ECON 1002: Microeconomics

Final

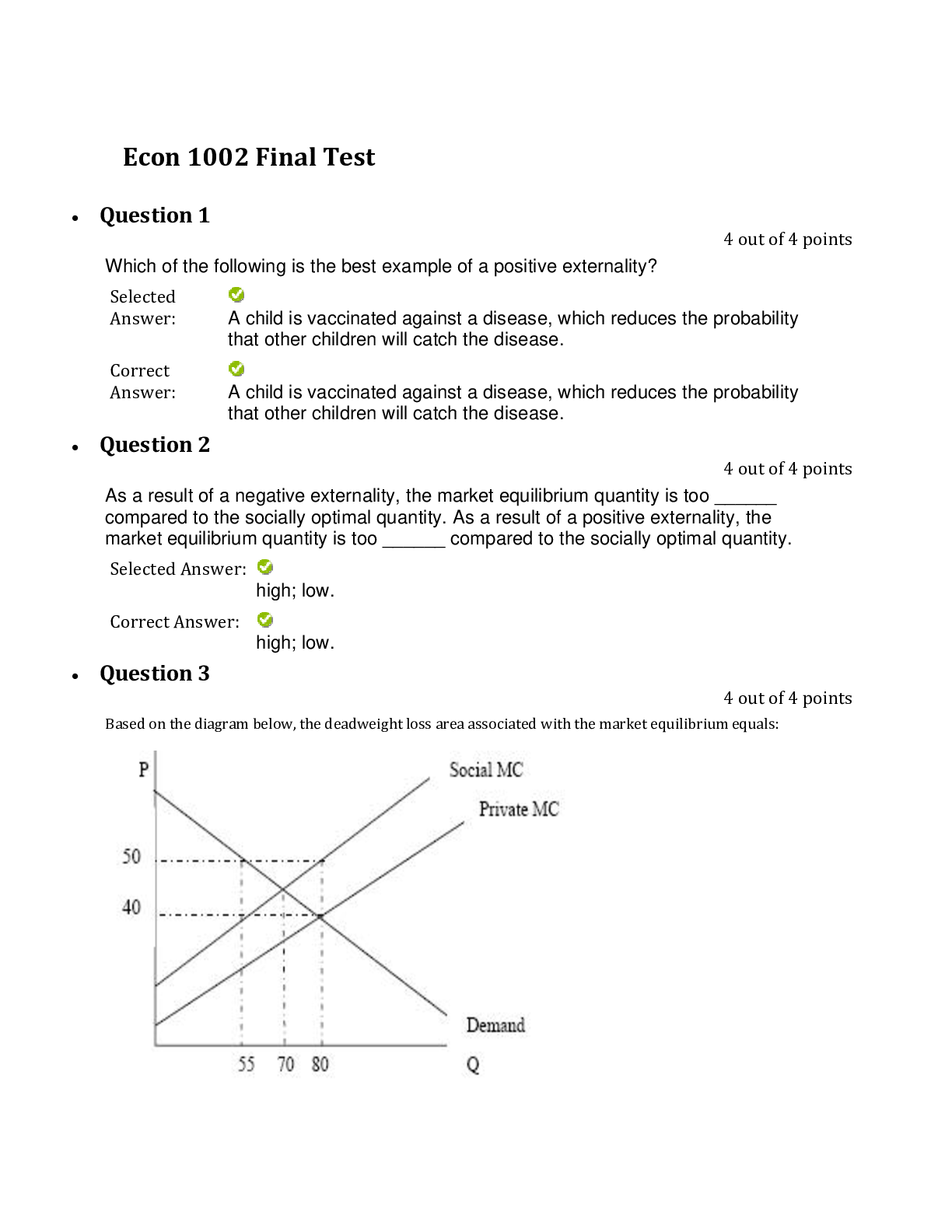

1. The main determinant of elasticity of supply is the:

A. number of close substitutes for the product available to consumers.

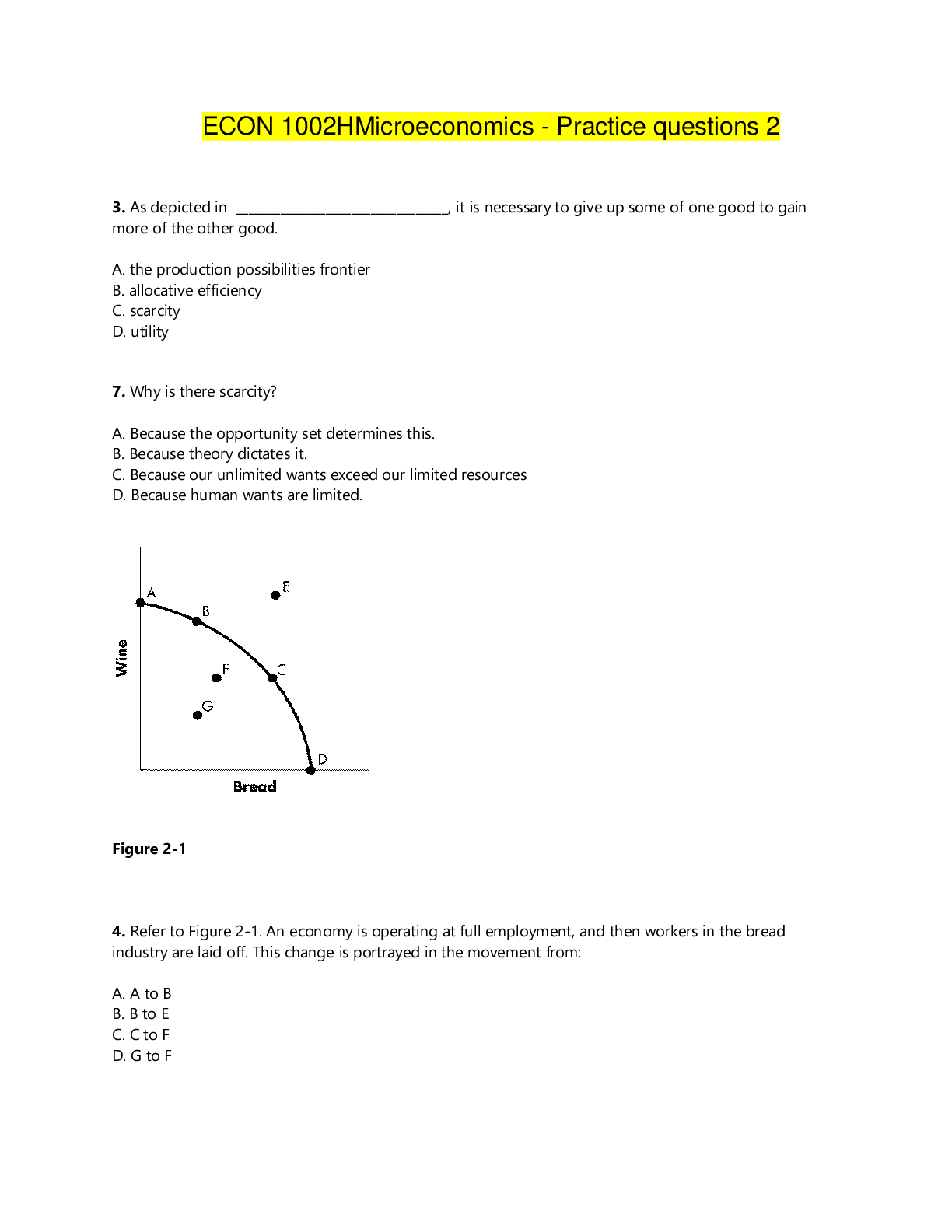

B. amount of time the producer has to adjust input

...

ECON 1002: Microeconomics

Final

1. The main determinant of elasticity of supply is the:

A. number of close substitutes for the product available to consumers.

B. amount of time the producer has to adjust inputs in response to a price change.

C. urgency of consumer wants for the product.

D. number of uses for the product.

Use the following table to answer question 2

2. Refer to the table. Over the $6-$4 price range, supply is:

A. perfectly elastic.

B. elastic.

C. perfectly inelastic.

D. inelastic.

3. The supply of product X is inelastic (but not perfectly inelastic) if the price of X rises by:

A. 5 percent and quantity supplied rises by 7 percent.

B. 8 percent and quantity supplied rises by 8 percent.

C. 10 percent and quantity supplied remains the same.

D. 7 percent and quantity supplied rises by 5 percent.

4. The elasticity of supply of product X is unitary if the price of X rises by:

A. 5 percent and quantity supplied rises by 7 percent.

B. 8 percent and quantity supplied rises by 8 percent.

C. 10 percent and quantity supplied stays the same.

D. 7 percent and quantity supplied rises by 5 percent.

5. The supply of product X is perfectly inelastic if the price of X rises by:

A. 5 percent and quantity supplied rises by 7 percent.

B. 8 percent and quantity supplied rises by 8 percent.

C. 10 percent and quantity supplied stays the same.

D. 7 percent and quantity supplied rises by 5 percent.

6. It takes a considerable amount of time to increase the production of pork. This implies that:

A. a change in the demand for pork will not affect its price in the short run.

B. the short-run supply curve for pork is less elastic than the long-run supply curve for pork.

C. an increase in the demand for pork will elicit a larger supply response in the short run than in the long run.

D. the long-run supply curve for pork is less elastic than the short-run supply curve for pork.

7. Suppose that the price of product X rises by 20 percent and the quantity supplied of X increases by 15 percent. The coefficient of price elasticity of supply for good X is:

A. negative and therefore X is an inferior good.

B. positive and therefore X is a normal good.

C. less than 1 and therefore supply is inelastic.

D. more than 1 and therefore supply is elastic.

8. If the supply of product X is perfectly elastic, an increase in the demand for it will increase:

A. equilibrium quantity but reduce equilibrium price.

B. equilibrium quantity, but equilibrium price will be unchanged.

C. equilibrium price but reduce equilibrium quantity.

D. equilibrium price, but equilibrium quantity will be unchanged.

9. A supply curve that is a vertical straight line indicates that:

A. production costs for this product cannot be calculated.

B. the relationship between price and quantity supplied is inverse.

C. a change in price will have no effect on the quantity supplied.

D. an unlimited amount of the product will be supplied at a constant price.

10. A supply curve that is parallel to the horizontal axis suggests that:

A. the industry is organized monopolistically.

B. the relationship between price and quantity supplied is inverse.

C. a change in demand will change price in the same direction.

D. a change in demand will change the equilibrium quantity but not price.

11. The price of old baseball cards rises rapidly with increases in demand because:

A. the supply of old baseball cards is price inelastic.

B. the supply of old baseball cards in price elastic.

C. the demand for old baseball cards is price inelastic.

D. the demand for old baseball cards is price elastic.

12. Suppose the income elasticity of demand for toys is +2.00. This means that:

A. a 10 percent increase in income will increase the purchase of toys by 20 percent.

B. a 10 percent increase in income will increase the purchase of toys by 2 percent.

C. a 10 percent increase in income will decrease the purchase of toys by 2 percent.

D. toys are an inferior good.

13. If the income elasticity of demand for lard is -3.00, this means that:

A. lard is a substitute for butter.

B. lard is a normal good.

C. lard is an inferior good.

D. more lard will be purchased when its price falls.

14. Cross elasticity of demand measures how sensitive purchases of a specific product are to changes in:

A. the price of some other product.

B. the price of that same product.

C. income.

D. the general price level.

15. The larger the positive cross elasticity coefficient of demand between products X and Y, the:

A. stronger their complementariness.

B. greater their substitutability.

C. smaller the price elasticity of demand for both products.

D. the less sensitive purchases of each are to increases in income.

16. We would expect the cross elasticity of demand between Pepsi and Coke to be:

A. positive, indicating normal goods.

B. positive, indicating inferior goods.

C. positive, indicating substitute goods.

D. negative, indicating substitute goods.

17. We would expect the cross elasticity of demand between dress shirts and ties to be:

A. positive, indicating normal goods.

B. positive, indicating complementary goods.

C. negative, indicating substitute goods.

D. negative, indicating complementary goods.

18. Compared to coffee, we would expect the cross elasticity of demand for:

A. tea to be negative, but positive for cream.

B. tea to be positive, but negative for cream.

C. both tea and cream to be negative.

D. both tea and cream to be positive.

19. Suppose that a 10 percent increase in the price of normal good Y causes a 20 percent increase in the quantity demanded of normal good X. The coefficient of cross elasticity of demand is:

A. negative and therefore these goods are substitutes.

B. negative and therefore these goods are complements.

C. positive and therefore these goods are substitutes.

D. positive and therefore these goods are complements.

20. Suppose that a 20 percent increase in the price of normal good Y causes a 10 percent decline in the quantity demanded of normal good X. The coefficient of cross elasticity of demand is:

A. negative and therefore these goods are substitutes.

B. negative and therefore these goods are complements.

C. positive and therefore these goods are substitutes.

D. positive and therefore these goods are complements.

21. Assume that a 4 percent increase in income across the economy produces an 8 percent increase in the quantity demanded of good X. The coefficient of income elasticity of demand is:

A. negative and therefore X is an inferior good.

B. negative and therefore X is a normal good.

C. positive and therefore X is an inferior good.

D. positive and therefore X is a normal good.

22. Assume that a 6 percent increase in income in the economy produces a 3 percent increase in the quantity demanded of good X. The coefficient of income elasticity of demand is:

A. negative and therefore X is an inferior good.

B. positive but less than one; therefore X is an inferior good.

C. positive and therefore X is an inferior good.

D. positive and therefore X is a normal good.

23. Assume that a 3 percent increase in income across the economy produces a 1 percent decline in the quantity demanded of good X. The coefficient of income elasticity of demand for good X is:

A. negative and therefore X is an inferior good.

B. negative and therefore X is a normal good.

C. positive and therefore X is an inferior good.

D. positive and therefore X is a normal good.

24. Which type of goods is most adversely affected by recessions?

A. Goods for which the income elasticity coefficient is relatively low or negative.

B. Goods for which the income elasticity coefficient is relatively high and positive.

C. Goods for which the cross elasticity coefficient is positive.

D. Goods for which the cross elasticity coefficient is negative.

25. Which of the following goods will least likely suffer a decline in demand during a recession?

A. Dinner at a nice restaurant

B. iPods

C. Toothpaste

D. Plasma screen and LCD TVs

26. Economic cost can best be defined as:

A. any contractual obligation that results in a flow of money expenditures from an enterprise to resource suppliers.

B. any contractual obligation to labor or material suppliers.

C. a payment that must be made to obtain and retain the services of a resource.

D. all costs exclusive of payments to fixed factors of production.

27. Which of the following constitutes an implicit cost to the Johnston Manufacturing Company?

A. Payments of wages to its office workers.

B. Rent paid for the use of equipment owned by the Schultz Machinery Company.

C. Use of savings to pay operating expenses instead of generating interest income.

D. Economic profits resulting from current production.

28. Production costs to an economist:

A. consist only of explicit costs.

B. reflect opportunity costs.

C. never reflect monetary outlays.

D. always reflect monetary outlays.

29. Implicit and explicit costs are different in that:

A. explicit costs are opportunity costs; implicit costs are not.

B. implicit costs are opportunity costs; explicit costs are not.

C. the latter refer to nonexpenditure costs and the former to monetary payments.

D. the former refer to nonexpenditure costs and the latter to monetary payments.

Use the following information to answer questions 30 and 31

The cost information for the Creamy Crisp Donut Company:

Entrepreneur's potential earnings as a salaried worker = $50,000

Annual lease on building = $22,000

Annual revenue from operations = $380,000

Payments to workers = $120,000

Utilities (electricity, water, disposal) costs = $8,000

Value of entrepreneur's talent in the next best entrepreneurial activity = $80,000

Entrepreneur's forgone interest on personal funds used to finance the business = $6,000

30. Refer to the data for the Creamy Crisp Donut Company. Creamy Crisp's accounting profit is:

A. $150,000.

B. $380,000.

C. $230,000.

D. $294,000.

31. Refer to the data for the Creamy Crisp Donut Company. Creamy Crisp's economic profit is:

A. $150,000.

B. $80,000.

C. $230,000.

D. $94,000.

32. The basic characteristic of the short run is that:

A. barriers to entry prevent new firms from entering the industry.

B. the firm does not have sufficient time to change the size of its plant.

C. the firm does not have sufficient time to cut its rate of output to zero.

D. a firm does not have sufficient time to change the amounts of any of the resources it employs.

33. The long run is characterized by:

A. the relevance of the law of diminishing returns.

B. at least one fixed input.

C. insufficient time for firms to enter or leave the industry.

D. the ability of the firm to change its plant size.

34. The law of diminishing returns indicates that:

A. as extra units of a variable resource are added to a fixed resource, marginal product will decline beyond some point.

B. because of economies and diseconomies of scale, a competitive firm's long-run average total cost curve will be U-shaped.

C. the demand for goods produced by purely competitive industries is downsloping.

D. beyond some point, the extra utility derived from additional units of a product will yield the consumer smaller and smaller extra amounts of satisfaction.

35. Which of the following best expresses the law of diminishing returns?

A. Because large-scale production allows the realization of economies of scale, the real costs of production vary directly with the level of output.

B. Population growth automatically adjusts to that level at which the average product per worker will be at a maximum.

C. As successive amounts of one resource (labor) are added to fixed amounts of other resources (capital), beyond some point the resulting extra or marginal output will decline.

D. Proportionate increases in the inputs of all resources will result in a less-than-proportionate increase in total output.

Use the table to answer questions 36 and 37

36. Assume that the amounts of all nonlabor resources are fixed.

Refer to the data. The marginal product of the sixth worker is:

A. 180 units of output.

B. 30 units of output.

C. 15 units of output.

D. negative.

37. Assume that the amounts of all nonlabor resources are fixed.

Refer to the data. Average product is at a maximum when:

A. five workers are hired.

B. four workers are hired.

C. three workers are hired.

D. two workers are hired.

38. Marginal product:

A. diminishes at all levels of production.

B. may initially increase, then diminish, but never become negative.

C. may initially increase, then diminish, and ultimately become negative.

D. is always less than average product.

Use the following graph to answer questions 39 and 40

39. In the diagram, curves 1, 2, and 3 represent the:

A. average, marginal, and total product curves respectively.

B. marginal, average, and total product curves respectively.

C. total, average, and marginal product curves respectively.

D. total, marginal, and average product curves respectively.

40. The diagram suggests that:

A. when marginal product is zero, total product is at a minimum.

B. when marginal product lies above average product, average product is rising.

C. when marginal product lies below average product, average product is rising.

D. when total product is at a maximum, so are marginal product and average product.

Use the following table to answer question 41

41. Refer to the data. The marginal product of the fourth worker:

A. is 5.

B. is 7.

C. is 71/2.

D. cannot be calculated from the information given.

Use the graph to answer question 42

42. In the diagram, the range of diminishing marginal returns is:

A. 0Q3.

B. 0Q2.

C. Q1Q2.

D. Q1Q3

Use the following data to answer the question 43

43. Refer to the data. The average product (AP) when two units of labor are hired is:

A. 8.

B. 9.

C. 10.

D. 18.

44. Fixed cost is:

A. the cost of producing one more unit of capital, for example, machinery.

B. any cost that does not change when the firm changes its output.

C. average cost multiplied by the firm's output.

D. usually zero in the short run.

45. If you operated a small bakery, which of the following would be a variable cost in the short run?

A. Baking ovens.

B. Interest on business loans.

C. Annual lease payment for use of the building.

D. Baking supplies (flour, salt, etc.).

46. Which of the following is correct as it relates to cost curves?

A. Average variable cost intersects marginal cost at the latter's minimum point.

B. Marginal cost intersects average total cost at the latter's minimum point.

C. Average fixed cost intersects marginal cost at the latter's minimum point.

D. Marginal cost intersects average fixed cost at the latter's minimum point.

Use the following graph to answer questions 47 and 48

47. Refer to the diagram. The vertical distance between ATC and AVC reflects:

A. the law of diminishing returns.

B. the average fixed cost at each level of output.

C. marginal cost at each level of output.

D. the presence of economies of scale.

48. If a firm decides to produce no output in the short run, its costs will be:

A. its marginal costs.

B. its variable costs.

C. its fixed costs.

D. zero.

Use the following table to answer questions 49 and 50

49. Refer to the data. The average total cost of producing 3 units of output is:

A. $14.

B. $12.

C. $13.50.

D. $16.

50. Refer to the data. The marginal cost of producing the sixth unit of output is:

A. $24.

B. $12.

C. $16.

D. $8.

Use the following graph to answer question 51

51. In the figure, curves 1, 2, 3, and 4 represent the:

A. ATC, MC, AFC, and AVC curves respectively.

B. MC, AFC, AVC, and ATC curves respectively.

C. MC, ATC, AVC, and AFC curves respectively.

D. ATC, AVC, AFC, and MC curves respectively.

52. Fixed costs are associated with:

A. highly adjustable inputs such as labor.

B. both the short run and the long run.

C. the short run only.

D. the long run only.

Use the following graph to answer question 53

53. In the diagram, curves 1, 2, and 3 represent:

A. average variable cost, marginal cost, and average fixed cost respectively.

B. total variable cost, total fixed cost, and total cost respectively.

C. total fixed cost, total variable cost, and total cost respectively.

D. marginal product, average variable cost, and average total cost respectively.

Use the following graph to answer questions 54 through 56

54. Refer to the short-run production and cost data. In Figure A curve (1) is:

A. total product and curve (2) is average product.

B. total product and curve (2) is marginal product.

C. average product and curve (2) is marginal product.

D. marginal product and curve (2) is average product.

55. Refer to the short-run production and cost data. In Figure B curve (3) is:

A. AVC and curve (4) is MC.

B. MC and curve (4) is AVC.

C. MC and curve (4) is AFC.

D. AFC and curve (4) is MC.

56. Refer to the short-run production and cost data. The curves of Figures A and B suggest that:

A. marginal product and marginal cost reach their maximum points at the same output.

B. marginal cost reaches a minimum where marginal product is at its maximum.

C. marginal cost and marginal product reach their minimum points at the same output.

D. AVC cuts MC at the latter's minimum point.

57. Economies of scale are indicated by:

A. the rising segment of the average variable cost curve.

B. the declining segment of the long-run average total cost curve.

C. the difference between total revenue and total cost.

D. a rising marginal cost curve.

Use the following graph to answer questions 58 and 59

58. Refer to the diagram. Economies of scale:

A. are evident over the entire range of output.

B. develop over the 0Q1 range of output.

C. begin at output Q3.

D. occur only over the Q1Q3 range of output.

59. Refer to the diagram. Constant returns to scale:

A. occur over the 0Q1 range of output.

B. occur over the Q1Q3 range of output.

C. begin at output Q3.

D. are in evidence at all output levels.

60. If a firm increases all of its inputs by 10 percent and its output increases by 10 percent, then:

A. it is encountering diseconomies of scale.

B. it is encountering economies of scale.

C. it is encountering constant returns to scale.

D. the marginal products of all inputs are falling.

[Show More]

.png)

.png)