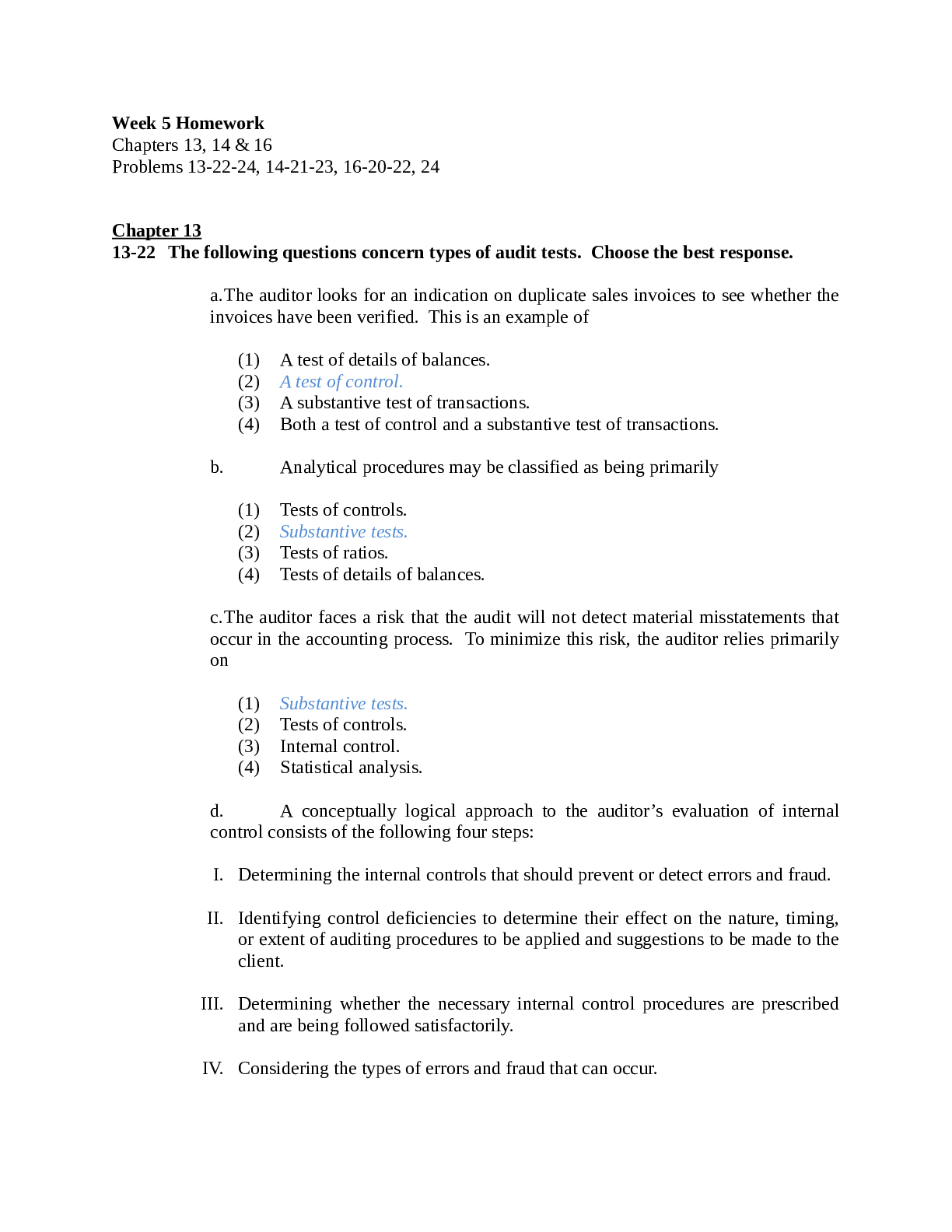

ACCT 555 HW week 7

Chapter 18: 21, 24, 28(e)

Chapter 19: 4, 12, 21, 22, 26

Chapter 21: 8, 10, 24, 27, 30

Chapter 24: 12, 13, 30, 28, 27

18-21 (Objective 18-3) Questions 1 through 8 are typically found in que

...

ACCT 555 HW week 7

Chapter 18: 21, 24, 28(e)

Chapter 19: 4, 12, 21, 22, 26

Chapter 21: 8, 10, 24, 27, 30

Chapter 24: 12, 13, 30, 28, 27

18-21 (Objective 18-3) Questions 1 through 8 are typically found in questionnaires used by auditors to obtain an understanding of internal control in the acquisition and payment cycle. In using the questionnaire for a client, a “yes” response to a question indicates a possible internal control, whereas a “no” indicates a potential deficiency.

1. Is the purchasing function performed by personnel who are independent of the receiving and shipping functions and the payables and disbursing functions?

2. Are all vendors’ invoices routed directly to accounting from the mailroom?

3. Are all receiving reports prenumbered and the numerical sequence checked by a person independent of check preparation?

4. Are all extensions, footings, discounts, and freight terms on vendors’ invoices checked for accuracy?

5. Does a responsible employee review and approve the invoice account distribution before the transaction is entered in the computer?

6. Are checks automatically posted in the cash disbursements journal as they are prepared?

7. Are all supporting documents properly cancelled at the time the checks are signed?

8. Is the custody of checks after signature and before mailing handled by an employee independent of all payable, disbursing, cash, and general ledger functions?

Required

a. For each of the preceding questions, state the transaction-related audit objective(s) being fulfilled if the control is in effect.

b. For each internal control, list a test of control to test its effectiveness.

c. For each of the preceding questions, identify the nature of the potential financial misstatement(s) if the control is not in effect.

d. For each of the potential misstatements in part c, list a substantive audit procedure that can be used to determine whether a material misstatement exists.

18-24 (Objectives 18-3, 18-6) The following misstatements are included in the accounting records of Westgate Manufacturing Company.

1. The accounts payable clerk prepares a monthly check to Story Supply Company for the amount of an invoice owed and submits the unsigned check to the treasurer for payment along with related supporting documents that have already been approved. When she receives the signed check from the treasurer, she records it as a debit to accounts payable and deposits the check in a personal bank account for a company named Story Company. A few days later, she records the invoice in the acquisitions journal again, resubmits the documents and a new check to the treasurer, and sends the check to the vendor after it has been signed.

2. The amount of a check in the cash disbursements journal is recorded as $4,612.87 instead of $6,412.87.

3. The accounts payable clerk intentionally excluded from the cash disbursements journal seven large checks written and mailed on December 26 to prevent cash in the bank from having a negative balance on the general ledger. They were recorded on January 2 of the subsequent year.

4. Each month, a fraudulent receiving report is submitted to accounting by an employee in the receiving department. A few days later, he sends Westgate an invoice for the quantity of goods ordered from a small company he owns and operates in the evening. A check is prepared, and the amount is paid when the receiving report and the vendor’s invoice are matched by the accounts payable clerk.

5. Telephone expense (account 2112) was unintentionally charged to repairs and maintenance (account 2121).

6. Acquisitions of raw materials are often not recorded until several weeks after the goods are received because receiving personnel fail to forward receiving reports to accounting. When pressure from a vendor’s credit department is put on Westgate’s accounting department, it searches for the receiving report, records the transactions in the acquisitions journal, and pays the bill.

Required

a. For each misstatement, identify the transaction-related audit objective that was not met.

b. For each misstatement, state a control that should have prevented it from occurring on a continuing basis.

c. For each misstatement, state a substantive audit procedure that could uncover it.

18-28 (Objective 18-6) You were in the final stages of your audit of the financial statements of Ozine Corporation for the year ended December 31, 2011, when you were consulted by the corporation’s president, who believes there is no point to your examining the year 2012 acquisitions journal and testing data in support of year 2012 entries. He stated that (a) bills pertaining to 2011 that were received too late to be included in the December acquisitions journal were recorded as of the year-end by the corporation by journal entry, (b) the internal auditor made tests after the year-end, and (c) he will furnish you with a letter certifying that there were no unrecorded liabilities.

e. What sources in addition to the year 2012 acquisitions journal should the CPA consider to locate possible unrecorded liabilities?

19-4 (Objective 19-2) List and briefly state the purpose of all audit procedures that might reasonably be applied by an auditor to determine that all property, plant, and equipment retirements have been recorded in the accounting system.

19-12 (Objective 19-4) Which documents will be used to verify accrued property taxes and the related expense accounts?

1. The asset lives used to depreciate equipment are less than reasonable, expected useful lives.

2. Capitalizable assets are routinely expensed as repairs and maintenance, perishable tools, or supplies expense.

3. Acquisitions of property are recorded at incorrect amounts.

4. A loan against existing equipment is not recorded in the accounting records. The cash receipts from the loan never reached the company because they were used for the down payment on a piece of equipment now being used as an operating asset. The equipment is also not recorded in the records.

5. Computer equipment that is abandoned or traded for replacement equipment is not removed from the accounting records.

6. Depreciation expense for manufacturing operations is charged to administrative expenses.

7. Tools necessary for the maintenance of equipment are stolen by company employees for their personal use.

19-22 (Objective 19-2) The following types of internal controls are commonly used by organizations for property, plant, and equipment:

1. A fixed asset master file is maintained with a separate record for each fixed asset.

2. Written policies exist and are known by accounting personnel to differentiate between capitalizable additions, freight, installation costs, replacements, and maintenance expenditures.

3. Depreciation charges for individual assets are calculated for each asset; recorded in a fixed asset master file that includes cost, depreciation, and accumulated depreciation for each asset; and verified periodically by an independent clerk.

4. Acquisitions of fixed assets in excess of $20,000 are approved by the board of directors.

5. When practical, equipment is labeled with metal tags and is inventoried on a systematic basis.

Required

a. State the purpose of each of the internal controls just listed. Your answer should be in the form of the type of misstatement that is likely to be reduced because of the control.

b. For each internal control, list one test of control the auditor can use to test for its existence.

c. List one substantive procedure for testing whether the control is actually preventing misstatements in property, plant, and equipment.

19-26 (Objective 19-4) As part of the audit of different audit areas, auditors should be alert for the possibility of unrecorded liabilities. For each of the following audit areas or accounts, describe a liability that can be uncovered and the audit procedures that can uncover it:

a. Minutes of the board of directors meetings

b. Land and buildings

c. Rent expense

d. Interest expense

e. Cash surrender value of life insurance

f. Cash in the bank

g. Officers’ travel and entertainment expenses

21-8 (Objectives 21-4, 21-5, 21-6) In the verification of the amount of the inventory, one of the auditor’s concerns is that slow-moving and obsolete items be identified. List the auditing procedures that can be used to determine whether slow-moving or obsolete items have been included in inventory.

21-10 (Objective 21-5) Explain why a proper cutoff of purchases and sales is heavily dependent on the physical inventory observation. What information should be obtained during the physical count to make sure that cutoff is accurate?

21-24 (Objectives 21-1, 21-5, 21-6) The following misstatements are included in the inventory and related records of Westbox Manufacturing Company:

1. An inventory item was priced at $12 each instead of at the correct cost of $12 per dozen.

2. In taking the physical inventory, the last shipments for the day were excluded from inventory and were not included as a sale until the subsequent year.

3. The clerk in charge of the perpetual inventory master file altered the quantity on an inventory tag to cover up the shortage of inventory caused by its theft during the year.

4. After the auditor left the premises, several inventory tags were lost and were not included in the final inventory summary.

5. When raw material acquisitions were recorded, the improper unit price was included in the perpetual inventory master file. Therefore, the inventory valuation was misstated because the physical inventory was priced by referring to the perpetual records.

6. During the physical count, several obsolete inventory items were included.

7. Because of a significant increase in volume during the current year and excellent control over manufacturing overhead costs, the manufacturing overhead rate applied to inventory was far greater than actual cost.

21-27 (Objective 21-5) You encountered the following situations during the December 31, 2011, physical inventory of Latner Shoe Distributor Company:

Required

a. Latner maintains a large portion of the shoe merchandise in 10 warehouses throughout the eastern United States. This ensures swift delivery service for its chain of stores. You are assigned alone to the Boston warehouse to observe the physical inventory process. During the inventory count, several express trucks pulled in for loading. Although infrequent, express shipments must be attended to immediately. As a result, the employees who were counting the inventory stopped to assist in loading the express trucks. What should you do?

b.

(1) In one storeroom of 10,000 items, you have test-counted about 200 items of high value and a few items of low value. You found no misstatements. You also note that the employees are diligently following the inventory instructions. Do you think you have tested enough items? Explain.

(2) What would you do if you test-counted 150 items and found a substantial number of counting errors?

c. In observing an inventory of liquid shoe polish, you note that one lot is 5 years old. From inspection of some bottles in an open box, you find that the liquid has solidified in most of the bottles. What action should you take?

d. During your observation of the inventory count in the main warehouse, you found that most of the prenumbered tags that had been incorrectly filled out are being destroyed and thrown away. What is the significance of this procedure and what action should you take?

21-30 (Objective 21-5) In an annual audit at December 31, 2011, you find the following transactions near the closing date:

1. Merchandise costing $1,822 was received on January 3, 2012, and the related acquisition invoice recorded January 5. The invoice showed the shipment was made on December 29, 2011, FOB destination.

2. Merchandise costing $625 was received on December 28, 2011, and the invoice was not recorded. You located it in the hands of the purchasing agent; it was marked “on consignment.”

3. A packing case containing products costing $816 was standing in the shipping room when the physical inventory was taken. It was not included in the inventory because it was marked “Hold for shipping instructions.” Your investigation revealed that the customer’s order was dated December 18, 2011, but that the case was shipped and the customer billed on January 10, 2012. The product was a stock item of your client.

4. Merchandise received on January 6, 2012, costing $720 was entered in the acquisitions journal on January 7, 2012. The invoice showed shipment was made FOB supplier’s warehouse on December 31, 2011. Because it was not on hand December 31, it was not included in inventory.

5. A special machine, fabricated to order for a customer, was finished and in the shipping room on December 31, 2011. The customer was billed on that date and the machine excluded from inventory, although it was shipped on January 4, 2012.

24-12 (Objective 24-4) What major considerations should the auditor take into account in determining how extensive the review of subsequent events should be?

The major considerations would be if it has a direct effect on the financial statements and requires adjustment. Or if it has no direct effect on the financial statements but for which disclosure is advisable.

24-13 (Objective 24-4) Identify five audit procedures normally done as a part of the review for subsequent events.

24-30 (Objectives 24-4, 24-8) The field work for the June 30, 2011, audit of Tracy Brewing Company was finished August 19, 2011, and the completed financial statements, accompanied by the signed audit reports, were mailed September 6, 2011. In each of the highly material independent events (a through i), state the appropriate action (1 through 4) for the situation and justify your response. The alternative actions are as follows:

1. Adjust the June 30, 2011, financial statements.

2. Disclose the information in a footnote in the June 30, 2011, financial statements.

3. Request the client to recall the June 30, 2011, statements for revision.

4. No action is required.

*AICPA adapted.

The events are as follows:

a. On December 14, 2011, the auditor discovered that a debtor of Tracy Brewing went bankrupt on July 15, 2011, due to declining financial health. The sale had taken place January 15, 2011.

3.

b. On December 14, 2011, the auditor discovered that a debtor of Tracy Brewing went bankrupt on October 2, 2011. The sale had taken place April 15, 2011, but the amount appeared collectible at June 30, 2011, and August 19, 2011.

4

c. On August 15, 2011, the auditor discovered that a debtor of Tracy Brewing went bankrupt on August 1, 2011. The most recent sale had taken place April 2, 2010, and no cash receipts had been received since that date.

1.

d. On August 6, 2011, the auditor discovered that a debtor of Tracy Brewing went bankrupt on July 30, 2011. The cause of the bankruptcy was an unexpected loss of a major lawsuit on July 15, 2011, resulting from a product deficiency suit by a different customer.

2.

e. On August 6, 2011, the auditor discovered that a debtor of Tracy Brewing went bankrupt on July 30, 2011, for a sale that took place July 3, 2011. The cause of the bankruptcy was a major uninsured fire on July 20, 2011.

4.

f. On July 20, 2011, Tracy Brewing settled a lawsuit out of court that had originated in 2008 and is currently listed as a contingent liability.

1.

g. On September 14, 2011, Tracy Brewing lost a court case that had originated in 2010 for an amount equal to the lawsuit. The June 30, 2011, footnotes state that in the opinion of legal counsel there will be a favorable settlement.

4

h. On July 20, 2011, a lawsuit was filed against Tracy Brewing for a patent infringement action that allegedly took place in early 2011. In the opinion of legal counsel, there is a danger of a significant loss to the client.

i. On May 31, 2011, the auditor discovered an uninsured lawsuit against Tracy Brewing that had originated on February 28, 2011.

24-28 (Objective 24-3) In analyzing legal expense for the Boastman Bottle Company, Mary Little, CPA, observes that the company has paid legal fees to three different law firms during the current year. In accordance with her CPA firm’s normal operating practice, Little requests standard attorney letters as of the balance sheet date from each of the three law firms.

On the last day of field work, Little notes that one of the attorney letters has not yet been received. The second letter contains a statement to the effect that the law firm deals exclusively in registering patents and refuses to comment on any lawsuits or other legal affairs of the client. The third attorney’s letter states that there is an outstanding unpaid bill due from the client and recognizes the existence of a potentially material lawsuit against the client but refuses to comment further to protect the legal rights of the client.

a. Evaluate Little’s approach to sending the attorney letters and her follow-up on the responses.

b. What should Little do about each of the letters?

24-27 (Objective 24-2) In an audit of the Marco Corporation as of December 31, 2011, the following situations exist. No entries have been made in the accounting records in relation to these items.

1. During the year 2011, the Marco Corporation was named as a defendant in a suit for damages by the Dalton Company for breach of contract. An adverse decision to the Marco Corporation was rendered and the Dalton Company was awarded $4,000,000 damages. At the time of the audit, the case was under appeal to a higher court.

2. On December 23, 2011, the Marco Corporation declared a common stock dividend of 1,000 shares with a par value of $1,000,000 of its common stock, payable February 2, 2012, to the common stockholders of record December 30, 2011.

3. The Marco Corporation has guaranteed the payment of interest on the 10-year, first mortgage bonds of the Newart Company, an affiliate. Outstanding bonds of the Newart Company amount to $5,500,000 with interest payable at 5% per annum, due June 1 and December 1 of each year. The bonds were issued by the Newart Company on December 1, 2009, and all interest payments have been met by that company with the exception of the payment due December 1, 2011. The Marco Corporation states that it will pay the defaulted interest to the bondholders on January 15, 2012.

Required

a. Define contingent liability.

b. Describe the audit procedures you would use to learn about each of the situations listed.

[Show More]