Auditing > QUESTIONS & ANSWERS > AUDIT THEORY Post-Quiz #9: Audit Sampling | Download for quality grades | (All)

AUDIT THEORY Post-Quiz #9: Audit Sampling | Download for quality grades |

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 9 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Mar 08, 2023

Number of pages

9

Written in

All

Additional information

This document has been written for:

Uploaded

Mar 08, 2023

Downloads

0

Views

200

Document Keyword Tags

Recommended For You

Get more on QUESTIONS & ANSWERS »

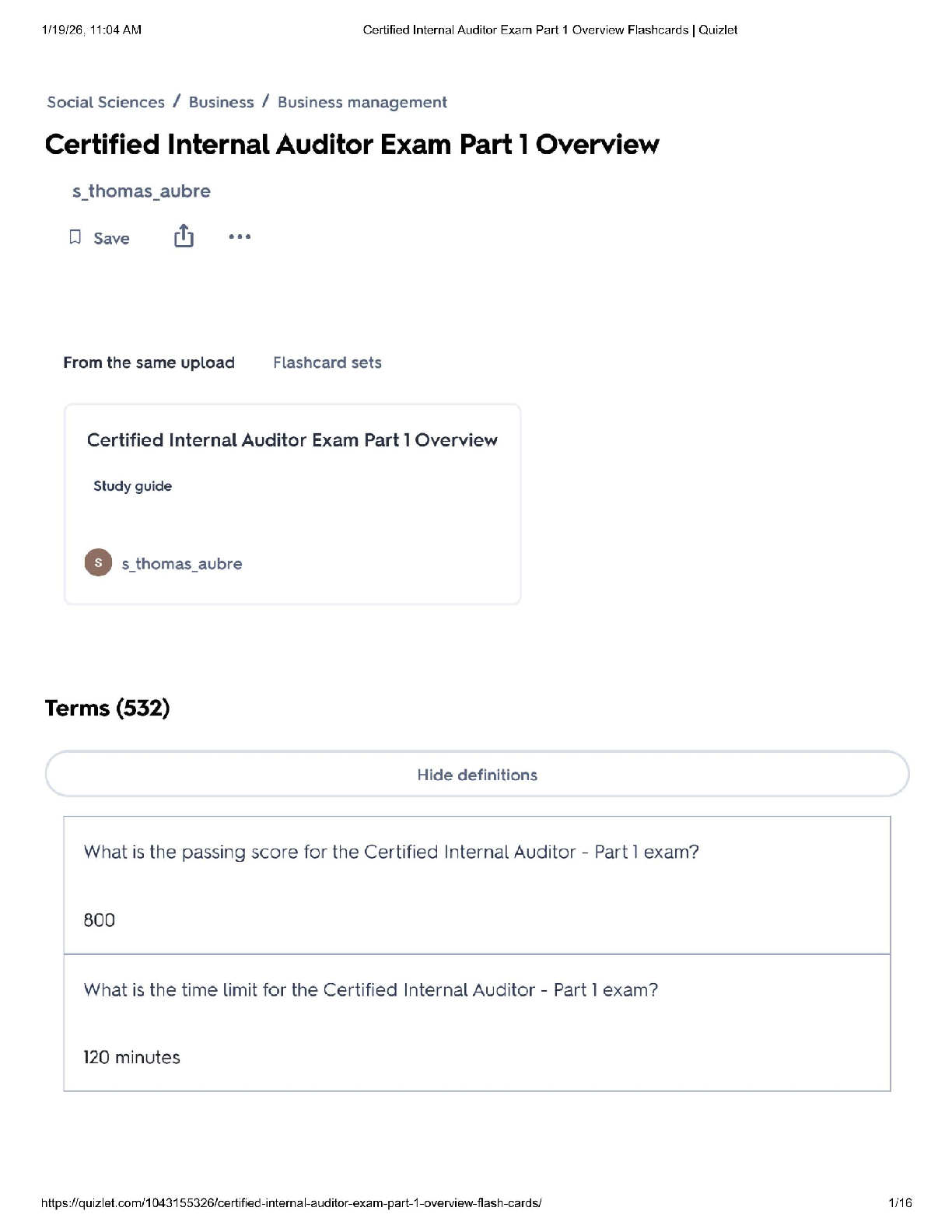

CIA Exam Part 1 Study Unit 2 / Score 100% / New 2025 Update /...

Certified Internal Auditor (CIA) Part 1 / Overview Flashcards...

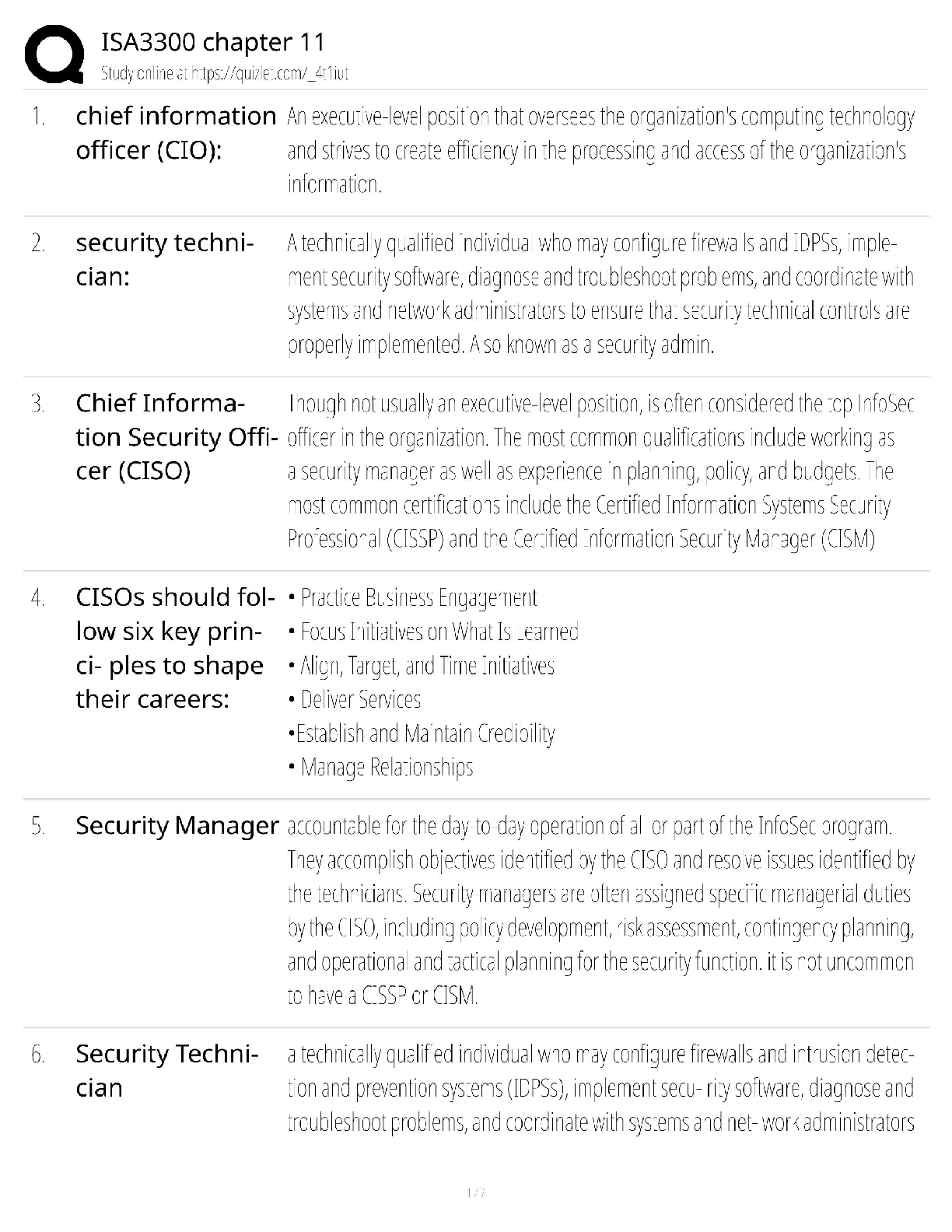

ISA 3300 Chapter 11 / Study Guide & Test Bank / Score 100% / 2...

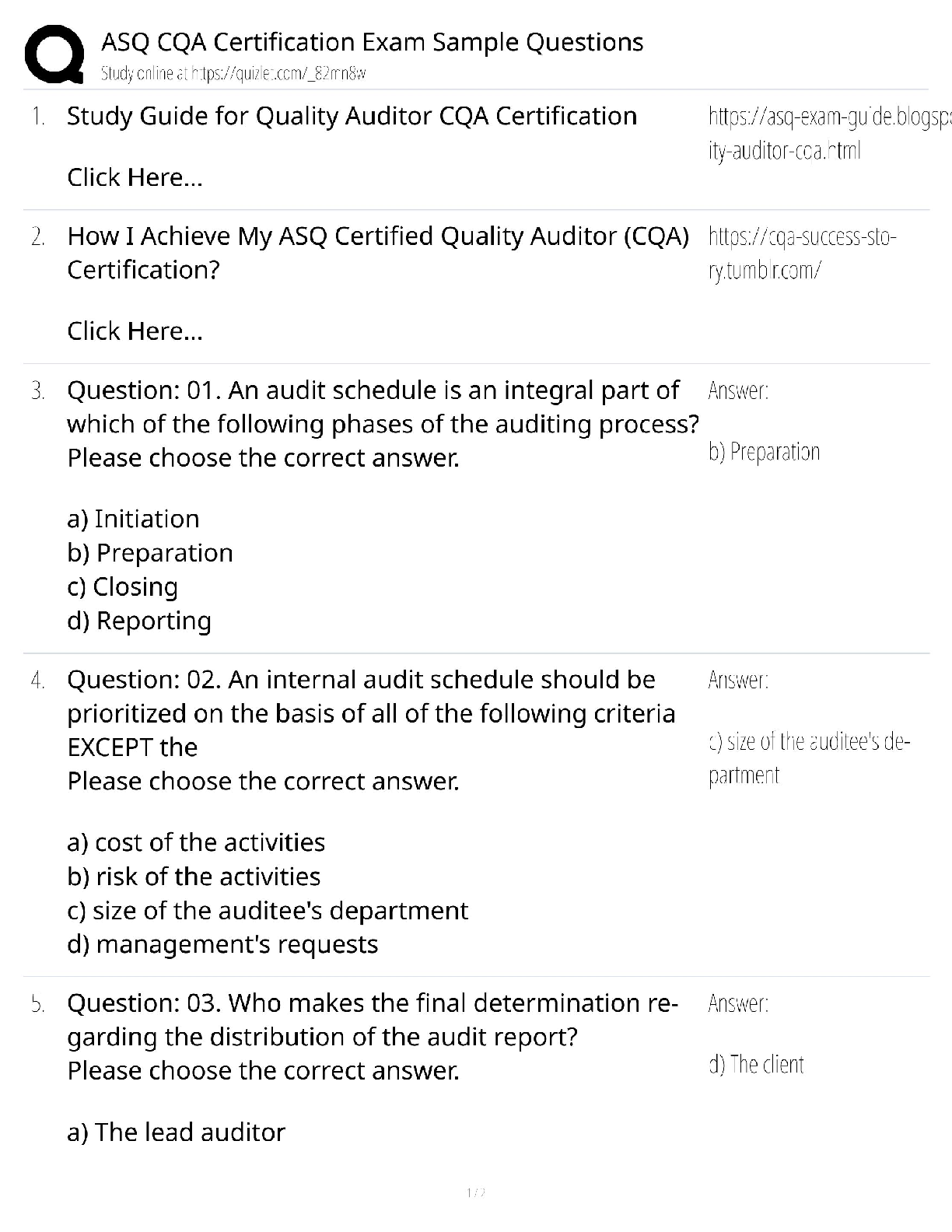

ASQ CQA Certification Exam / Score 100% / 2025 Official Practi...

Auditing A Risk-Based Approach to Conducting a Quality Audit,...

Solution Manual for Principles of Auditing & Other Assurance S...

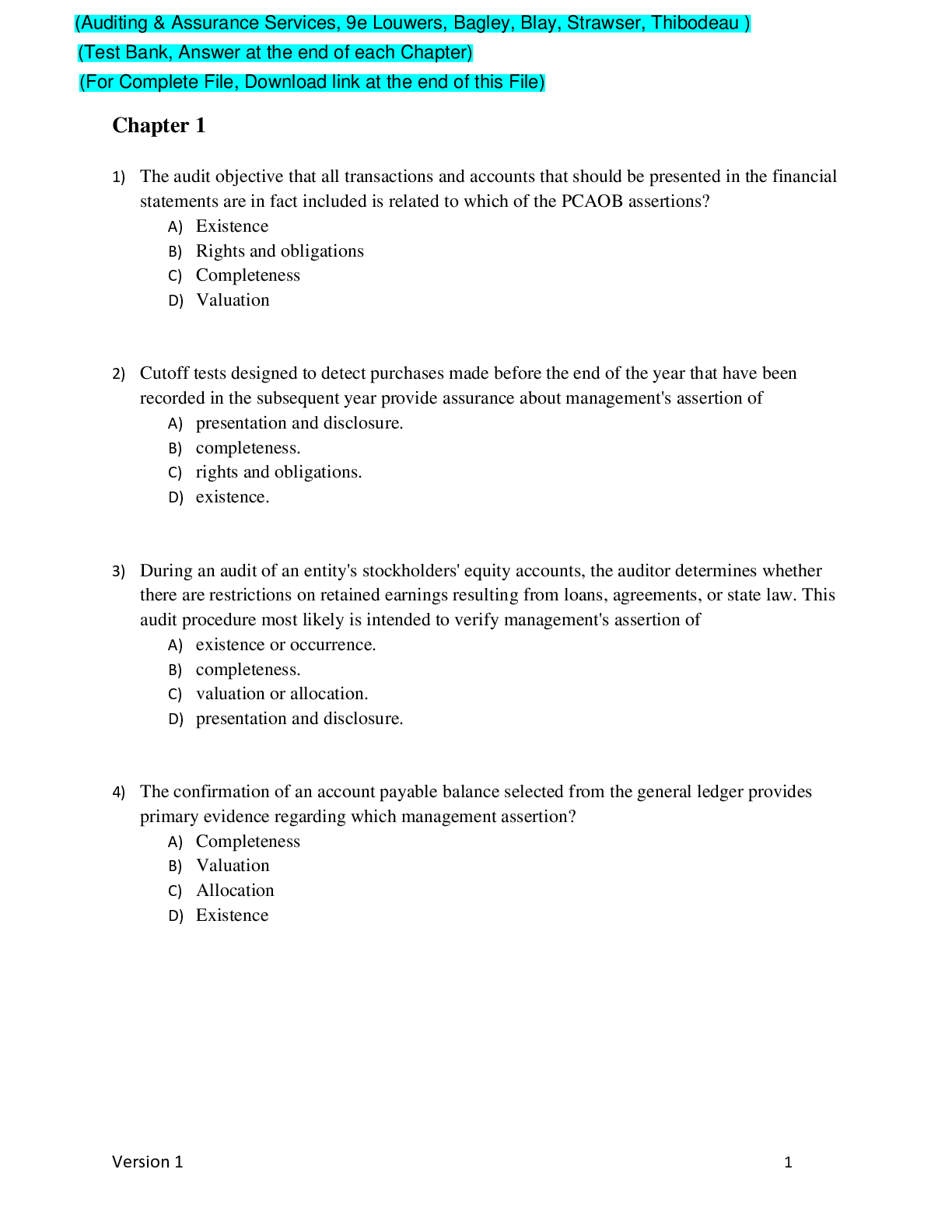

Auditing & Assurance Services, 9e Louwers, Bagley, Blay, Straw...

Auditing & Assurance Services, 9e Louwers, Bagley, Blay, Straw...

.png)

Cloud 9 Ltd II An Audit Case Study, 1st Canadian Edition, 1e...

SOLUTIONS MANUAL for Auditing & Assurance Services 9th Editio...

![Preview of eBook [PDF] Principles of Auditing Other Assurance Services (EverGreen Release) (2024 Rele](https://scholarfriends.com/img/resources-img.jpg)

![Preview of eBook ISE [PDF] Principles of Auditing Other Assurance Services 2024 Release By O. Ray Whi](https://browseimages.nyc3.digitaloceanspaces.com/paper-images/2026/03/11/X9sk1UMk2026-03-11-12-0469b087581b389.png)

![Preview of eBook ISE [PDF] AUDITING and ASSURANCE SERVICES 9th Edition By Timothy J. Louwers, Penelop](https://browseimages.nyc3.digitaloceanspaces.com/paper-images/2026/03/10/igRpsVBO2026-03-10-11-4269b0822e8d69d.png)

![Preview of Problem 06: Getting a Date in the American Southwest (Using Dendrochronology): [18FA]](https://browseimages.nyc3.digitaloceanspaces.com/paper-images/2023/Apr/03/xdPF5U4X2023-04-03-11-40642a90e71aae8.png)