WALDEN UNIVERSITY NRNP 6568 FINAL EXAM 180 PRACTICE Questions & Answers | With Well Elaborated and Verified Questions |100% Verified solutions | 2026\2027 Latest!!

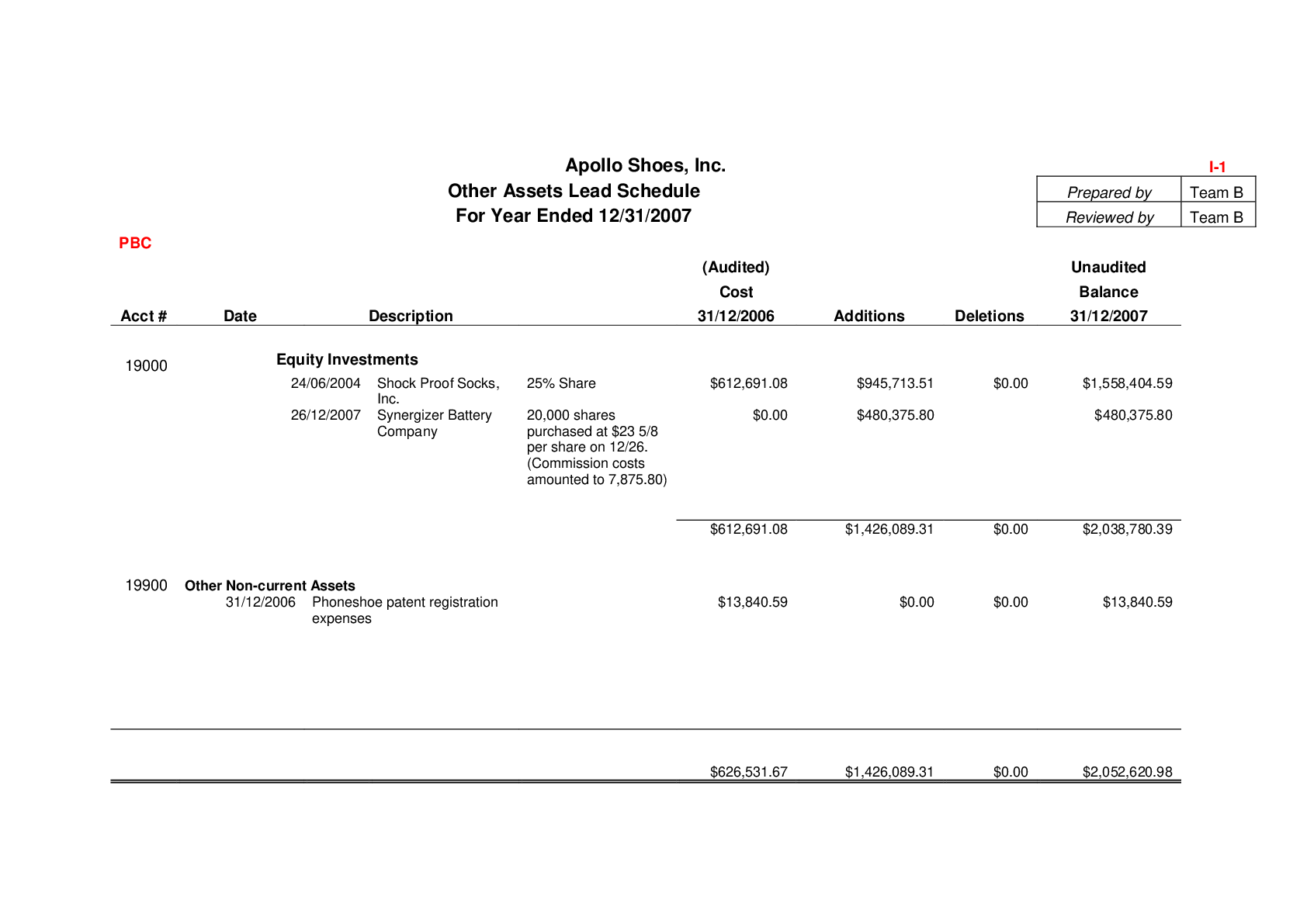

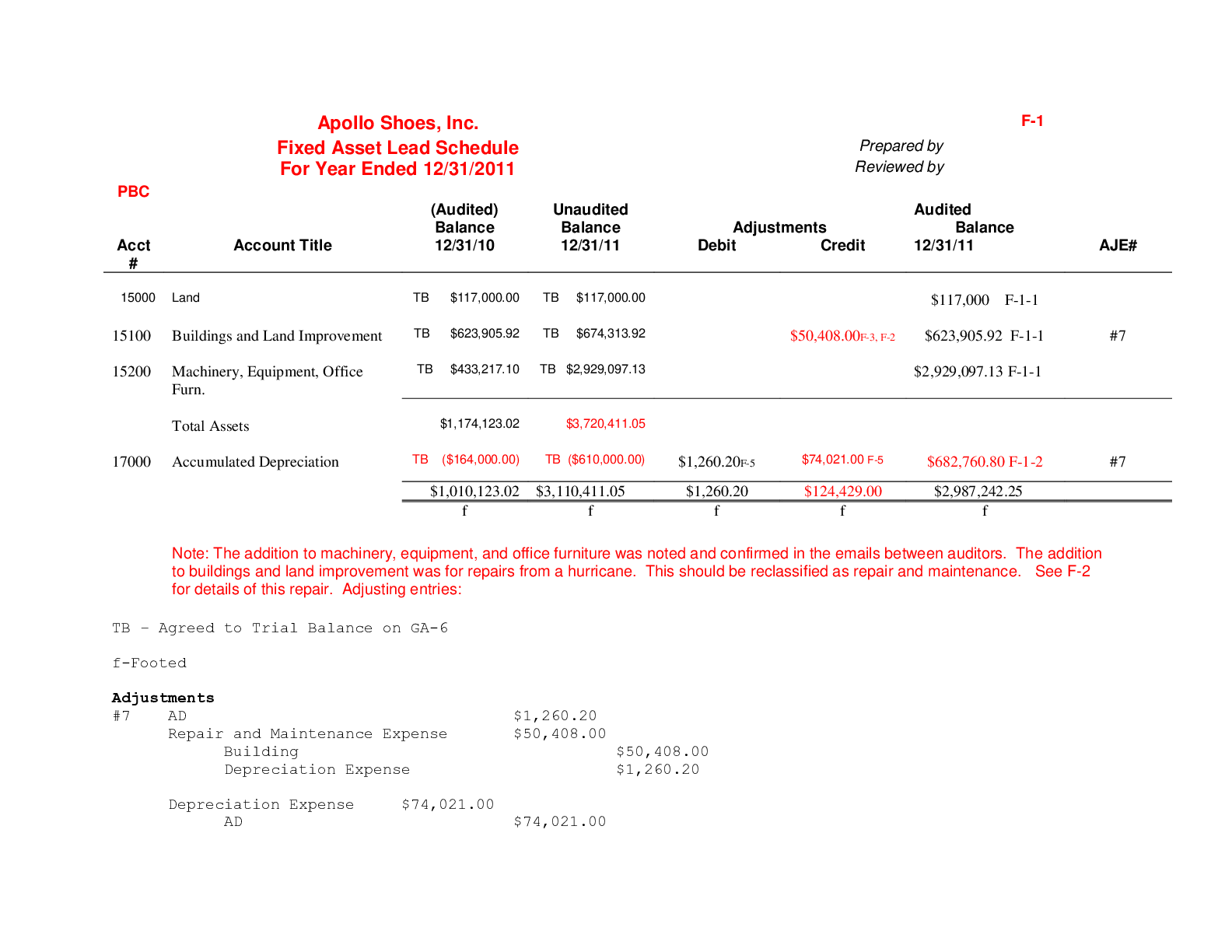

Financial Accounting > CASE STUDY > ACC 3455Fixed Assets Lead Schedule (All)

Last updated: 3 years ago

Preview 1 out of 6 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Connected school, study & course

About the document

Uploaded On

Sep 20, 2020

Number of pages

6

Written in

All

This document has been written for:

Uploaded

Sep 20, 2020

Downloads

0

Views

271

Scholarfriends.com Online Platform by Browsegrades Inc. 651N South Broad St, Middletown DE. United States.

We're available through e-mail, Twitter, and live chat.

FAQ

Questions? Leave a message!

Copyright © Scholarfriends · High quality services·