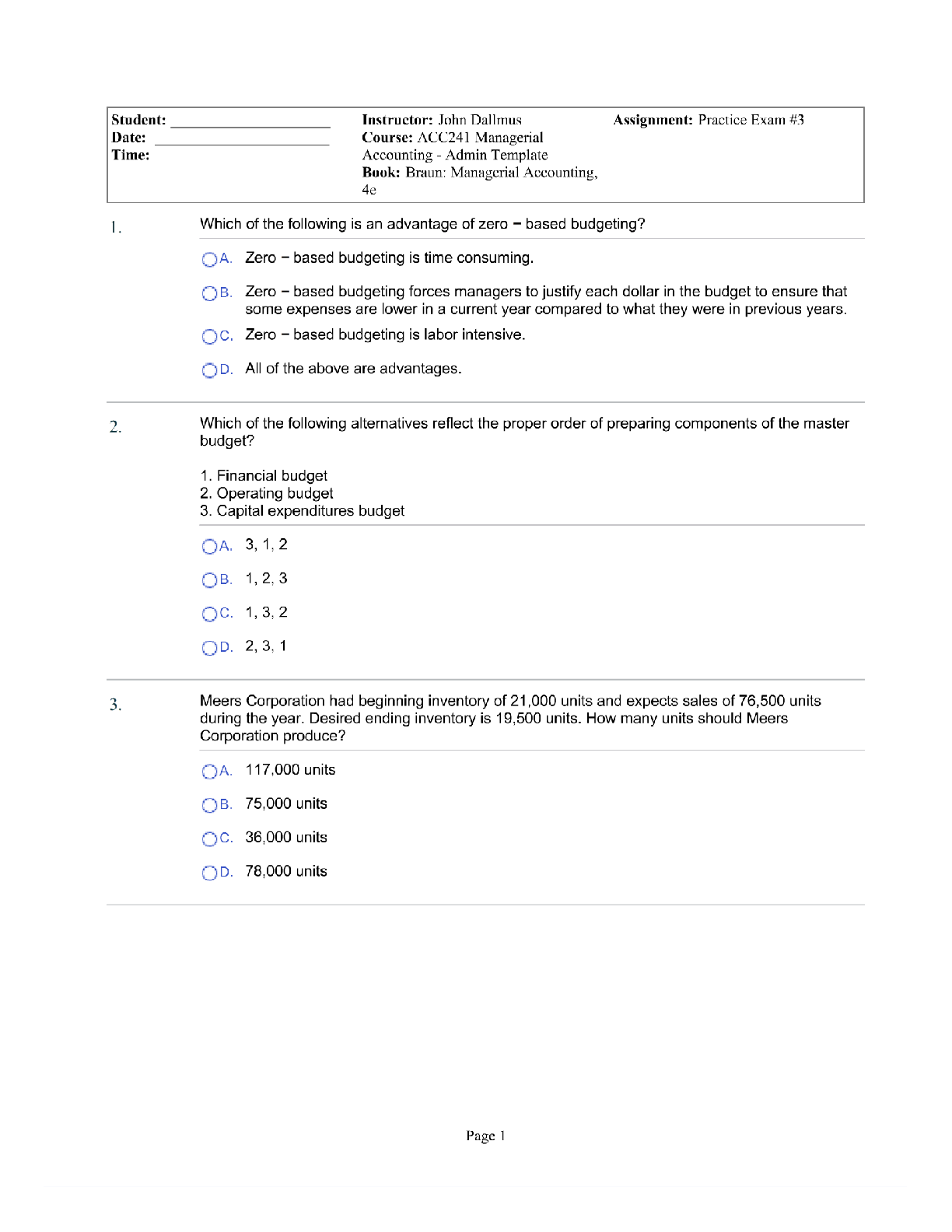

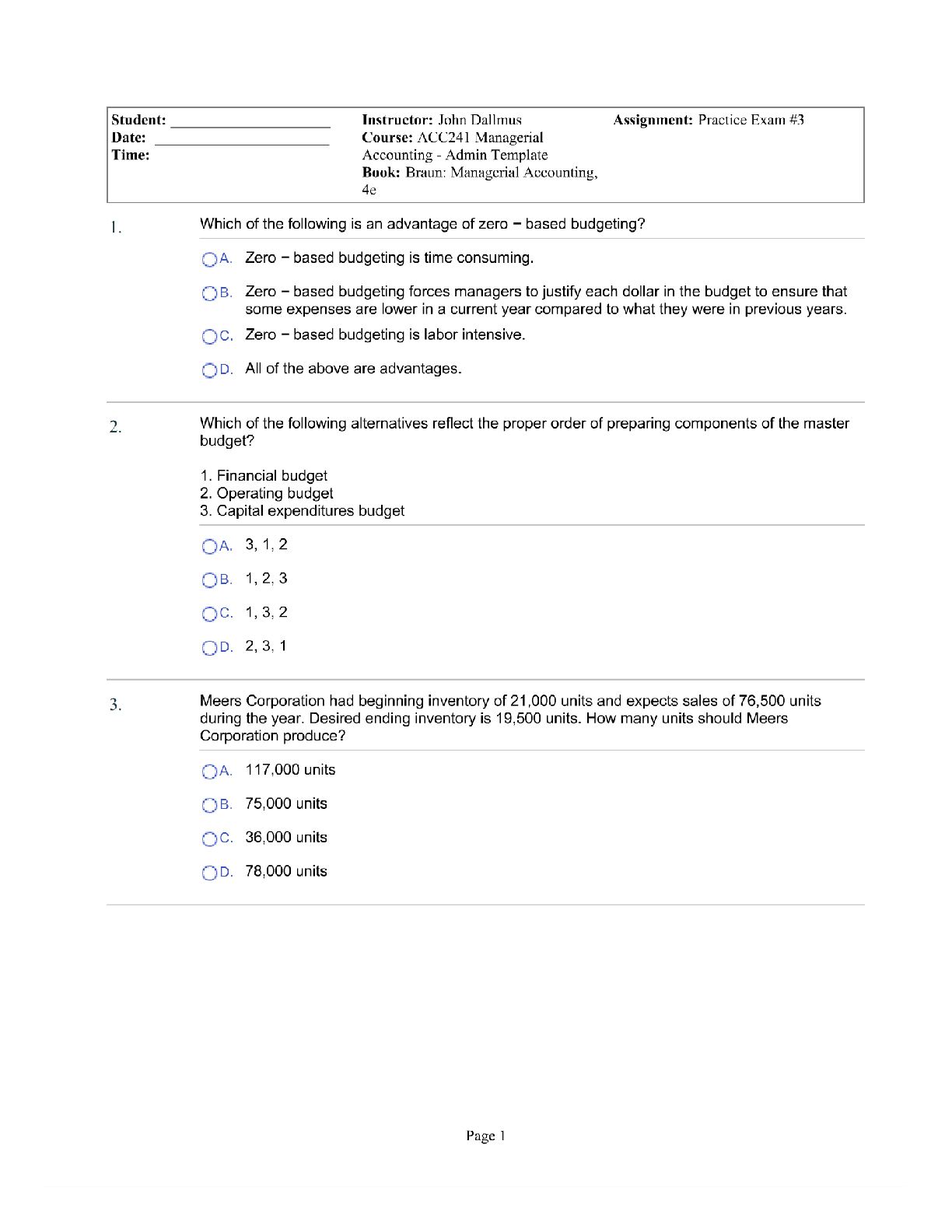

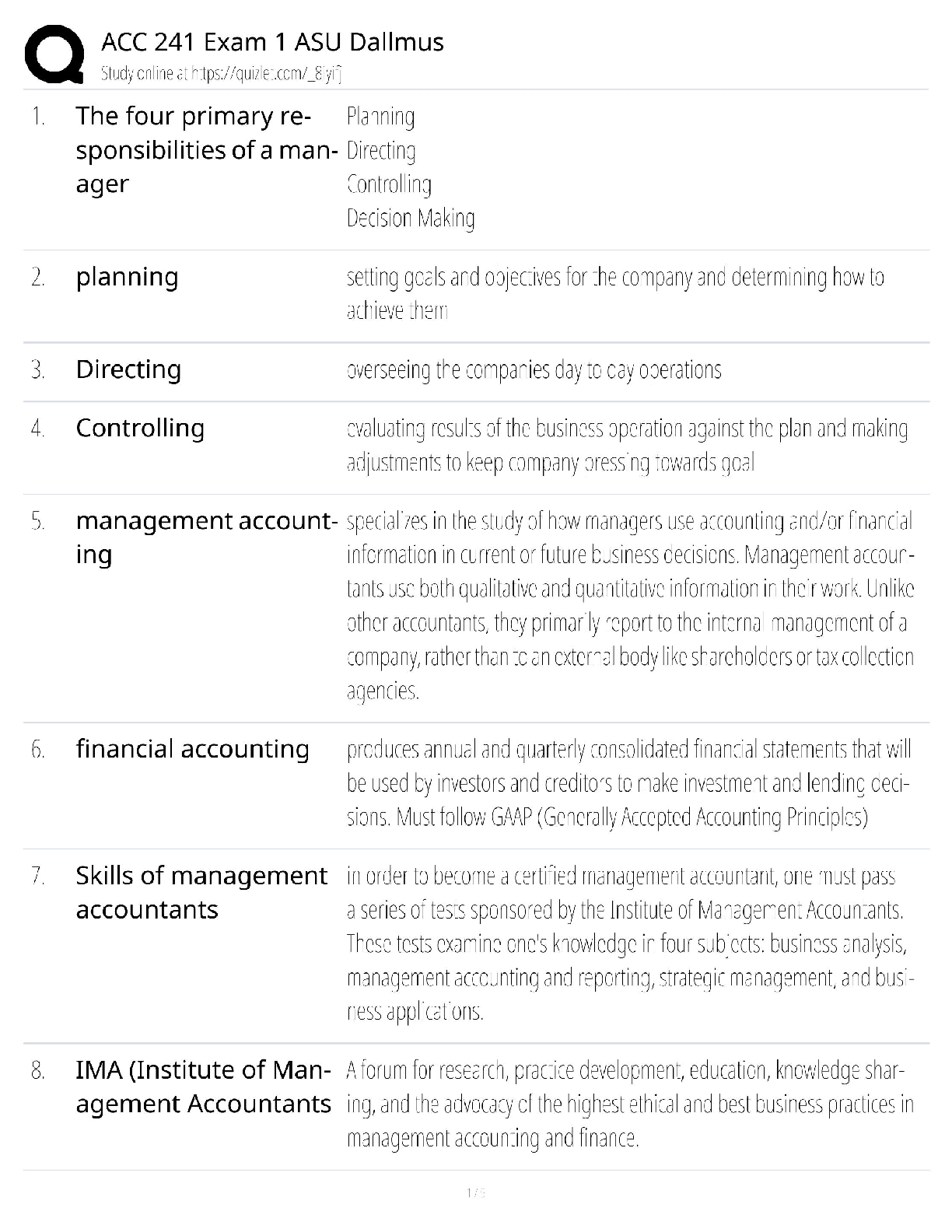

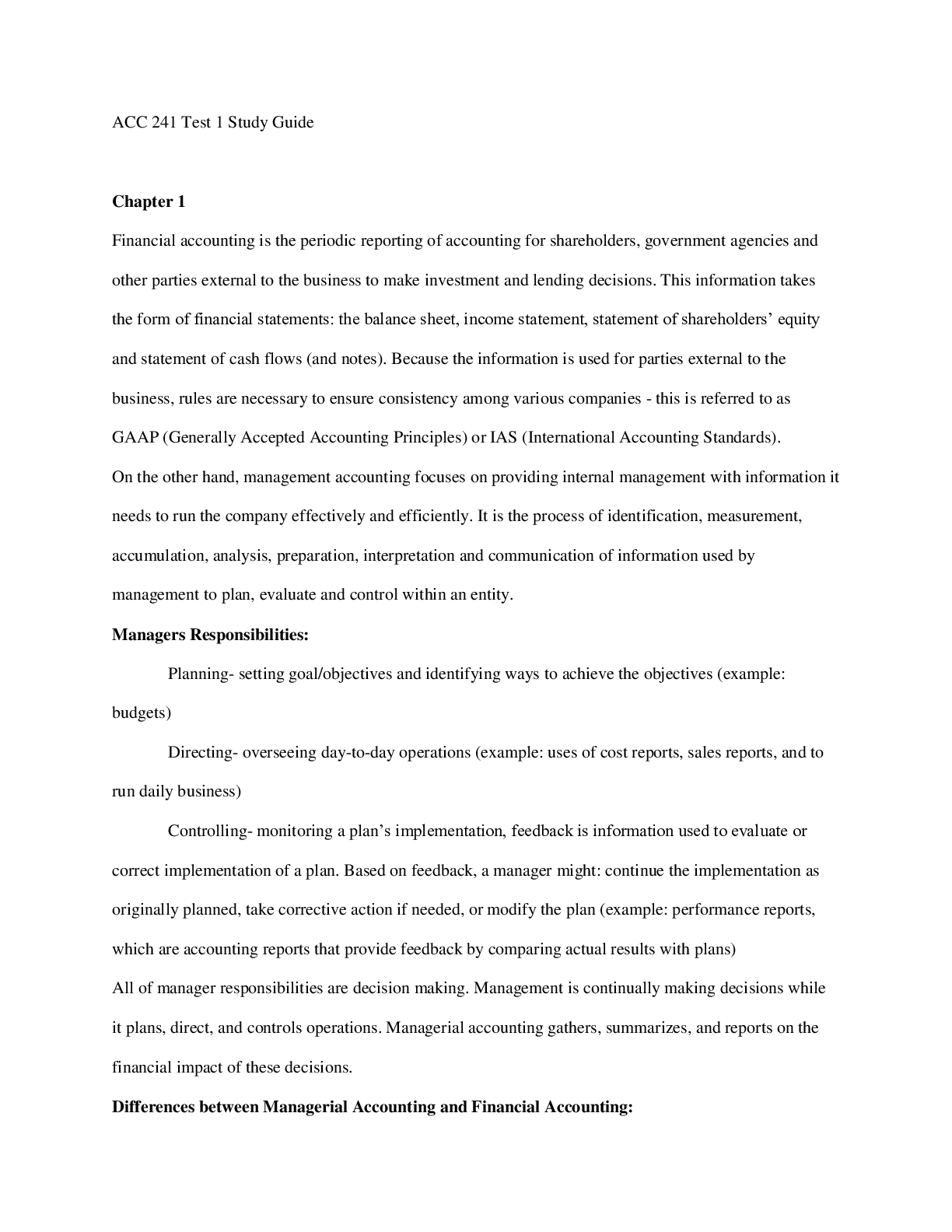

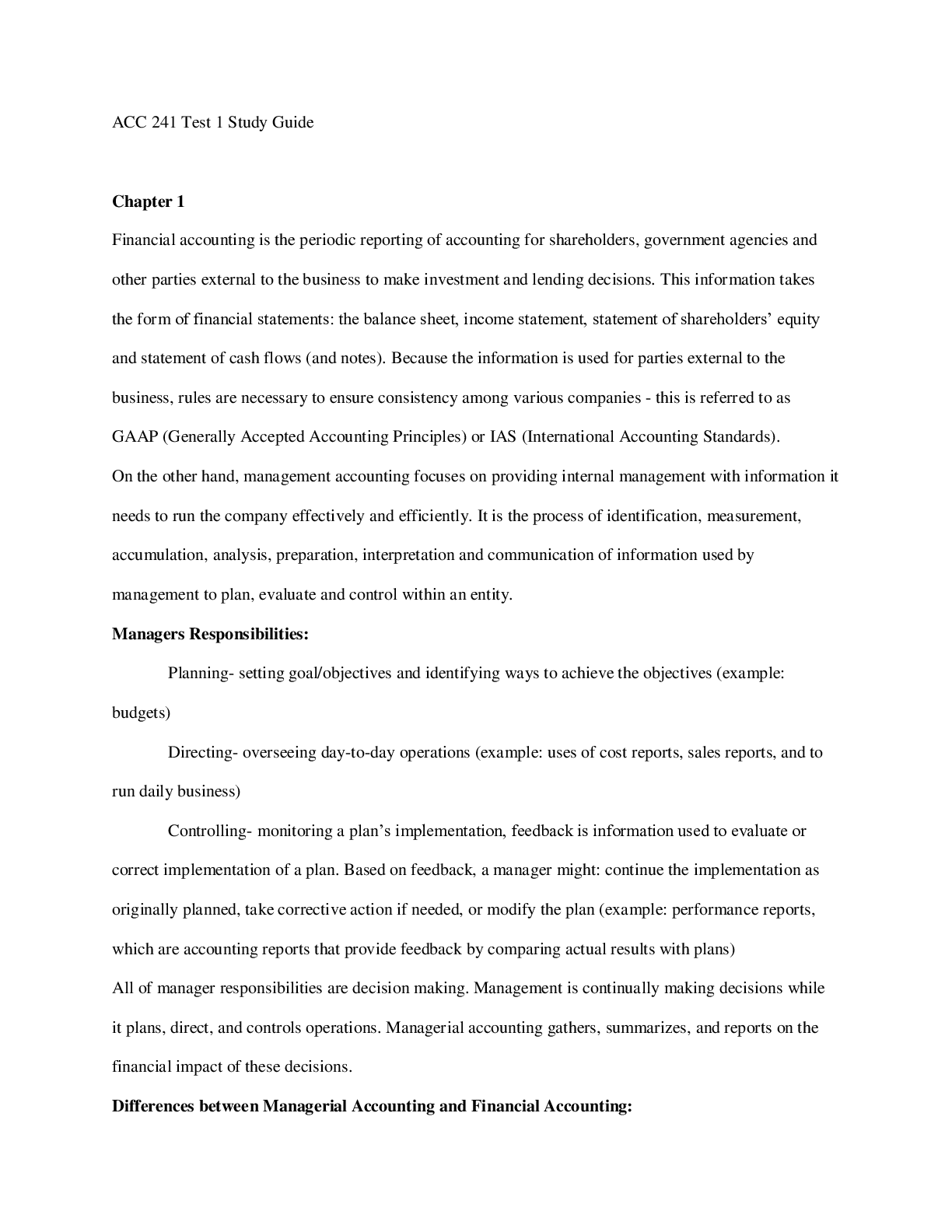

True / False Questions

1. Interim testing is ordinarily done prior to the date of the financial statements.

True False

2. Auditors are not responsible for evaluating the accuracy of management's

estimates but the rea

...

True / False Questions

1. Interim testing is ordinarily done prior to the date of the financial statements.

True False

2. Auditors are not responsible for evaluating the accuracy of management's

estimates but the reasonableness of those estimates.

True False

3. While useful, analytical procedures are not required in the final review stages of

the audit.

True False

4. The existence of "miscellaneous" revenue or expense accounts may signal the

practice of earnings management.

True False

5. Auditors' initial source of information about litigation, claims, and assessments is

the client's attorney.

True False

6. The auditor ordinarily requests the attorney letter directly from the attorneys.

True False

7. Attorneys should always provide a dollar estimate of the amount of potential loss

for items included in the attorney letter.

True False

8. If the attorney's views differ from information provided in the attorney letter, the

attorney is not expected to provide additional explanation to auditors.

True False

9. A primary purpose of obtaining written representations is for management to

acknowledge their responsibility for the fairness of the financial statements.

True False

10.Written representations should be dated as of the date of the financial

statements.

True False

11. If the client refuses to provide written representations, auditors should issue either

a qualified opinion or adverse opinion, depending on the importance of the

omission.

True False

12.The chief executive officer, chief financial officer, or other executive-level client

personnel should sign written representations.

True False

13.It is ultimately the client's responsibility for adjusting the financial statements for

matters identified during the audit.

True False

14.The engagement quality review of audit documentation by a different partner

focuses on whether all appropriate steps in the audit were performed and whether

the referencing among all audit documentation is clear.

True False

15.Roll-forward procedures are normally conducted prior to the date of the financial

statements.

True False

16.Reviewing the latest interim financial statements is one method of identifying

subsequent events.

True False

17.Subsequent events may provide additional information about a condition that

existed at the date of the financial statements.

True False

18.Subsequently discovered facts are matters identified by auditors after the date of

the financial statements but prior to the date of the auditors' report.

True False

19.If a necessary audit procedure has been omitted, auditors should first identify

whether individuals are currently relying on the client's financial statements and

auditors' reports.

True False

20.Auditors' communications with the individuals charged with governance of the

client can be provided either during the audit or at the conclusion of the audit.

True False

Multiple Choice Questions

21. Which of the following events or activities

may occur following the audit report

release date?

A

.

Interim testing.

B. Roll-forward work.

C. Subsequent events.

D. Subsequently discovered facts.

22. Interim testing normally occurs between

what two dates?

A. Beginning of the year uaudit and audit report redate.

B. Date of the financial statements and audit report releaC. Beginning of the year under audit and date of the finaD. End of the year under audit and date of the auditors' r23. Roll-forward work normally occurs

between what two dates?

A. Beginning of the year uaudit and audit report redate.

B. Date of the financial statements and audit report releaC. Beginning of the year under audit and date of the finaD. Date of the financial statements and date of the audito24. For which of the following objectives would

auditors be least likely to use analytical

procedures in the completion stages of the

audit?

A. Obtaining eviderelated to accoutransactions.

B. Evaluating the adequacy of evidence gathered in respaccount balances.

C. Identifying unusual or unexpected account balances oaccount balances that were not identified during the aD. Evaluating the adequacy of evidence gathered in resprelationships among account balances.

25. Which of the following best describes the

auditors' responsibility with respect to

management's estimates?

A. Verifying the mathemataccuracy of managemeestimates.

B. Assessing the likelihood that actual results will be conmanagement's estimates.

C. Evaluating the reasonableness of management's estimD. Identifying how the entity's failure to achieve manageminfluence users' decisions.

26. Which of the following would not ordinarily

be considered when using analytical

procedures to verify the overall

reasonableness of revenue and expense

accounts?

A. Current-year recorded

(unaudited) balances.

B. Expected balances using a statistical analysis or relataccounts.

C. Internal budgets and reports.

D. Prior-year balances.

27. Why should auditors be particularly

concerned with "miscellaneous" "other,"

and "clearing" accounts classified as

revenues or expenses?

A. These accounts are likelyrelate to going-concern

matters.

B. These accounts are often more difficult to audit using procedures.

C. These accounts may represent attempts of earnings mD. These accounts are likely to require the assistance of 28. Which of the following is the most effective

method of identifying potential earnings

management attempts?

A. Analytical

procedures.

B. Detailed substantive procedures.

C. Inquiry of client management and key financial personD. Scanning accounts for unusual items.

29. An important method used by auditors to

learn of material contingencies is

A. Examining documpossession conceB. Inquiring and discussing them with management.

C. Obtaining responses to an attorney letter.

D. Confirming accounts receivable with the client's custo

30. Which of the following procedures is not

used in auditors' examination of litigation,

claims, and assessments?

A. Obtaining a deslitigation, claimsmanagement.

B. Examining documentary evidence regarding litigation,assessments.

C. Reading minutes of meetings of stockholders, directorcommittees.

D. Performing analytical procedures.

31. Which of the following is typically not

included in the inquiry letter sent to the

client's attorneys?

A. A disclaimer regardiof settlement of penB. A listing of pending or threatened litigation, claims, or C. An evaluation of the likelihood of an unfavorable outcoD. An estimate of the range of potential loss.

32. Which party should request a letter

regarding litigation, claims, and

assessments from the client's attorney?

A. Attor

ney.

B. Auditors.

C. Client.

D. Securities and Exchange Commission or other regula33. To whom should written representations

be addressed?

A. Audit

ors.

B. Board of directors.

[Show More]

.png)

.png)

.png)

.png)