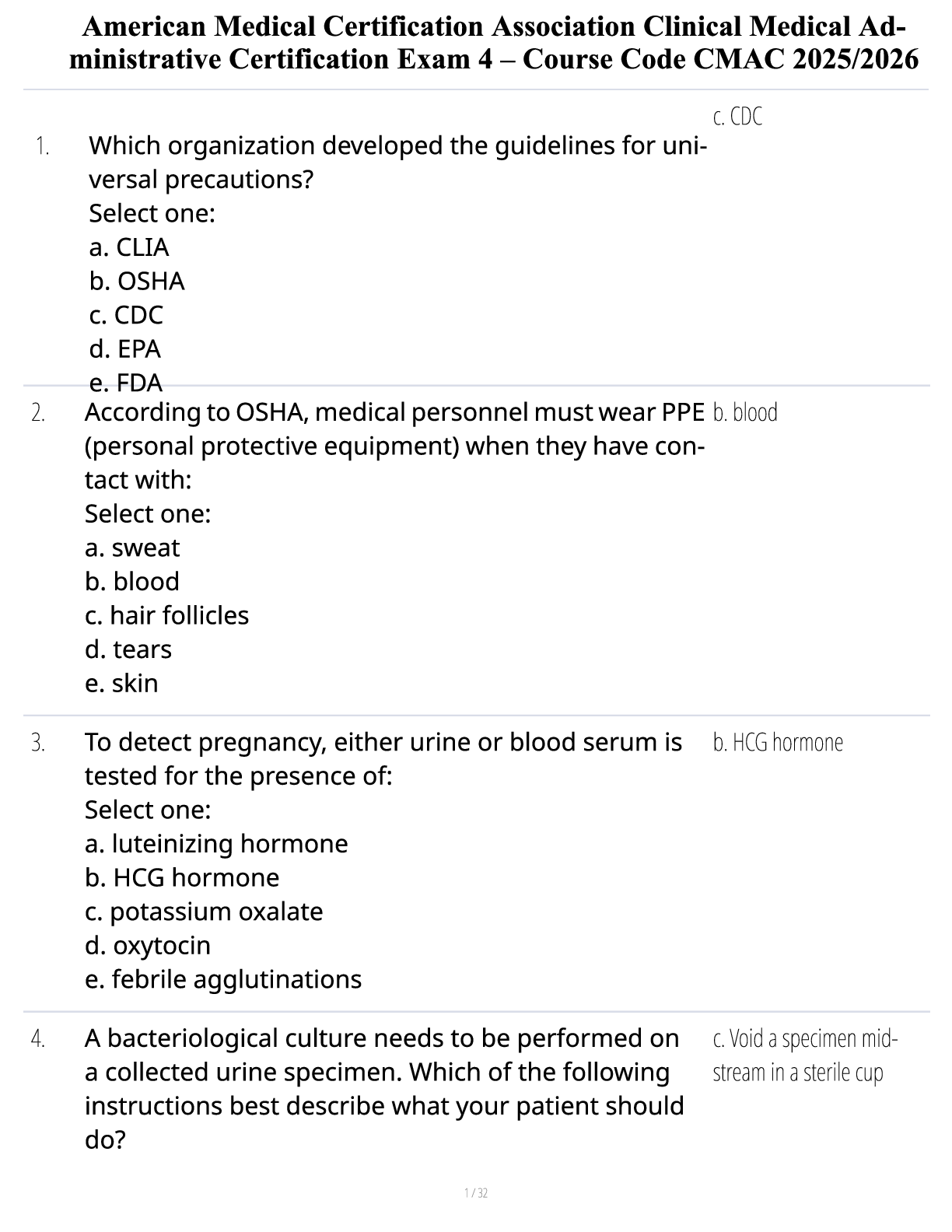

AC202 Quiz - Multiple_Choice_Answers 1. The total amount of cash and other assets received by a corporation from its stockholders in exchange for common stock is: A) Always equal to its par value. B) Always equal to its

...

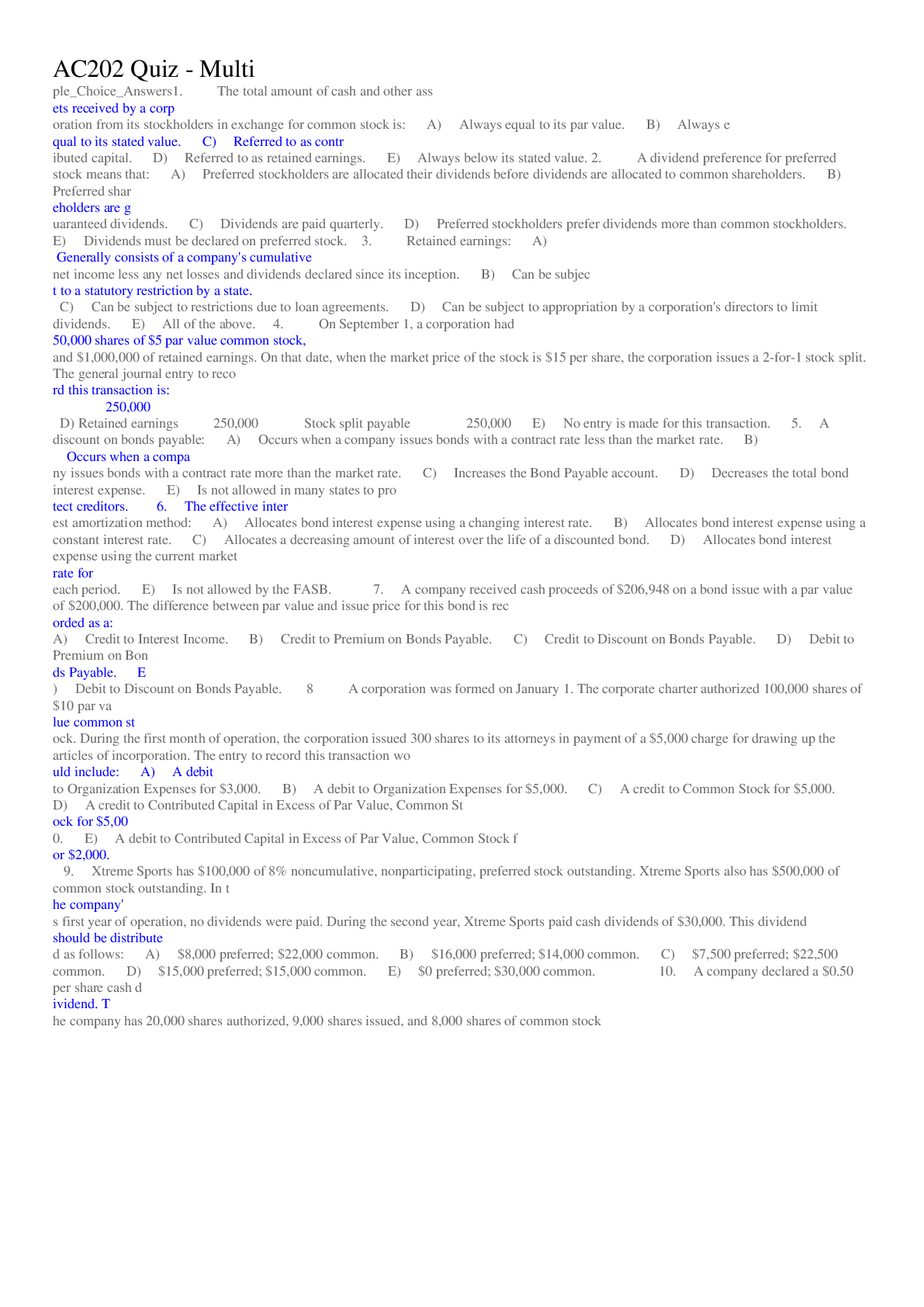

AC202 Quiz - Multiple_Choice_Answers 1. The total amount of cash and other assets received by a corporation from its stockholders in exchange for common stock is: A) Always equal to its par value. B) Always equal to its stated value. C) Referred to as contributed capital. D) Referred to as retained earnings. E) Always below its stated value. 2. A dividend preference for preferred stock means that: A) Preferred stockholders are allocated their dividends before dividends are allocated to common shareholders. B) Preferred shareholders are guaranteed dividends. C) Dividends are paid quarterly. D) Preferred stockholders prefer dividends more than common stockholders. E) Dividends must be declared on preferred stock. 3. Retained earnings: A) Generally consists of a company's cumulative net income less any net losses and dividends declared since its inception. B) Can be subject to a statutory restriction by a state. C) Can be subject to restrictions due to loan agreements. D) Can be subject to appropriation by a corporation's directors to limit dividends. E) All of the above. 4. On September 1, a corporation had 50,000 shares of $5 par value common stock, and $1,000,000 of retained earnings. On that date, when the market price of the stock is $15 per share, the corporation issues a 2-for-1 stock split. The general journal entry to record this transaction is: A) Retained earnings 750,000 Common Stock Split Distributable 750,000 B) Retained earnings 750,000 Common Stock 750,000 C) Retained Earnings 250,000 Common Stock 250,000 D) Retained earnings 250,000 Stock split payable 250,000 E) No entry is made for this transaction. 5. A discount on bonds payable: A) Occurs when a company issues bonds with a contract rate less than the market rate. B) Occurs when a company issues bonds with a contract rate more than the market rate. C) Increases the Bond Payable account. D) Decreases the total bond interest expense. E) Is not allowed in many states to protect creditors. 6. The effective interest amortization method: A) Allocates bond interest expense using a changing interest rate. B) Allocates bond interest expense using a constant interest rate. C) Allocates a decreasing amount of interest over the life of a discounted bond. D) Allocates bond interest expense using the current market rate for each period. E) Is not allowed by the FASB. 7. A company received cash proceeds of $206,948 on a bond issue with a par value of $200,000. The difference between par value and issue price for this bond is recorded as a: A) Credit to Interest Income. B) Credit to Premium on Bonds Payable. C) Credit to Discount on Bonds Payable. D) Debit to Premium on Bonds Payable. E) Debit to Discount on Bonds Payable. 8 A corporation was formed on January 1. The corporate charter authorized 100,000 shares of $10 par value common stock. During the first month of operation, the corporation issued 300 shares to its attorneys in payment of a $5,000 charge for drawing up the articles of incorporation. The entry to record this transaction would include: A) A debit to Organization Expenses for $3,000. B) A debit to Organization Expenses for $5,000. C) A credit to Common Stock for $5,000. D) A credit to Contributed Capital in Excess of Par Value, Common Stock for $5,000. E) A debit to Contributed Capital in Excess of Par Value, Common Stock for $2,000. 9. Xtreme Sports has $100,000 of 8% noncumulative, nonparticipating, preferred stock outstanding. Xtreme Sports also has $500,000 of common stock outstanding. In the company's first year of operation, no dividends were paid. During the second year, Xtreme Sports paid cash dividends of $30,000. This dividend should be distributed as follows: A) $8,000 preferred; $22,000 common. B) $16,000 preferred; $14,000 common. C) $7,500 preferred; $22,500 common. D) $15,000 preferred; $15,000 common. E) $0 preferred; $30,000 common. 10. A company declared a $0.50 per share cash dividend. The company has 20,000 shares authorized, 9,000 shares issued, and 8,000 shares of common stock outstanding. The journal entry to record the dividend declaration is: A) Retained Earnings 4,000 Common Dividends Payable 4,000 B) Common Dividends Payable 4,000 Cash 4,000 C) Retained Earnings 4,500 Common Dividends Payable 4,500 D) Common Dividends Payable 4,500 Cash 4,500 E) Retained Earnings 5,000 Common Dividends Payable 5,000 11. A company has bonds outstanding with a par value of $100,000. The unamortized premium on these bonds is $2,700. If the company retired these bonds at a call price of 99, the gain or loss on this retirement is: A) $ 1,000 gain. B) $ 1,000 loss. C) $ 2,700 loss. D) $ 2,700 gain. E) $ 3,700 gain. 12. On October 1, a $30,000, 6%, 3-year installment note payable is issued by a company. The note requires that $10,000 of principal plus accrued interest be paid at the end of each year on September 30. The issuer's journal entry to record the second annual interest payment would include: A) A debit to Interest Expense for $1,800. B) A debit to Interest Expense for $1,200. C) A credit to Cash for $11,800. D) A credit to Cash for $10,000. E) A debit to Notes Payable for $1,200. 13. Short-term investments in held-to-maturity debt securities are accounted for using the: A) Market value method with market adjustment to income. B) Market value method with market adjustment to equity. C) Cost method with amortization. D) Cost method without amortization. E) Equity method. 14. A decrease in the fair market value of a security that has not yet been realized through an actual sale of the security is called a(n): A) Contingent loss. B) Realizable loss. C) Unrealized loss. D) Capitalized loss. E) Market loss. 15. Six months ago, a company purchased an investment in stock for $65,000. This investment is considered available-for-sale. The current market value of the stock is $68,500. The company should record a: A) Debit to Unrealized Loss–Equity for $3,500. B) Credit to Unrealized Gain–Equity for $3,500. C) Debit to Investment Revenue for $3,500. D) Credit to Market Adjustment – Available-for-Sale for $3,500. E) Credit to Investment Revenue for $3,500. 16. Preparation of the statement of cash flows involves: A) Computing the net increase or decrease in cash. B) Computing and reporting net cash provided or used by operations. C) Computing and reporting net cash provided or used by investing activities. D) Computing and reporting net cash provided or used by financing activities. E) All of the above. 17. A statement of cash flows should reconcile the differences between the beginning and ending balances of: A) Net income. B) Equity. C) Cash and cash equivalents. D) Working capital. E) Cash, cash equivalents, and short-term investments. 18. Use the following information to calculate cash paid for wages and salaries: Salaries expense $168,000 Salaries payable, January 1 6,400 Salaries payable, December 31 10,600 A) $157,400. B) $163,800. C) $168,000. D) $172,200. E) $174,400. 19. When using the indirect method to calculate and report net cash provided or used by operating activities, which of the following is subtracted from net income? A) Decrease in income taxes payable. B) Depreciation expense. C) Amortization of intangible assets. D) Bad debts expense. E) Decrease in merchandise inventory. 20. Use the following information and the indirect method to calculate the net cash provided or used by operating activities: Net income $12,300 Depreciation expense 12,000 Payment on mortgage payable 15,000 Gain on sale of land 7,500 Increase in merchandise inventory 2,050 Increase in accounts payable 6,150 Proceeds from sale of land 8,000 A) $12,700. B) $13,900. C) $20,900. D) $28,400. E) $35,900. 21. . The ability to generate future revenues and meet long-term obligations is referred to as: A) Liquidity and efficiency. B) Solvency. C) Profitability. D) Market prospects. E) Creditworthiness. 22. The comparison of a company's financial condition and performance to a base amount is known as: A) Financial reporting. B) Horizontal ratios. C) Investment analysis. D) Risk analysis. E) Vertical analysis. 23. The common-size percent is computed by: A) Dividing the analysis amount by the base amount. B) Dividing the base amount by the analysis amount. C) Dividing the analysis amount by the base amount and multiplying the result by 100. D) Dividing the base amount by the analysis amount and multiplying the result by 1,000. E) Subtracting the base amount from the analysis amount and multiplying the result by 100. 24. One of several ratios that reflects solvency includes the: A) Acid-test ratio. B) Current ratio. C) Times interest earned ratio. D) Total asset turnover. E) Days' sales in inventory. 25. A company had a market price of $37.50 per share, earnings per share of $1.25, and dividends per share of $0.40. Its price-earnings ratio equals: A) 3.1. B) 30.0. C) 93.8. D) 32.0. E) 3.3.

[Show More]