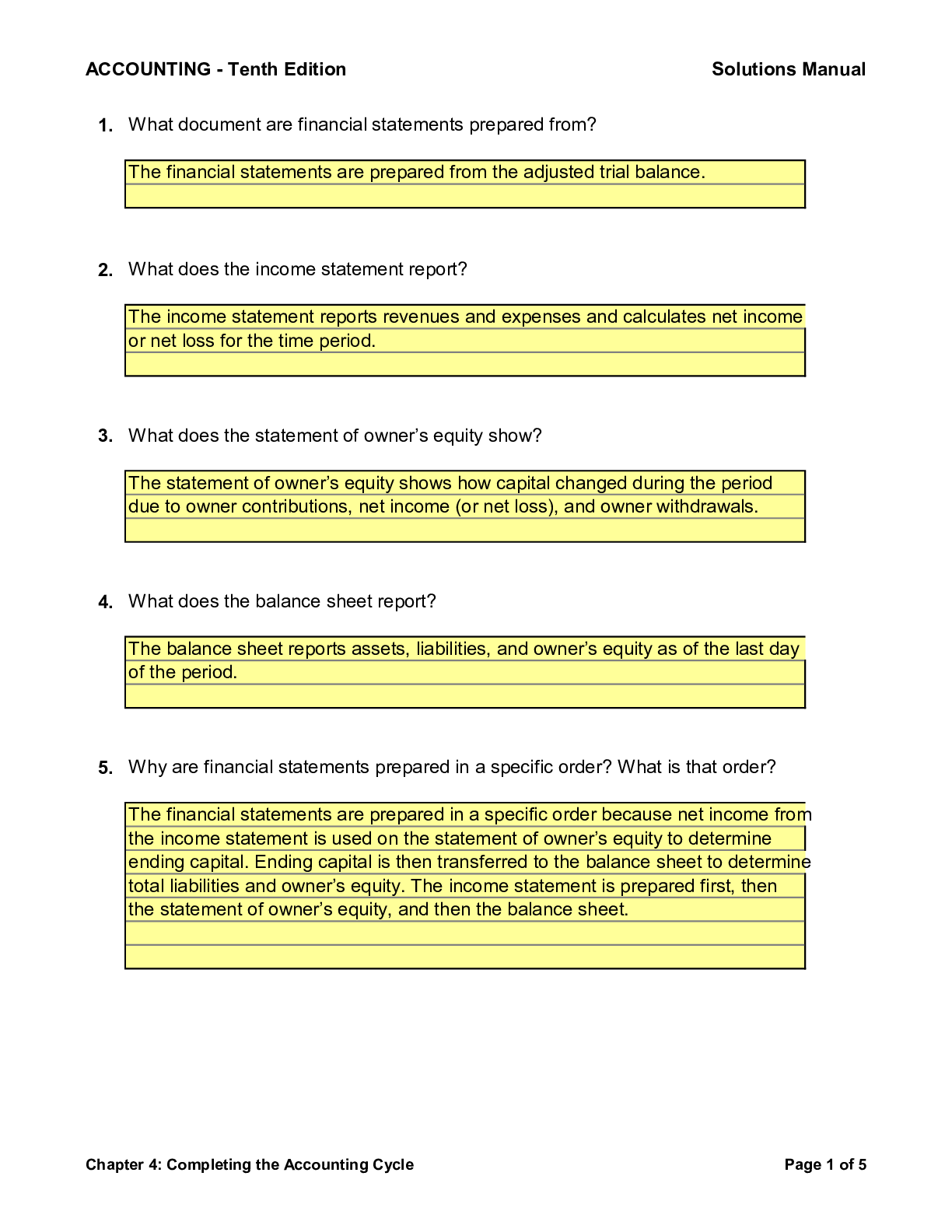

Capella University:MBA-FP6014 Assessment

Sanchez Corporation - Company records at the end of accounting period December 31, 2012: Problem 1.

Account Dollar Amount

Total Assets $ 600,000.00

Total Noncurrent assets $ 3

...

Capella University:MBA-FP6014 Assessment

Sanchez Corporation - Company records at the end of accounting period December 31, 2012: Problem 1.

Account Dollar Amount

Total Assets $ 600,000.00

Total Noncurrent assets $ 350,000.00

Liabilities Dollar Amount

Notes Payable (8% due in 6 yrs) $ 40,000.00

Accounts payable $ 60,000.00

Income taxes currently payable $ 15,000.00

Liability for withholding taxes $ 4,000.00

Rent revenue collected in advance by up to 4 months $ 8,000.00

Bonds payable (due in 15 yrs) $ 100,000.00

Wages payable $ 6,000.00

Property taxes payable $ 3,000.00

Notes Payable (10% due in 6 months) $ 22,000.00

Interest payable $ 1,200.00

Common stock $ 200,000.00

Use the informtion provided in the table to compute and answer the following for the Sanchez Corp:

1. Compute (a.) working capital and (b.) the quick ratio - quick assets are $120,000

2. Why is working capital important to management?

3. How do finanical analysts use the quick ratio?

4. Would your computations be different if the company reported $250,000 worth of contingent liabilities in th Include in your explanation a definintion of contingent liabilities and an example of a contingent liability.

t

e notes to the statements? Explain.

nces of pending litigati

on or the issuance of product warranties.

Selected data from recent financial statements of Lincoln and Samuelson, In Prob. 2, Table 1

Assets (in thousands)

Current assets: Cash and cash equivalents

Accounts receivable (net of allowances of $32 and $28 respectively)

Selected data from income statement of Lincoln and Samuelson, Inc. (in milli Prob. 2, Table 2

Account

Net sales (in millions)

Net income (in millions)

The selected income statement data is for the year ended Dec. 31. The comp Using the data provided, complete the following:

1. Compute the dollar amount of uncollectible accounts receivable that the c

2. Assuming all sales were on credit, what amount of cash did the company c

3. Compute the company's net profit margin for the 3 years presented. What

c. (dollars in thousands):

December 31, 2012 December 31, 2011

$ 4,000.00 $ 3,400.00

$ 6,500.00 $ 5,700.00

ons) :

2012 2011 2010

$6,020 $5,425 $5,000

$300 $285 $220

any also reported bad debt expense of $62,000 in 2012; $55,000 in 2011 and $49,500 in 2010.

ompany wrote off as uncollectible in 2012. Show all of your work.

ollect on accounts receivable in 2012? Show all of your work.

does the trend suggest about the company?

esn’t appear to affect it. A low net profit margin indicates the company is not ed costs

ttom margin.

The Israel Manners Entertainment Group uses the allowance approach to estimate bad debt expense, as is requir

1. How is it possible that the allowance for doubtful accounts has developed a debit balance instead of a credit b

There could have been more bad debt than what the company allowed for which resulted in a debit balance.

2. What amount of bad debt expense should be recorded for 2012?

The total bad debt expense that should be recorded for 2012 is $42,500 (Uncollectible/Doubtful Accounts) $4

3. What amount will be reported on the 2012 balance sheet as the net realizable amount of accounts receivable? The net realizale amount of accounts receivable formula is A/R - Bad Debt Expense.

A/R = $4350

Allowance for Doubtful Accounts = $42500

$4,350 - $42,500 = $4,307,500

ed of all companies with significant sales on accounts receivable. At the end of 2012, the Manners Group reporte alance.

4,000 - $1,500 (the additional debit balance) = $42,500

ed a balance in accounts recievable of $4,350,000 and estimated that $44,000 of it's accounts receivable would lik

ely be uncollectible. The allowance for doubtful accounts has a $1,500 debit balance at year-end, prior to the adj

ustment needed to raise it to the $44,000 desired amount. Use this information to answer the following question

s for the Manners group:

At the end of 2012, the unadjusted trial balance of Donovan, Inc. included $6,000,000 in accounts recei a credit balance of $50,000 in the allowance for doubtful accounts, and sales revenues (all on credit) of Based on knowledge that the current economy is in distress, Donovan increased its bad debt rate estim Use this information to answer the following questions for Donovan, Inc.:

1. What amount of bad debt expense should be recorded in 2012?

The allowance for bad debt is calculated by multiplying the sales revenue (200,000,000) by the bad deb

$200,000,000 X 0.4 = $800,000

2. What amount will be reported on the 2012 balance sheet for the net realizable amount of accounts The formula for determining the net realizable amount of accounts receivable is A/R less Allowance for (A/R) $6,000,000 - $850,000 (50,000+800,000) = $5,150,000

vable,

$200,000,000.

ate to 0.4 % on credit sales.

t rate (0.4%):

receivable, after being reduced by the balance in the allowance for uncollectible accounts? uncollectibles:

BrightStar Company Reported the following inventory records for June 2012:

Problem 2, Table 3: BrightStar Company Inventory Records

Date Activity # Units Cost/Unit

June 1 Beginning Balance 200 $40

June 5 Purchase 600 $42

June 8 Sale @ $100 per unit 500

June 17 Purchase 400 $45

June 23 Sale @ $100 per unit 500

Selling, administrative, and depreciation expenses for the month were $20,000. BrightStar's tax rate is 35 Using this information and the table above to complete the following for BrightStar Company.

1. Calculate the cost of ending inventory and the cost of goods sold under each of the following methods:

a. First in First out (FIFO)

Units Sold Cost Total

200 40 8000

300 42 12600

300 42 12600

200 45 9000

Cost of Goods Sold 42200

Ending Inventory 200 45 9000

b. Last in, first out (LIFO)

Cost of Goods Sold Ending Inventory Units Sold Cost Total

400 45 18000

100 42 4200

500 42 21000

43200

200 40 9000

Goods Sold $43,200

Cost of Ending Inventory 200 @ $45 = $9,000

c. Weighted average.

Units Purchased Cost Total

200 40 8000

600 42 25200

400 45 18000

1200 51200

Weighted Avg. = Total Cost/Total Units = 51200 / 1200 = 42.67

Ending Inventory = 200 units x 42.67 = $8533

2. Using your answers from questions 1 above, answer the following:

a. What is the gross profit percentage under the FIFO method? Sales (500 +500)= 1000 x 100 = $100,000

Cost of goods sold $42,200

Selling, Distribution and Depr. Exps $0

Gross profit = $58,000 (sales less cost of goods sold less selling , distribution & depr)

Gross profit percentage = 58 % (gross profit/net sales)

b. What is net income under the LIFO method? Sales = (500+500) 1000 units x $100 + $100,000 cost of goods sold = $43,200

Gross profit = $56,800

Selling, Admin & Depreciation expenses = $20,000 Income from Ops = $36,800

Tax @ 35% = $12,880

Net Income = $23,920

c. Which method would you recommend to BrightStar for tax purposes? Explain your recommendation.

I would recommend theWeighted Average method because it will result in a lower tax on income and yi

FIFO LIFO Weighted Avg

Sales = (500+500) 1000 x $100 $100,000 $100,000 $100,000

Cost of goods sold ($42,200) ($43,200) ($512,000)

Gross profit $58,000 $56,800 $48,800

Selling, Admin & Depreciation ($20,000) ($20,000) ($20,000)

Net Income Pretax $38,000 $36,800 $28,800

Tax @ 35% ($36800 x 35%) $13,300 $12,880 $10,080

Net Income (Post Tax) $24,700 $23,920 $18,720

d. If BrightStar also used the method that you recommend for tax purposes on its balance sheet , would Br

Using the Weighted Average method would not affect their current ratio as opposed to using the FIFO m

3. BrightStar uses the lower of FIFO cost or market method to value its inventory for reporting purposes at BrightStar would report the market value of $44 per unit @ 200 units ($8,800) because they would be repo

$44 x 200 = $8800

%.

ightStar's current ratio suffer, compared to the use of FIFO?

ethod. Weighted Average means lower tax expenses. The FIFO would be a higher tax laibility due to current ass

the end of the month. If inventory had a market replacement value of $44 per unit, what would be BrightStar rep rting the lower cost of inventory with FIFO.

ets being divided by current liabilities, which would negatively impact the current ratio.

ort in its balance sheet for inventory? Why?

BlackBurn Company purchased the following on Januray 1, 2012:

Office equipment at a cost of $10,000 with an estimated useful life to the company of 5 year Factory equipent at an nvoice price of $780,000 plus shipping costs of $20,000. The equipme A patent at a cost of $450,000 with an estimated useful life of 15 years. The company uses th Use the information above to complete the following for BlackBurn Company:

1. Prepare a partial depreciation schedule for 2012, 2013, and 2014 for the following assets.

a. Office equipment.

Account Office Equipment

Cost $100,000

Residual Value $10,000

Life 5

Rate 0.4

Year Beginning Value

2012 $100,000

2013 $60,000

2014 $36,000

b. Factory equipment. The company used the equipment for 8,000 hours in 2012; 9,000 hour

Account Office Equipment

Invoice Price $780,000

Shipping cost $20,000

total $800,000

Life (hours) $100,000

Usage Cost/Hours

2012 8 * 8000

2013 8 * 9000

2014 8 * 8500

2. On January 1, 2014, BlackBurn altered its corporate strategy dramatically. The company so

Factory Equipment price sold - $700,000

3. On January 1, 2014, when the company changed its corporate strategy, its patent had esti What would the company report on the income statement (account and amount) regarding t

Yearly Amortization = (cost of patent)/ estimate

Accumulated Depreciation for 2012 & 2013 = (30, Book Value on January 2, 2014 = (Cost of patent l Fair Value = $250,000

Year Opening Book Value Depreciation

2012 $100,000 $40,000

2013 $60,000 $24,000

2014 $36,000 $14,000

s and a residual vaue of $10,000. The company uses the double-declining-balance method of depreciation for the nt has an estimated useful life of 100,000 hours and no residual value. The company uses the units-of-production e straight-line method of amortization for intangible assets with no residual value.

Round your answers to the nearest dollar.

The double declining method is 2 x (1/estimated useful life) x cost of the asset = 0.4% or 40%

Ending Value

$60,000

$36,000

$21,600

s in 2013; and 8,500 hours in 2014.

800000/10000 hrs = $8 (Cost)

Depreciation method is number of production hours

Depreciation = Cost/Total Usage x Hours used = $8.00

ld the factory equipment for $700,000 in cash. Record the entry related to the sale of the factory equipment.

mated future cash flows of $300,000 and a fair value of $250,000.

he patent on January 2, 2014? Explain your answer. (Hint: You may need to research this question using Internet s

d patent life in years 450000/15 = $30,000

000 x 2) $60,000

ess accumulated depreciation) $450,000 - $60,000 = $390,000

Accumulated Depr Ending Book Value

$40,000 $60,000

$64,000 $36,000

$78,400 $21,600

equipment.

method of depreciation for the equipment.

ources.)

[Show More]