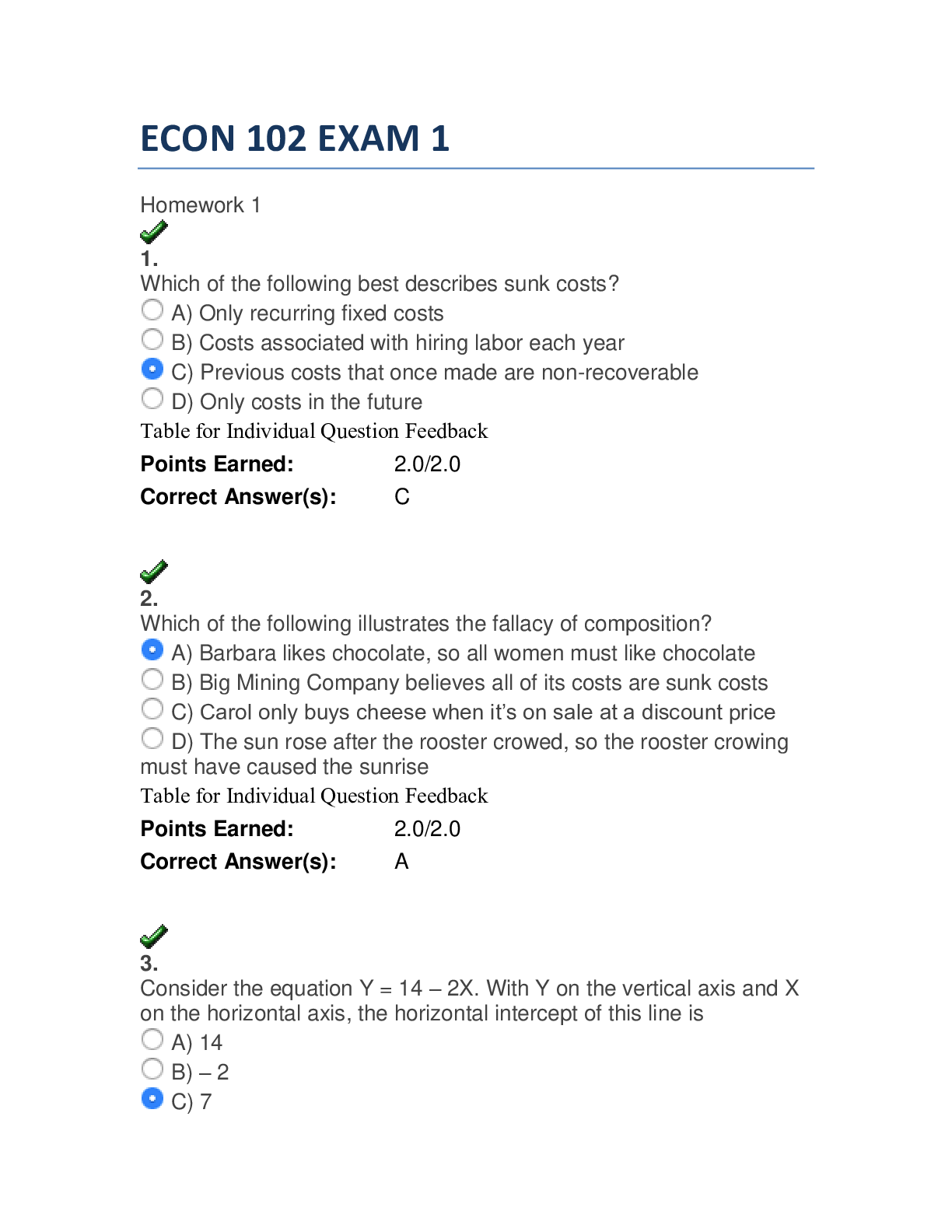

ECON 102 MIDTER EXAM . SCORED 90%. Calculation Solutions Provided.

Document Content and Description Below

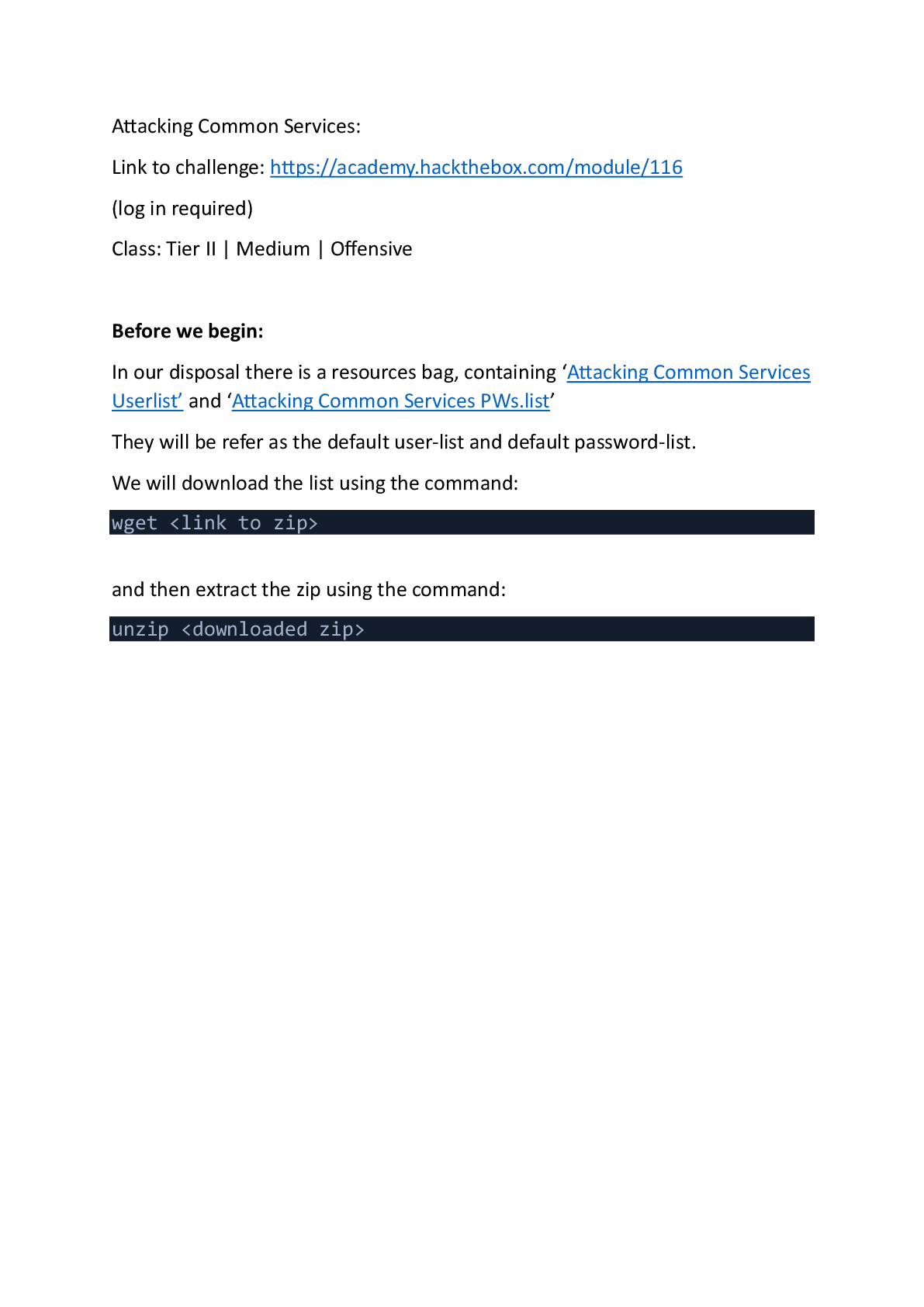

ECON 102 MIDTER EXAM

Points Awarded 54.00

Points Missed 6.00

Percentage 90.0%

1.

A firm’s product price multiplied by the total number of items sold is called

A) profit

B) explicit cost

C) total reve

...

[Show More]

Last updated: 3 years ago

Preview 1 out of 13 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Oct 03, 2020

Number of pages

13

Written in

All

Additional information

This document has been written for:

Uploaded

Oct 03, 2020

Downloads

0

Views

105

Document Keyword Tags

Recommended For You

Get more on EXAM »

$9

65 Pages

Pennsylvania State University - ECON 102 EXAM 1. All Answers I...

$12

99 Pages

ECON 102 Final Exam Quizzes HW Lecture and Transcript. . All...

$10.5

4 Pages

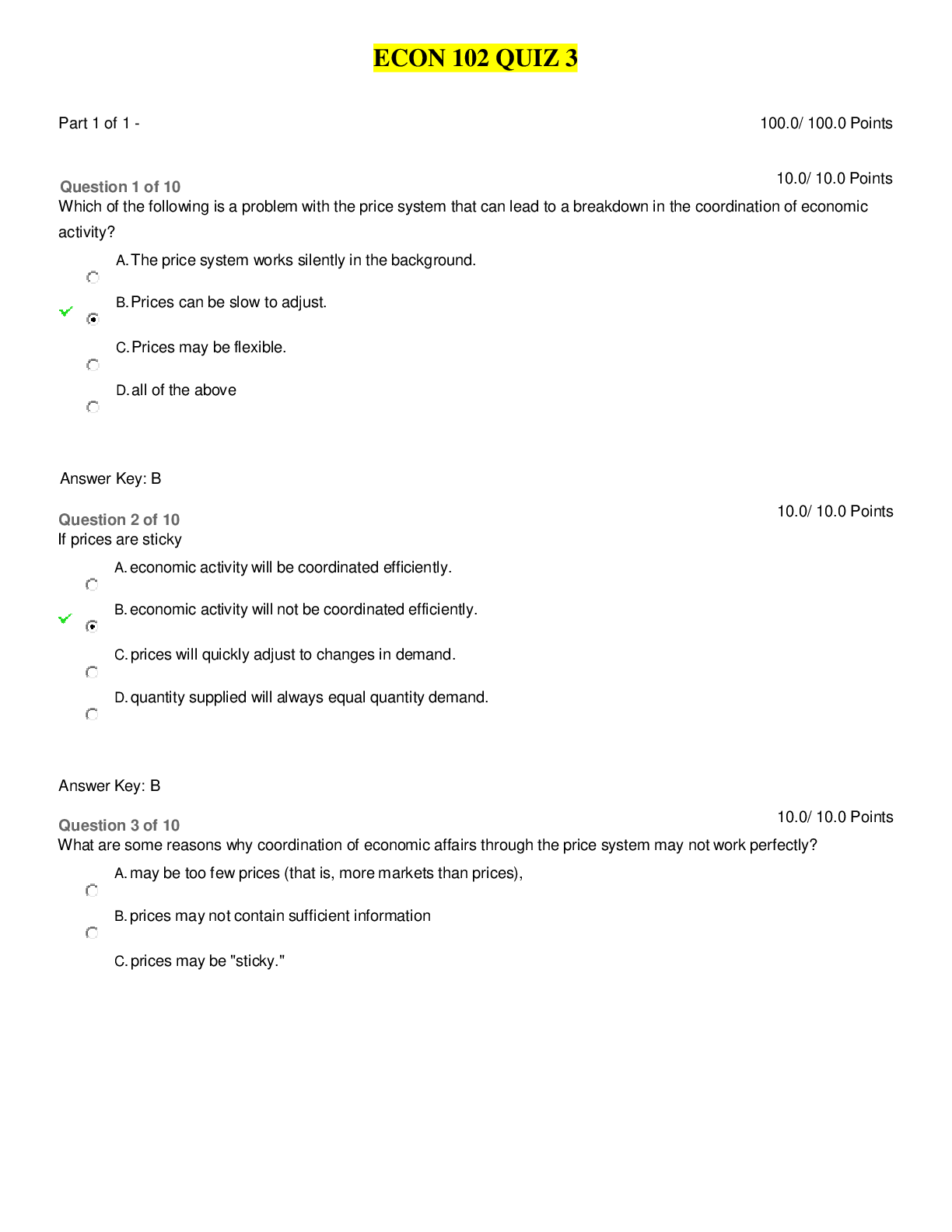

Econ 102 quiz 3 ALL ANSWERS 100% CORRECT SPRING FALL-2022 LATE...

.png)

$11

18 Pages

Cornell Institute of Business & Technology ECON 1023 Arrow's i...

$11

26 Pages

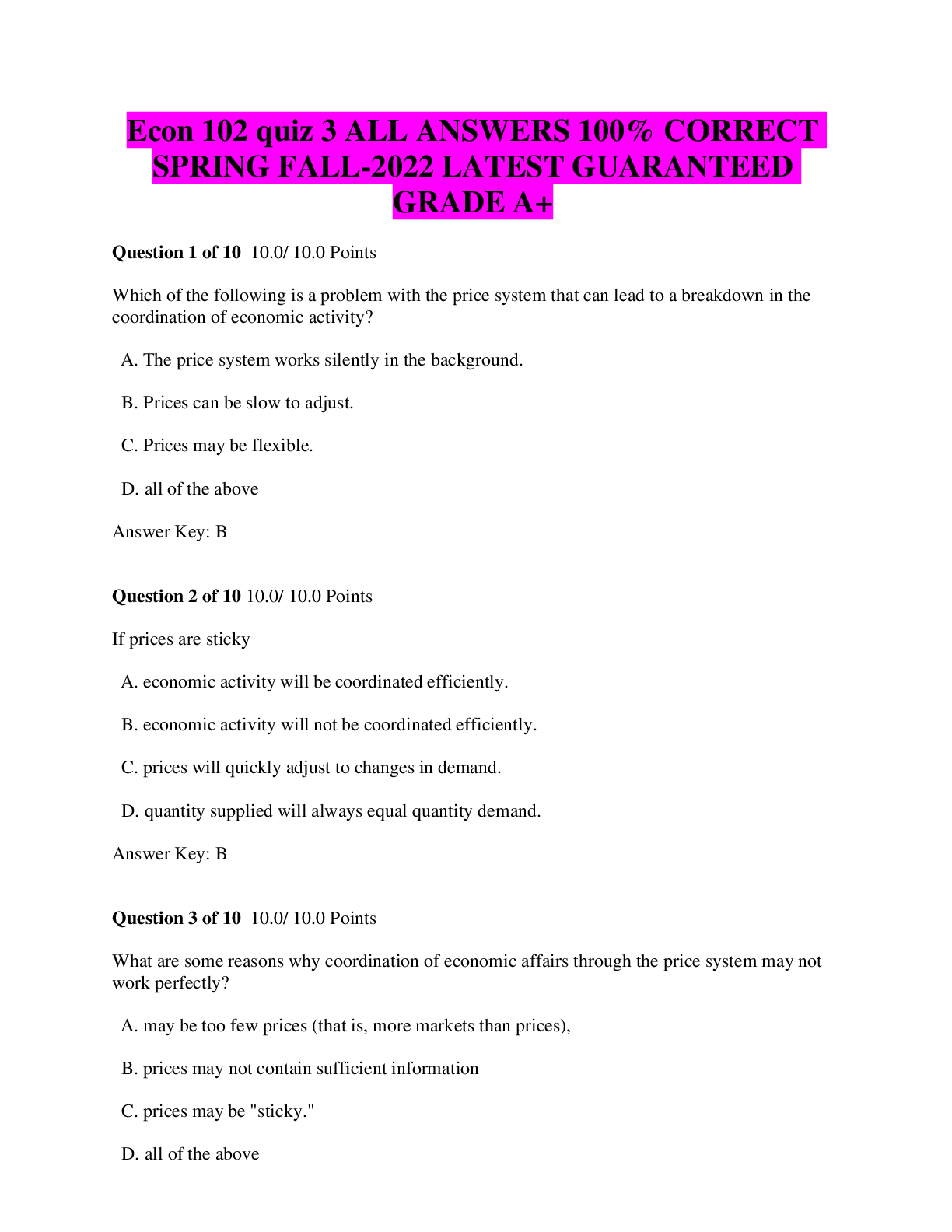

University of Maryland, Baltimore CountyECON 102chapter 2.

$7

5 Pages

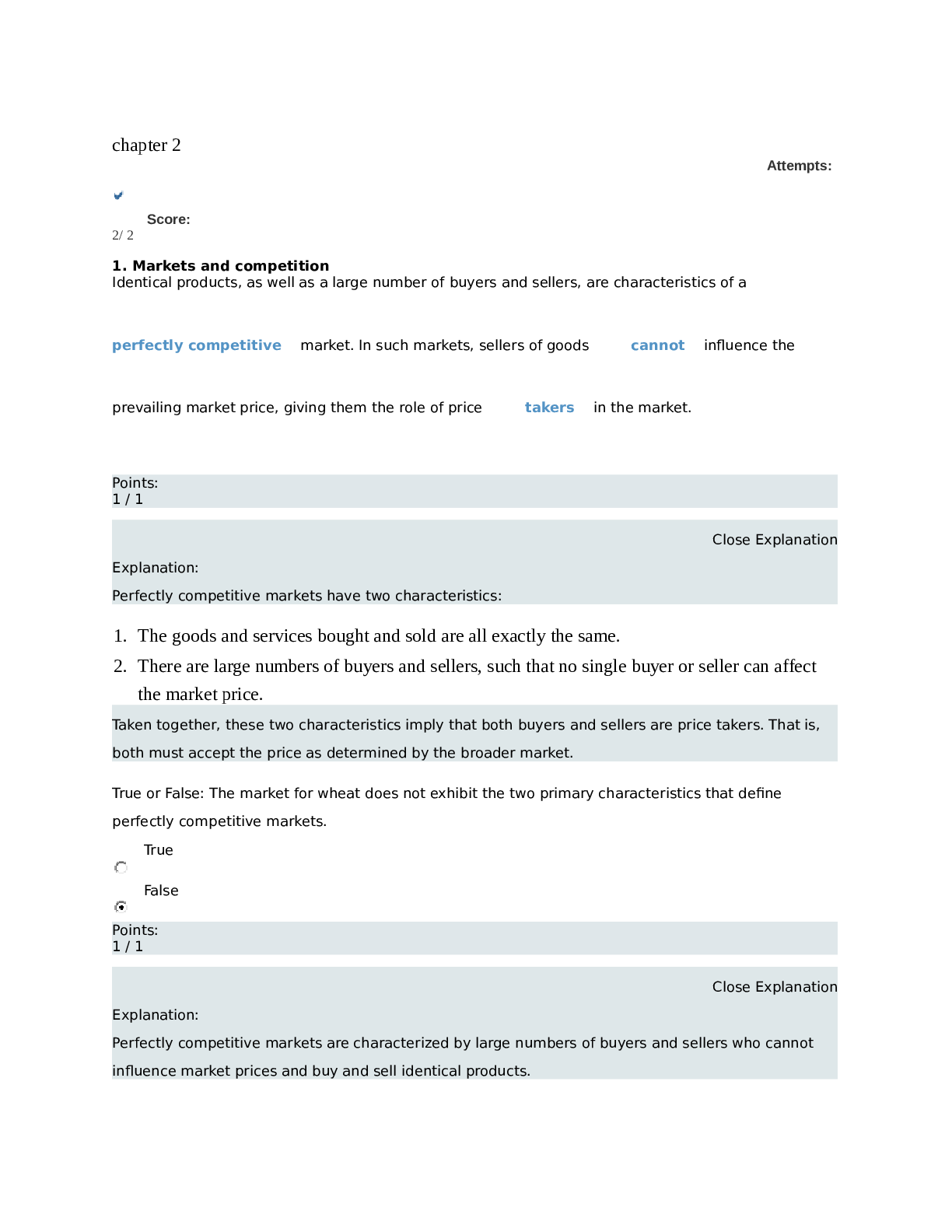

University of California, Los Angeles - ECON 102solutions_ch27

$7

9 Pages

Case Western Reserve University - ECON 102Chapter 7 Review

$9.5

23 Pages

Pennsylvania State University - ECON 102 Homework 05. All the...

$12

5 Pages

SOPHIA ECON102 Unit 2 Milestone Updated/SOPHIA ECON102 Unit 2...

![Preview of Essentials of Econometrics, 5th Edition by Damodar Gujarati [eBook] [PDF]](https://scholarfriends.com/storage/5tQSjcjn2024-12-16-11-2967608dc2076f3.png)

$29

633 Pages

Essentials of Econometrics, 5th Edition by Damodar Gujarati [e...

$25

228 Pages

Essentials of Econometrics, 5th Edition by Damodar Gujarati, D...

.png)

$25

1176 Pages

Microeconomics Theory and Applications, 13e Edgar Browning, Ma...

![Preview of eBook [PDF] International Economics Global Market Competition, 5th Edition By Henry Thomp](https://browseimages.nyc3.digitaloceanspaces.com/paper-images/2026/04/07/S243XLY22026-04-07-10-4769d4b6a30dd86.png)

![Preview of eBook [PDF] Economics Private and Public Choice 18th Edition By James Gwartney, Richard St](https://browseimages.nyc3.digitaloceanspaces.com/paper-images/2026/04/05/r7BNbv8U2026-04-05-04-2969d263a22c575.png)

More related documents below