Financial Accounting > A-Level Question Paper > Solutions Manual for Accounting Principles, (All)

Solutions Manual for Accounting Principles,

Document Content and Description Below

Last updated: 2 years ago

Preview 1 out of 10 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Oct 31, 2023

Number of pages

10

Written in

All

Additional information

This document has been written for:

Uploaded

Oct 31, 2023

Downloads

0

Views

86

Document Keyword Tags

Recommended For You

Get more on A-Level Question Paper »

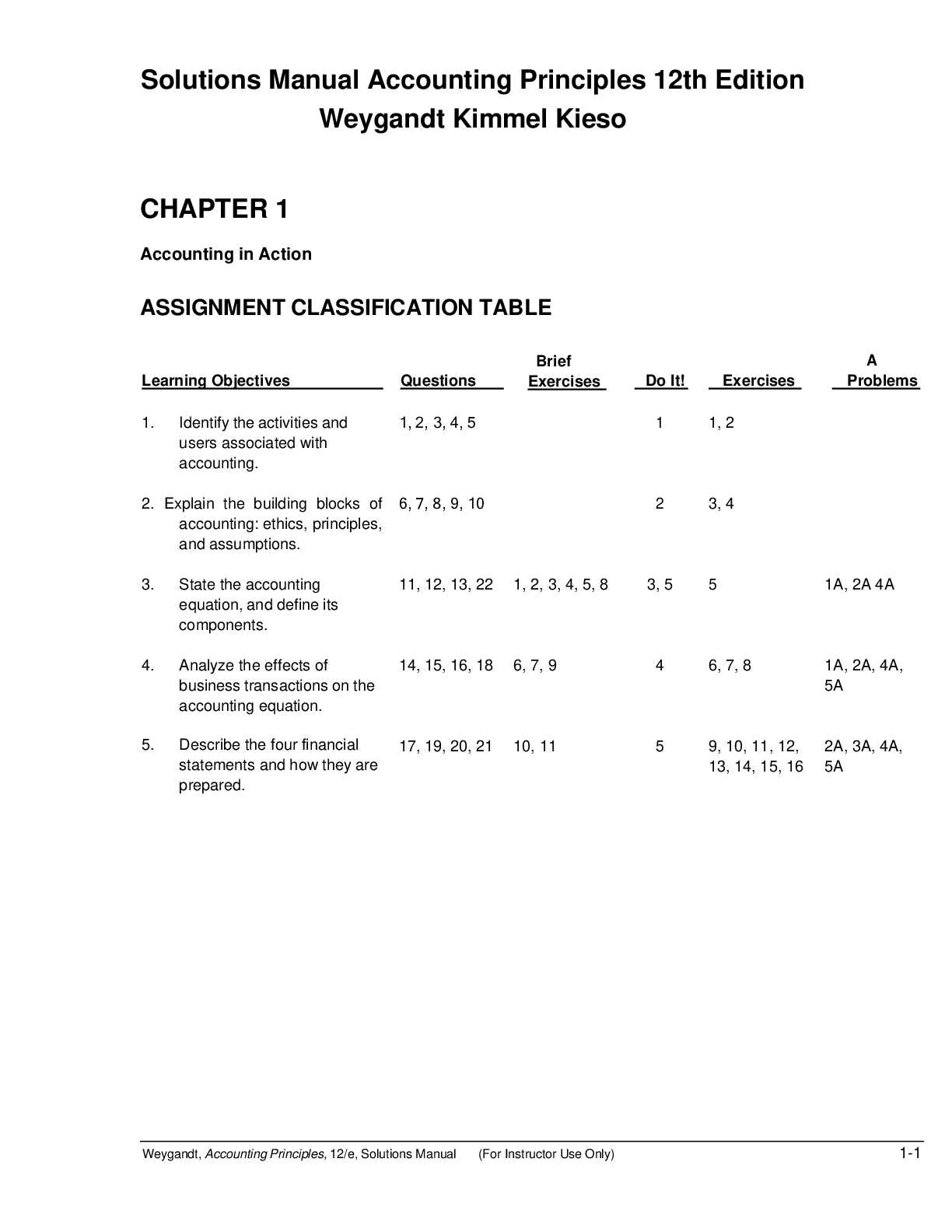

Solutions Manual Accounting Principles 12th Edition Weygandt K...

Test Bank for Advanced Accounting 4th Edition By Jeter Cheny

Test Bank For Advanced Financial Accounting 6th Edition By Ba...

Test Bank For Advanced Financial Accounting, Canadian 6th Edit...

Financial Accounting for Decision Makers 10th Edition By Peter...

Financial Accounting for Decision Makers 10th Edition, By Pete...

Advanced Accounting 5e Patrick Hopkins, Robert Halsey (Solutio...