected by its investors, i.e., its stated dividend.

In case dividends are not paid to preference

shareholders, it will affect the fund raising capacity of the

firm. Hence, dividends are usually paid regularly onpreference shares except when there are no profits to

pay dividends.

The cost of preference capital which is perpetual

can be calculated as:

KP = D/P

where KP = Cost of Preference Capital

D = Annual Preference Dividend

P = Preference Share Capital (Proceeds.)

Further, if preference shares are issued at Premium or

Discount or when costs of floatation are incurred to issue

preference shares, the nominal or par value of preference

share capital has to be adjusted to find out the net

proceeds from the issue of preference shares.

In such a case, the cost of preference capital can be

computed with the following formula:

KP = D/NP

It may be noted that as dividends are not allowed to be

deducted in computation of tax, no adjustment is

required for taxes.

Sometimes Redeemable Preference Shares are issued

which can be redeemed or cancelled on maturity date.

The cost of redeemable preference share capital can

be calculated as:

where, Kpr = Cost of Redeemable Preference Shares

D = Annual Preference Dividend

MV = Maturity Value of Preference Shares

NP = Net Proceeds of Preference Shares.

Illustration 10:A company issues 10,000 10% Preference Shares of Rs.

100 each. Cost of issue is Rs. 2 per share. Calculate cost

of preference capital if these shares are issued (a) at par,

(b) at a premium of 10%, and (c) at a discount of 5%.

Solution:

Illustration 11:

A company issues 10,000 10% Preference Shares of Rs.

100 each redeemable after 10 years at a premium of 5%.

The cost of issue is Rs. 2 per share. Calculate the cost of

preference capital.

Solution:

Illustration 12:

A company issues 1,000 7% Preference Shares of Rs. 100

each at a premium of 10% redeemable after 5 years at

par. Compute the cost of preference capital.

Solution:Finance: Source # 3. Cost of Equity Share Capital:

The cost of equity is the ‘maximum rate of return that the

company must earn on equity financed portion of its

investments in order to leave unchanged the market

price of its stock.’ The cost of equity capital is a function

of the expected return by its investors.

The cost of equity is not the out-of-pocket cost of using

equity capital as the equity shareholders are not paid

dividend at a fixed rate every year. Moreover, payment of

dividend is not a legal binding. It may or may not be paid.

But it does not mean that equity share capital is a cost

free capital. Shareholders invest money in equity shares

on the expectation of getting dividend and the company

must earn this minimum rate so that the market price of

the shares remains unchanged. Whenever a company

wants to raise additional funds by the issue of new equity

shares, the expectations of the shareholders have to

evaluate.

The cost of equity share capital can be computed in

the following ways:

(a) Dividend Yield Method or Dividend/Price Ratio

Method:

According to this method, the cost of equity capital is the

‘discount rate that equates the present value of expected

future dividends per share with the net proceeds (or

current market price) of a share’.

Symbolically:Ke = D/NP or D/MP

where, Ke = Cost of Equity Capital

D = Expected dividend per share

NP = Net proceeds per share and

MP = Market Price per share.

The basic assumptions underlying this method are that

the investors give prime importance to dividends and risk

in the firm remains unchanged.

The dividend price ratio method does not seem to

consider the growth in dividend:

(i) It does not consider future earnings or retained

earnings, and

(ii) It does not take into account the capital gains.

This method of computing cost of equity capital is

suitable only when the company has stable earnings and