Auditing > Research Paper > Audit Procedures: Audit Procedures (All)

Audit Procedures: Audit Procedures

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 18 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Apr 29, 2023

Number of pages

18

Written in

All

Additional information

This document has been written for:

Uploaded

Apr 29, 2023

Downloads

0

Views

188

Document Keyword Tags

Recommended For You

Get more on Research Paper »

Contemporary Auditing 12th Edition By Michael Knapp (Solution...

.png)

Cloud 9 Ltd II An Audit Case Study, 1st Canadian Edition, 1e...

Auditing & Assurance Services, 9e Louwers, Bagley, Blay, Straw...

Auditing A Practical Approach, 4th Canadian Edition by Moroney...

Auditing & Assurance Services 8th Edition Timothy Louwers | Te...

Test Bank Auditing & Assurance Services, 9th Edition by Timoth...

TEST BANK for Auditing and Assurance Services, 18th edition by...

SOLUTIONS MANUAL for Auditing: The Art and Science of Assuranc...

SOLUTIONS MANUAL for Auditing & Assurance Services 9th Editio...

Test Bank for Principles of Auditing and Other Assurance Servi...

Solution Manual for Principles of Auditing & Other Assurance S...

AUDIT AND ASSURANCE- Electronic Question Bank From Exam 1 to E...

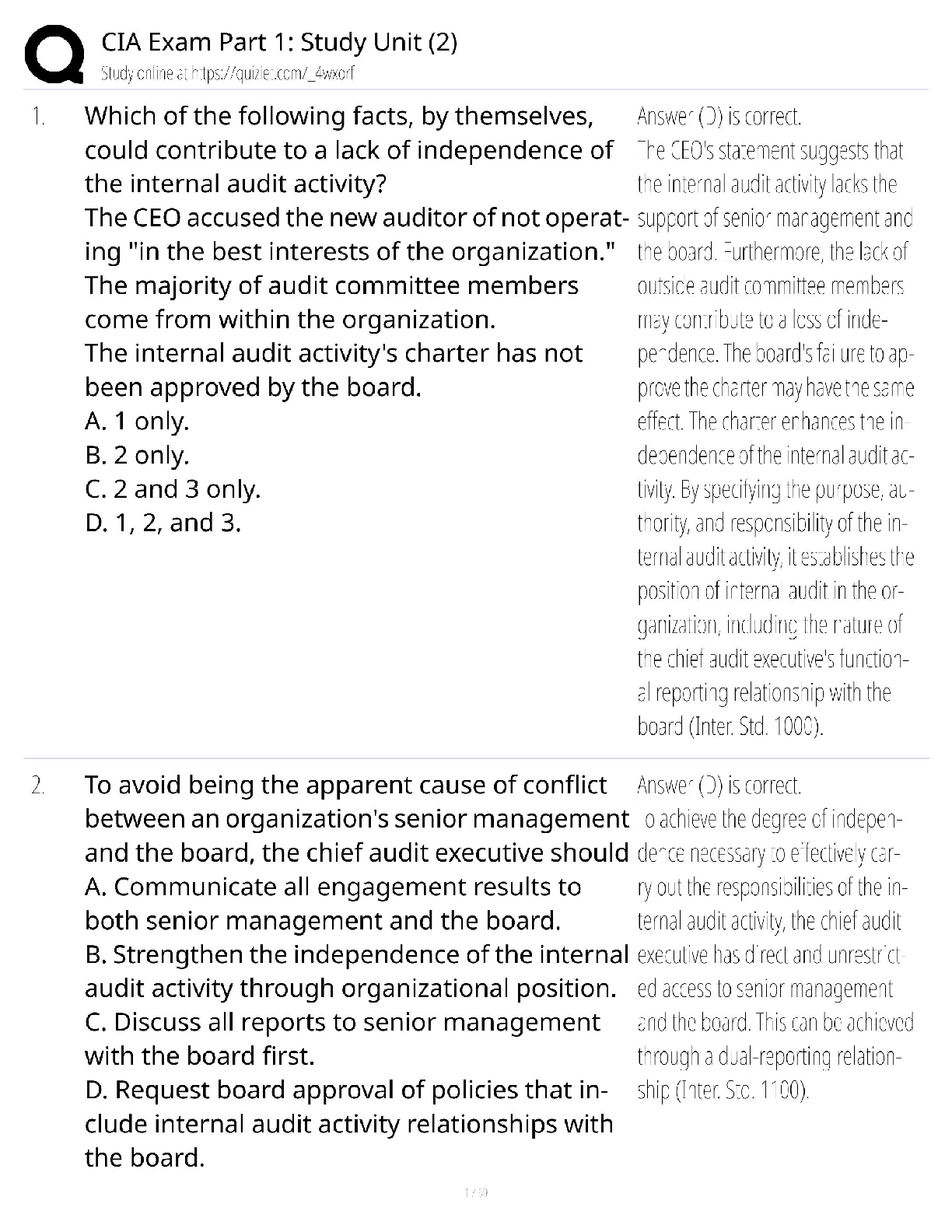

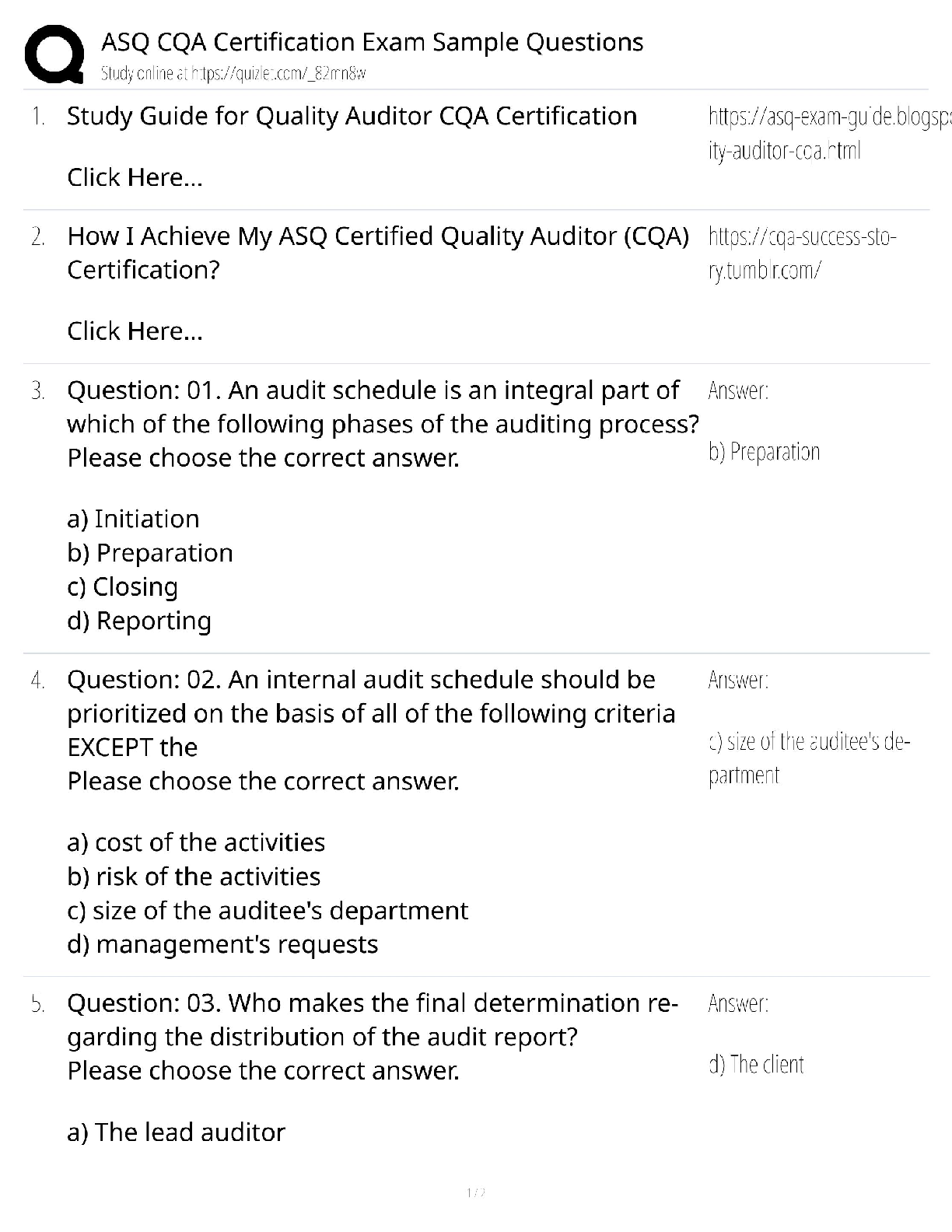

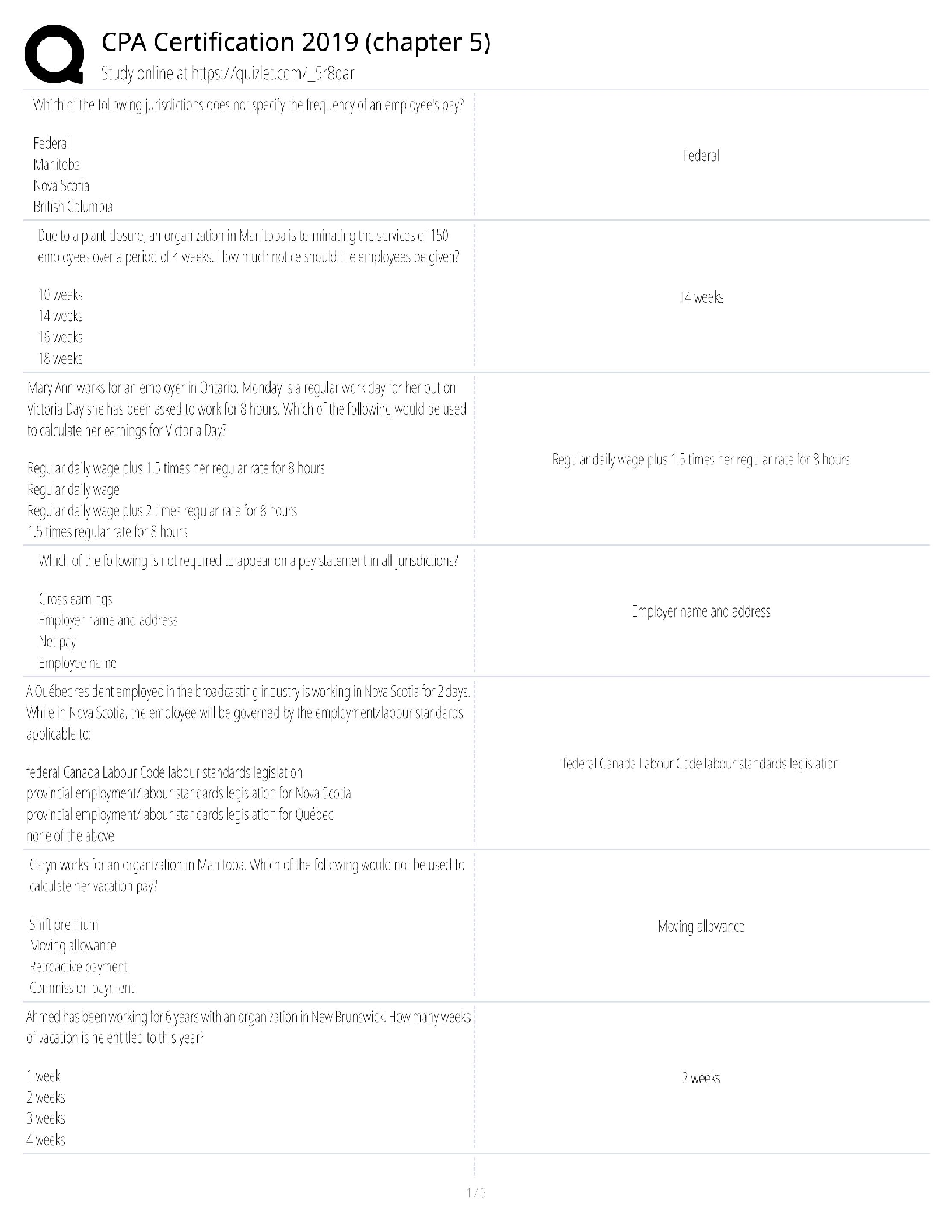

CIA Exam Part 1 Study Unit 2 / Score 100% / New 2025 Update /...

dfdfefe.png)