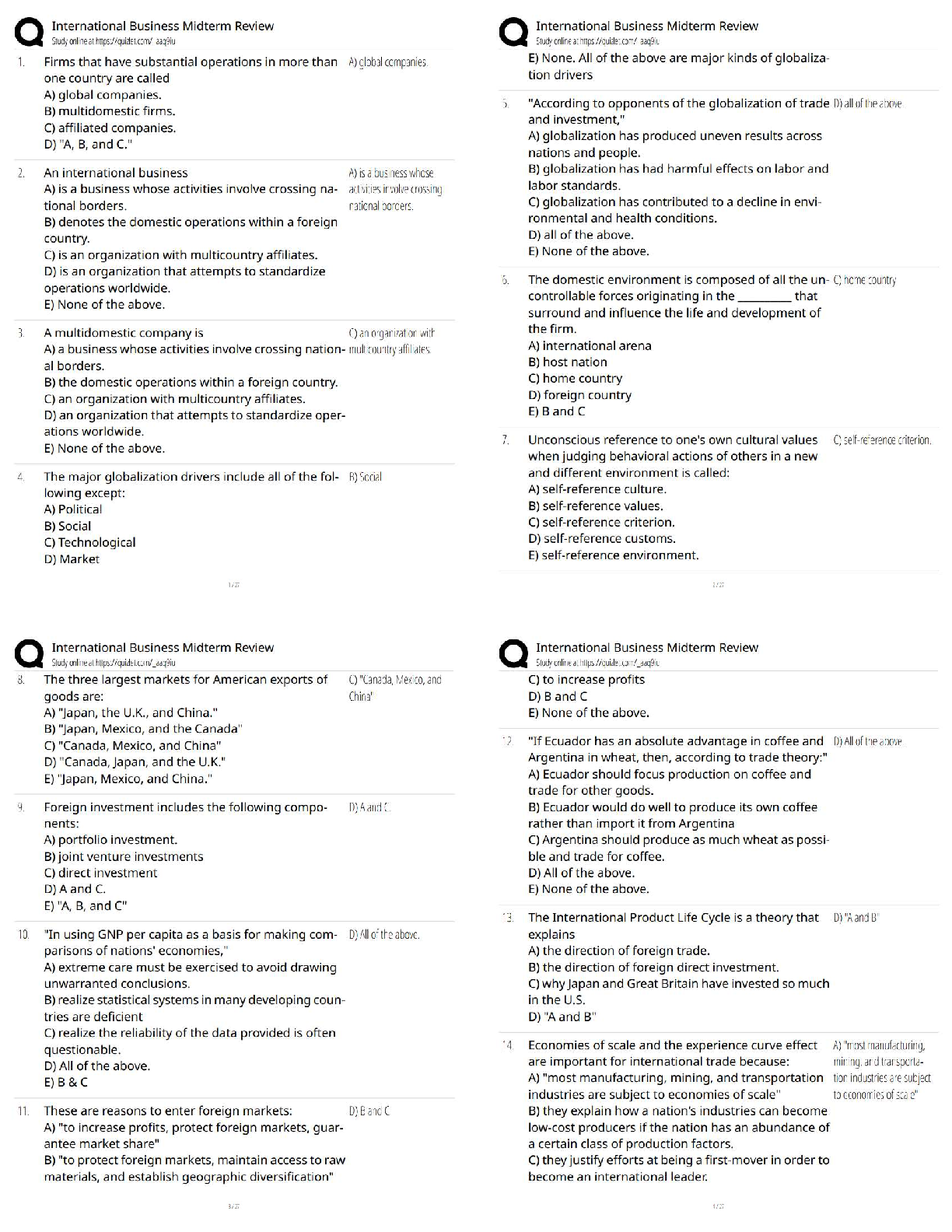

Strategic Management - MNGT - 405

Spring Term - R4B

Strategic Management - MNGT - 405 Spring Term - R4B

Sumit Karia Southern Alberta Institute of Technology

Table of Contents

The Merger of the

...

Strategic Management - MNGT - 405

Spring Term - R4B

Strategic Management - MNGT - 405 Spring Term - R4B

Sumit Karia Southern Alberta Institute of Technology

Table of Contents

The Merger of the TSX Group and the Montreal Exchange. 5

Tesla: Testing a Business Model at its (R)evolutionary Best. 19

Netflix Inc.: Streaming Across Borders and Into Original Content (A). 33

9B14N037

THE MERGER OF THE TSX GROUP AND THE MONTRÉAL EXCHANGE

THE MONTRÉAL EXCHANGE INC.

The Montréal Stock Exchange began operations in 1874. Bertrand became its president and CEO in March 2000, and one of his first actions was to demutualize the exchange in September 2000, creating the Montréal Exchange Inc. By year-end 2001

COMPETITIVE LANDSCAPE FOR EXCHANGES

The exchange industry had been consolidating rapidly over the past three years, with valuations driven up dramatically following a flurry of deals. Global consolidation was driven by the desire to achieve cost synergies by creating “super-exchanges.” Exchange mergers were motivated by the desire of institutional investors to trade across borders and time zones, pressure from regulators to cut retail trading costs, and the need to gain scale to finance information technology (IT) spending and overhead. Technology was a key value driver in the exchange industry, attracting trading volume, enabling new entrants and pushing down trading costs.

Exchange (CME) in a stock-swap transaction to form the CME Group (see Exhibits 7 and 8).

PREPARING FOR THE END OF THE 1999 SPECIALIZATION AGREEMENT

In March 1999, Canada’s securities exchanges had entered into a specialization agreement that was set to expire after 10 years.

• clearing of commodity contracts using the clearinghouse facilities of its U.S. partner.

Not everyone was in favour of a merger. The MX was the centre of the financial industry in Montréal, and its sale would be emblematic of more power shifting to Toronto, which raised hackles among Québec nationalists. The AMF wanted control of the MX to remain in Québec and the headquarters to remain in Montréal. Due to the 10 per cent ownership restriction, the AMF had the power to block any takeover of the MX. There was similar resistance from Toronto’s Bay Street community and the TSX board to giving in to the demands from Québec for greater influence over any merged entity.

MAKING A DECISION

Nesbitt’s years of experience told him that merging with the MX was the best strategic option for the TSX. He believed a merger was also in the best interests of the MX, as it would secure the exchange’s future in Montreal. The only question was how to make it happen. He began putting together a mental checklist of items to consider. Should he continue with negotiations with Bertrand and the MX board, even though talks had broken down? Or should he pursue a hostile bid? How much of a premium should the TSX offer for each MX share? Should they offer cash or stock? What other considerations were likely to be important for swaying the MX’s board and shareholders? And what would it take to convince the AMF not to block the deal?

EXHIBIT 1: MONTRÉAL EXCHANGE AND TSX GROUP SHARE PRICES

(March to October 2007)

Source: TSX-CMFRC database.

EXHIBIT 2: MONTRÉAL EXCHANGE BUSINESS SEGMENT

Source: Montreal Exchange, Prospectus dated March 23, 2007.

EXHIBIT 3: CONSOLIDATED INCOME STATEMENT FOR THE MONTRÉAL EXCHANGE INC.

(Thousands of dollars)

EXHIBIT 8: PRECEDENT TRANSACTIONS, 2004 TO 2007

Enterprise Price / EV / Premium (%)

Friendly Cur- Price / value (EV) Earnings EBITDA 1 1 1

Announce Target Acquirer / hostile Status rency share (millions) LTM* LTM* day week month

d

23-Jun-07 Borsa Italiana1 LSE Friendly Completed EUR 100.70 1,634 27.0 13.8 n.a. n.a. n.a.

14-Jun-07 CBOT CME Friendly Completed USD 208.38 11,065 55.5 28.0 54.9 59.4 72.5

25-May-07 OMX NASDAQ Friendly Completed SEK 208.1 25,100 27.1 17.5 19.0 22.3 25.0

30-Apr-07 ISE Eurex Friendly Completed USD 67.50 2,821 45.4 24.7 47.6 38.0 37.5

15-Mar-07 CBOT ICE Hostile Withdrawn USD 211.85 11,260 52.1 27.4 57.5 62.0 75.3

20-Nov-06 LSE NASDAQ Hostile Withdrawn GBP 12.43 2,401 26.9 16.8 2.1 (5.0) (2.5)

14-Sep-06 NYBOT ICE Friendly Completed USD n.a. 1,067 54.1 26.7 n.a. n.a. n.a.

1-Jun-06 Euronext NYSE Friendly Completed EUR 70.43 7,927 25.2 17.8 94.1 104.1 100.6

23-May-06 Euronext Deutsche Börse Hostile Withdrawn EUR 62.46 7,030 22.3 15.8 70.4 78.5 76.2

27-Mar-06 SFE ASE Friendly Completed AUD 16.63 2,251 32.5 24.4 17.8 17.9 28.9

9-Mar-06 LSE NASDAQ Hostile Withdrawn GBP 9.50 2,430 34.6 18.5 10.0 10.5 23.4

15-Dec-05 LSE Macquarie Bank Hostile Withdrawn GBP 5.80 1,476 21.1 10.8 5.1 7.4 16.0

13-Dec-04 LSE Deutsche Börse Hostile Withdrawn GBP 5.30 1,349 22.0 10.8 23.3 27.8 33.8

Average 34.3 19.5 36.5 38.4 44.2

Median 27.1 17.8 23.3 27.8 33.8

LTM = Last twelve months.

1. Not publicly listed.

Source: Thomson SDC.

9B18M033

TESLA: TESTING A BUSINESS MODEL AT ITS (R)EVOLUTIONARY BEST1

Tesla Motors, Inc. (Tesla), the electric car company, unveiled its Model 3 in late July 2017 as its stock price continued to appreciate. The Model 3 was priced to sell to the mass market and to potentially compete with the mass-market leaders such as Toyota. The stock market had also responded favourably to Tesla’s decision in 2016 to acquire SolarCity, a manufacturer of solar cells, and its decision to build the Gigafactory, the world’s largest lithium battery plant. Could Tesla justify its sky-high stock price multiple by simply selling electric cars, or was the market expecting Tesla to become a battery company that could fundamentally change the energy storage industry—or for that matter, some other type of company?

A BRIEF HISTORY OF TESLA MOTORS INC. (TESLA)

Tesla (NASDAQ: TSLA), was started on July 1, 2003, by two Silicon Valley-based entrepreneurs, Martin Eberhard and Marc Tarpenning, whose initial goal was to develop a fully electric sports car. Elon Musk was one of its most celebrated early investors and eventually became the chief executive officer (CEO) and driving force behind the new company.

THE OPPORTUNITY AND CHALLENGES DRIVING TESLA’S BUSINESS MODEL

Tesla’s disruptive business model had been seen before many times in other industries. Typically, a key resource—and usually the most expensive resource of the incumbent business model—was replaced by a new technology that over time became cost-competitive with the resources that were key to incumbents. This scenario had happened to the steam engine (disrupted by the gasoline engine), VHS videocassettes (disrupted by DVDs),

Distribution Channels

Tesla had been a vocal critic of the traditional dealer-based distribution model, claiming the model was outdated and costly for consumers. The latter claim was supported by a Goldman Sachs report that estimated a direct-to-consumer distribution model would save customers approximately $2,225 on a $26,000 car or approximately 8.6 per cent.15 The criticism was justified. According to the National Automobile Dealers Association, in 2012, the United States had 17,635 franchised dealerships. Total dealership revenue in 2012 reached $676 billion, up 9.8 per cent over 2011; however, total gross margins fell in 2012 due to increased costs and expenses in such areas as advertising, rent, and payroll.16 The dealer-based distribution system that allocated sales territories rested on the theory that a protected market compensated dealers for the risk of investing in buildings and large inventories. State laws generally prohibited anyone but a licensed franchisee from selling new cars.17

Tesla’s Gigafactory for Batteries

Tesla’s major sourcing challenge was the battery. Tesla was sourcing this critical component from the Far East, which left itself open to supply and quality problems. Moreover, it had no control over the cost—a factor that would become increasingly critical as the Model 3 rolled off the assembly line. Competition was also around the corner. For example, Volkswagen was developing a much longer-range vehicle battery that would pose serious competition to Tesla.

sustainable by using renewable energy from numerous metal windmills to generate electricity for the factory. Tesla also was reportedly looking at building another similar plant outside of North America.30

Acquisition of SolarCity

On November 21, 2016, Tesla acquired SolarCity for $2.6 billion.32 The deal made sense since the combined companies now produced three related products—solar power, power storage, and electric cars. Moreover, SolarCity had the largest market share (32 per cent) of the U.S. residential solar market. The former CEO of SolarCity commented that the deal would boost the development of renewable energy, and SolarCity might be able to lower its costs by virtue of

THE ROAD AHEAD FOR TESLA’S BUSINESS MODEL

From looking at its financials, it seemed that Tesla should have failed long ago. Since 2010, as it continued to pour its revenue back into the company, Tesla had recorded no positive EBIT (earnings before interest and taxes), no positive net income, and no positive free cash flow. In mid-2017, negative returns on assets, negative returns on equity, negative returns on invested capital, negative net margins, and negative earnings per share accompanied a debt/equity ratio of 1.4, a current ratio of 0.97, and a quick ratio of 0.53.36

According to Car and Driver, 27 different electric plug-ins or hybrids were either in design or available for purchase for the model year 2017–18.37 Some models, including some produced by Detroit’s Big Three, were already available and already priced below the lowest-priced Model 3.38 On July 5, 2017, Volvo announced that all of its 2019 models forward would be solely electric.39 Analysts nevertheless remained bullish on Tesla, given its integrated battery production. By one estimate, the battery for the Model 3 costs

$8,400 to produce, whereas the industry average price was $14,200 for a battery for a comparable vehicle.40

EXHIBIT 1: TESLA INC.’S CONSOLIDATED BALANCE SHEETS, 2015–2016 (IN US$ THOUSANDS)

Dec. 31,

2015 Dec. 31,

2016

1,196,908 3,393,216

22,628 105,519

168,965 499,142

1,277,838 2,067,454

115,667 194,465

2,782,006 6,259,796

1,791,403 3,134,080

– 5,919,880

3,403,334 5,982,957

12,816 376,145

– 506,302

31,522 268,165

46,858 216,751

8,067,939 22,664,076

916,148 1,860,341

422,798 1,210,028

423,961 763,126

136,831 179,504

283,370 663,859

627,927 984,211

– 165,936

2,811,035 5,827,005

2,021,093 5,860,049

– 99,164

– 10,287

446,105 851,790

1,293,741 2,210,423

364,976 1,891,449

6,936,950 16,750,167

– –

367,039

47,285 8,784

– –

131 161

3,409,452 7,773,727

(3,556) (23,740)

(2,322,323) (2,997,237)

1,083,704 4,752,911

– 785,175

8,067,939 22,664,076

– 5,919,880

– –

– 165,936

– 99,164

Source: United States Security and Exchange Commission, SEC Form 10-K, 56, filed by Tesla, Inc. on March 1, 2017 accessed August 13, 2017, www.sec.gov/Archives/edgar/data/1318605/000156459017003118/tsla-10k_20161231.htm# Consolidated_Balance_Sheets.

EXHIBIT 2: TESLA INC.’S CONSOLIDATED BALANCE SHEETS, DECEMBER 31, 2016, AND JUNE 30, 2017 (UNAUDITED) (IN US$ THOUSANDS)

Source: United States Security and Exchange Commission, SEC Form 10-Q, 4, filed by Tesla, Inc. on August 4, 2017, accessed August 13, 2017, www.sec.gov/Archives/edgar/data/1318605/000156459017015705/tsla-10q_20170630.htm.

EXHIBIT 4: TESLA INC.’S UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS, JUNE 2016 AND JUNE 2017 (IN US$ THOUSANDS)

6 Months Ended

Jun. 30, 2016 Jun. 30, 2017

Cash Flows From Operating Activities

Net loss (575,455) (798,608)

Adjustments to reconcile net loss to net cash used in operating activities:

Depreciation and amortization 339,692 765,773

Stock-based compensation 156,969 219,759

Amortization of debt discounts 41,696 64,151

Inventory write-downs 29,725 71,255

Loss on disposal of property and equipment 11,563 53,572

Foreign currency transaction loss (gain) (8,081) 29,394

Loss on the acquisition of SolarCity – 11,571

Non-cash interest and other operating activities 16,167 57,023

Changes operating assets and liabilities, net of effect of business combinations

Accounts receivable (1,426) 77,043

Inventories and operating lease vehicles (1,217,931) (1,121,155)

Prepaid expenses and other current assets 19,494 (113,192)

MyPower customer notes receivable and other assets (7,447) 26,339

Accounts payable and accrued liabilities 212,949 13,234

Deferred revenue 165,144 208,685

Customer deposits 398,555 (71,064)

Resale value guarantee 253,710 176,505

Other long-term liabilities 65,407 59,732

Net cash used in operating activities (99,269) (269,983)

Cash Flows from Investing Activities

Purchases of property and equipment excluding capital leases, net of sales (511,579) (1,511,692)

Maturities of short-term marketable securities 16,667 –

Purchase of solar energy systems, leased and to be leased – (418,792)

Increase in restricted cash (58,761) (102,528)

Business combination, net of cash acquired – (109,147)

Net cash used in investing activities (553,673) (2,142,159)

Cash Flows from Financing Activities

Proceeds from issuance of common stock in public offering 1,701,734 400,175

Proceeds from issuance of convertible and other debt 1,108,000 2,408,586

Repayments of convertible and other debt (578,683) (1,412,286)

Repayments of borrowings under solar bonds issued to related parties – (165,000)

Collateralized lease borrowings 384,525 335,675

Proceeds from exercise of stock options and other stock issuances 110,478 158,913

Principal payments on capital leases (18,270) (36,857)

Common stock and debt issuance costs (15,765) (13,688)

Purchase of convertible note hedges – (204,102)

Proceeds from settlement of convertible note hedges – 251,850

Proceeds from issuance of warrants – 52,883

Payments for settlement of warrants – (208,193)

Proceeds from investment by noncontrolling interests in subsidiaries – 583,433

Distributions paid to noncontrolling interests in subsidiaries – (123,873)

Net cash provided by financing activities 2,692,019 2,027,516

Effect of exchange rate changes on cash and cash equivalents 10,316 27,334

Net (decrease) increase in cash and cash equivalents 2,049,393 (357,292)

Cash and cash equivalents, beginning of period 1,196,908 3,393,216

Cash and cash equivalents, end of period 3,246,301 3,035,924

Supplemental noncash investing and financing activities

Acquisition of property and equipment included in liabilities 324,982 1,021,692

Estimated fair value of facilities under build-to-suit leases 172,770 173,075

Source: United States Security and Exchange Commission, SEC Form 10-Q, 7, filed by Tesla, Inc. on August 4, 2017, accessed August 13, 2017, www.sec.gov/Archives/edgar/data/1318605/000156459017015705/tsla-10q_20170630.htm

EXHIBIT 5: TESLA, INC.’S FREE CASH FLOWS, 2012–2016 (IN US$ MILLIONS)

FY (end of year data) 2012 2013 2014 2015 2016 TTM

Operating cash flow –266 258 –57 –524 –124 –295

Capital expenditure 239 264 970 1,635 1,440 2,859

Free cash flow –505 –6 –1,027 –2,159 –1,564 –3,154

Note: FY = financial year; TTM = trailing twelve months

Source: “Tesla Inc TSLA: Morningstar Rating,” Morningstar, accessed August 13, 2017, http://financials.morningstar.com/cash-flow/cf.html?t=TSLA®ion=usa&culture=en-US.

EXHIBIT 6: TESLA, INC.’S EBI, EBIT, AND NET INCOME, 2010–2016 (IN US$ MILLIONS)

FY (end of year data) 2010 2011 2012 2013 2014 2015 2016

EBIT –146.838 –251.488 –394.283 –61.283 –186.689 –716.629 –645.64

EBI –136.215 –234.569 –365.458 44.8 45.242 –294.039 301.459

Net Income –154.328 –254.411 –396.213 –74.014 –294.04 –888.663 –674.914

Note: EBI = earnings before interest; EBIT = earnings before interest and taxes; FY = financial year

Source: Created by authors using data from Wharton Research Data Services, “Complete Financial Statements (XLS),” accessed August 11, 2017, https://wrds.wharton.upenn.edu.

9B16M118

NETFLIX INC.: STREAMING ACROSS BORDERS AND INTO ORIGINAL CONTENT (A)1

Professor Luis Dau and David Wesley wrote this case solely to provide material for class discussion. The authors do not intend to illustrate either effective or ineffective handling of a managerial situation. The authors may have disguised certain names and other identifying information to protect confidentiality.

This publication may not be transmitted, photocopied, digitized or otherwise reproduced in any form or by any means without the permission of Ivey Publishing, the exclusive representative of the copyright holder. Reproduction of this material is not covered under authorization by any reproduction rights organization. To order copies or request permission to reproduce materials, contact Ivey Publishing, Ivey Business School, Western University, London, Ontario, Canada, N6G 0N1; (t) 519.661.3208; (e)

[email protected]; www.iveycases.com.

Copyright © 2016, Northeastern University, D’Amore-McKim School of Business Version: 2016-06-30

I was there when the new golden era of television went international, which is what Netflix did in this case by making the content more international.

— Steven Van Zandt, American actor and musician2

Netflix stock is wildly overvalued . . . in an increasingly commoditized business where brand will soon mean nothing—and international opportunities are not nearly what Netflix stock bulls believe them to be.

— Lawrence Meyers, chief executive officer of Asymmetrical Media Strategies3

Ted Sarandos, the chief content officer (CCO) at Netflix Inc. (Netflix), was the embodiment of a Silicon Valley executive, with cropped-back greying hair and an ever-present smile. Having spent his entire adult life working in video rentals and distribution, Sarandos was one of the world’s more knowledgeable people when it came to films, new and old. As CCO of Netflix, he was also arguably the world’s most influential person in video and film distribution.

In the days leading up to the 2015 U.S. Independence Day weekend, Sarandos found himself in Washington, D.C., addressing members of the Aspen Institute, a think tank focused on contemporary issues. As usual, Sarandos appeared relaxed in faded blue jeans, brown Chukka boots, and a blue dress shirt that he had left partially unbuttoned in an effort to counter the humid 90° F (30° C) heat that hung over Washington that summer day.

Only a few days earlier, billionaire investor Carl Icahn had sold his shares in Netflix for a $1.9 billion4 profit just as the company announced plans for a 7–1 stock split. “I believe the market is extremely overheated,” he exclaimed. “It is time to take some of the chips off the table.”5 At the Aspen Institute, the question on many people’s minds was whether Icahn was right in believing that Netflix had peaked. The company was spending unprecedented sums of money on its international expansion and original content, which left some wondering whether that level of investment was sustainable even as its domestic membership growth slowed considerably.

become bigger and bigger brands that down the road will become subscriber events as they grow.7

BACKGROUND

Original content was programming that was funded and distributed by cable network providers instead of being purchased from third-party studios and distributors. Although original content was as old as television, modern original content was more often associated with adult-oriented television series such as Sex and the City and Boardwalk Empire that, due to broadcast regulations, could be offered only on cable network channels.

Netflix began to offer original content in 2013 in an attempt to reduce its dependence on third-party studios and distributors for content. The company’s first original show was House of Cards, an American political thriller. More recent series were designed to appeal to broader demographic segments, both within the United States and internationally, which meant not only providing audio and subtitles in multiple languages but also creating stories that crossed cultural and political boundaries. The series Sense8, for example, centred on eight individuals who had a paranormal connection to each other, despite being located in various parts of the world. Filmed entirely on site in the United States, Germany, Iceland, the United Kingdom, Kenya, India, Mexico, and South Korea, the program utilized local actors and crews and was dubbed into various languages.

Netflix broke new ground in 2015 with the original series Narcos, a Spanish-language series chronicling the life of Colombian drug lord Pablo Escobar. Narcos featured a Brazilian film star in the lead role and was made by a French production company. Not only did Narcos become the top foreign-language television series of all time, some estimated that it surpassed HBO’s Game of Thrones as the most viewed TV series in any language.8

Even as Netflix sought to develop more international programming, it began to wind down some of its U.S.-based content partnerships. “I don’t think we will enter into large scale output deals in the U.S.

Competition

The goal is to become HBO faster than HBO can become us.

— Ted Sarandos, chief content officer, Netflix, Inc.14

Traditionally, content producers developed programming for regional markets. For example, French programs were developed for France, and British programs were developed for the United Kingdom. More recently, however, some content had been sold to specific foreign markets. For instance, popular British Broadcasting Corporation (BBC) programs such as Doctor Who, Downton Abbey, and Top Gear were often more popular in America than in their home market. Similarly, Mexican and South American telenovelas were popular with U.S. Spanish speakers, while dubbed versions found audiences as far away as Russia and the Balkans.15 Yet, many producers struggled with the concept of global content rights, which represented a paradigm shift in the way content was distributed. Sarandos noted that it was “a structural change that I think all of our studio partners are wrestling with. We are kind of alone in this space of buying global rights.”16

As Netflix began to acquire rights to more foreign programs, it also began to drive up the costs of those acquisition rights by as much as 50 per cent. In late 2015, when Netflix outbid the BBC for a new television series about the life of Queen Elizabeth II, titled The Crown, BBC’s director of content lamented that he “just couldn’t compete with the money.”17 Sarandos countered that other media companies, such as Amazon and Hulu, were to blame for driving up costs. “We are disciplined enough to pass when prices get irrational,” he said.18

Hulu

Founded in 2007, Hulu was a joint venture of Fox Broadcasting, NBC Universal, and Disney. Whereas Netflix originally focused on feature films, Hulu specialized in television programming, including new releases and back catalogues. Unlike Netflix, Hulu had a two-tier model of subscription-based and advertising-supported programming. At the basic level, anyone could view a limited number of programs for free, but, similar to cable and broadcast programs, the programming was periodically interrupted by advertisements. Paid subscribers could view a broader selection of shows for $7.99 per month that included both advertising-supported television shows and ad-free feature films. In late 2015, Hulu announced a third tier of commercial-free programming for $11.99 per month.19 Hulu’s catalogue

included the Criterion Collection, a distributor of award-winning and art-house feature films, primarily from the early to mid-20th century.

Initially, Hulu and Netflix were complementary services. However, as Hulu expanded into feature films, and Netflix began to offer its own television series, they increasingly saw each other as potential threats. In 2015, Hulu offered its own original series and exclusive programming. That year, Hulu and Amazon each spent roughly $1.5 billion on original content.20

YouTube Red

In late 2015, YouTube, the Google-owned streaming service that focused on user-generated content and music videos, entered the increasingly crowded market for streaming video with YouTube Red, its own

$9.99 per month subscription service. Like Netflix, Amazon, and Hulu, YouTube Red planned to offer original content and syndicated television series. In 2016, YouTube Red planned to release at least 10 original movies and television series.21

HBO

Netflix’s foray into original programming made it a direct competitor to Home Box Office (HBO), a

Amazon

Amazon was a large online retailer that offered a “prime” service to its members. Prime initially included unlimited free two-day ship

Cross-Border Alliances

Rising costs prompted some traditional television networks both to form cross-border alliances to spread out the expenses22 and to rethink selling the

INTERNATIONAL VIDEO STREAMING

As video-streaming growth slowed in the United States, international viewership continued to grow at a rapid pace. Regional growth in Latin America, Asia, and Europe, where the demand for English language programming was largely driven by Hollywood blockbuster films, was expected to outpace the United States over the next decade.24

Europe

The United Kingdom was Netflix’s largest European market with nearly 5 million subscribers in 2015. By the end of 2015, video on demand (VOD), at 39 million subscribers, was expected to overtake

One analyst noted:

We had expectations for Netflix to be doing slightly better, but the broadcasting landscape is very locally oriented. People are also more reluctant to pay for a monthly subscription to a video service in France and Germany.31

Those that did pay for service often preferred local providers such as Wuaki.tv of Spain, which boasted

China

China was arguably the largest video-streaming market in the world with 433 million viewers in 2015, generating an estimated $3.86 billion in revenues for Chinese streaming-video services.37 Prior to Netflix entering the market, many Chinese subscribed to its service through virtual private networks (VPNs), which made it appear that the viewer was located in another market in an attempt to circumvent geographic restrictions. China was also the main consumer of illegal downloads for Netflix original series, such as House of Cards.38

Japan

Hulu was one of the first streaming providers to enter international markets, starting with Japan in 2011 and later expanding across Europe. After failing to win sufficient subscribers to break even, Hulu sold its Japanese service to Nippon TV in February 2014

PIRACY

Perhaps the biggest threat to Netflix was not HBO, Amazon, or overseas providers, but piracy. “Video piracy is a substantial competitor for entertainment time in many international markets,” the company declared.

Despite the ubiquity of illegal content, Brazil was Netflix’s largest non-English-speaking market with more than 3 million subscribers (see Exhibit 4). Jonathan Friedland, the chief communications officer at Netflix, believed that competing in piracy-plagued markets required high quality at low prices, aided by a simplified content licensing process.52 “In Europe you have to buy individual content licences for every movie or TV show in each country, such as France, Germany or Spain,” explained Friedland.

BLANKETING THE GLOBE

We’re aspiring to take Netflix fully global.

—Ted Sarandos, chief content officer, Netflix, Inc.61