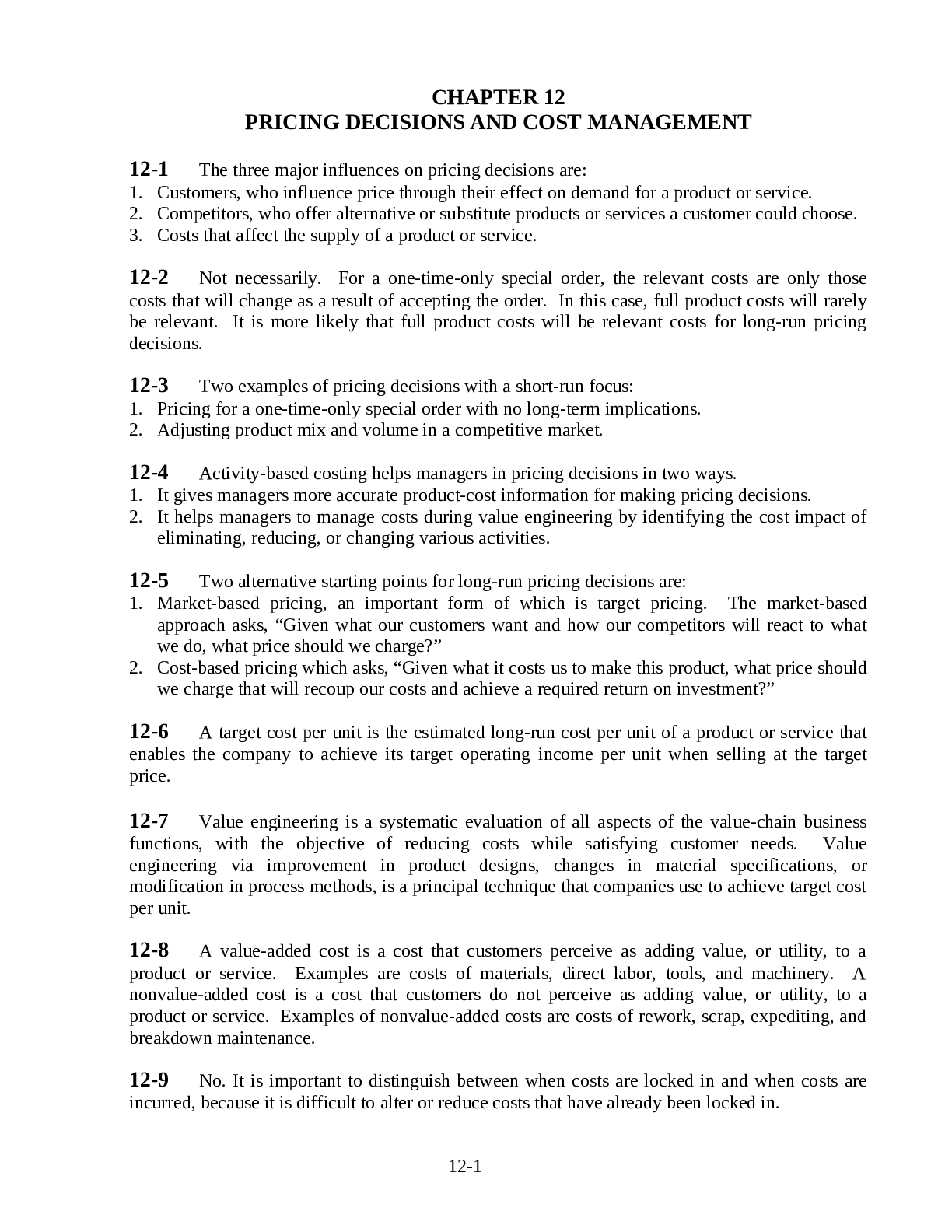

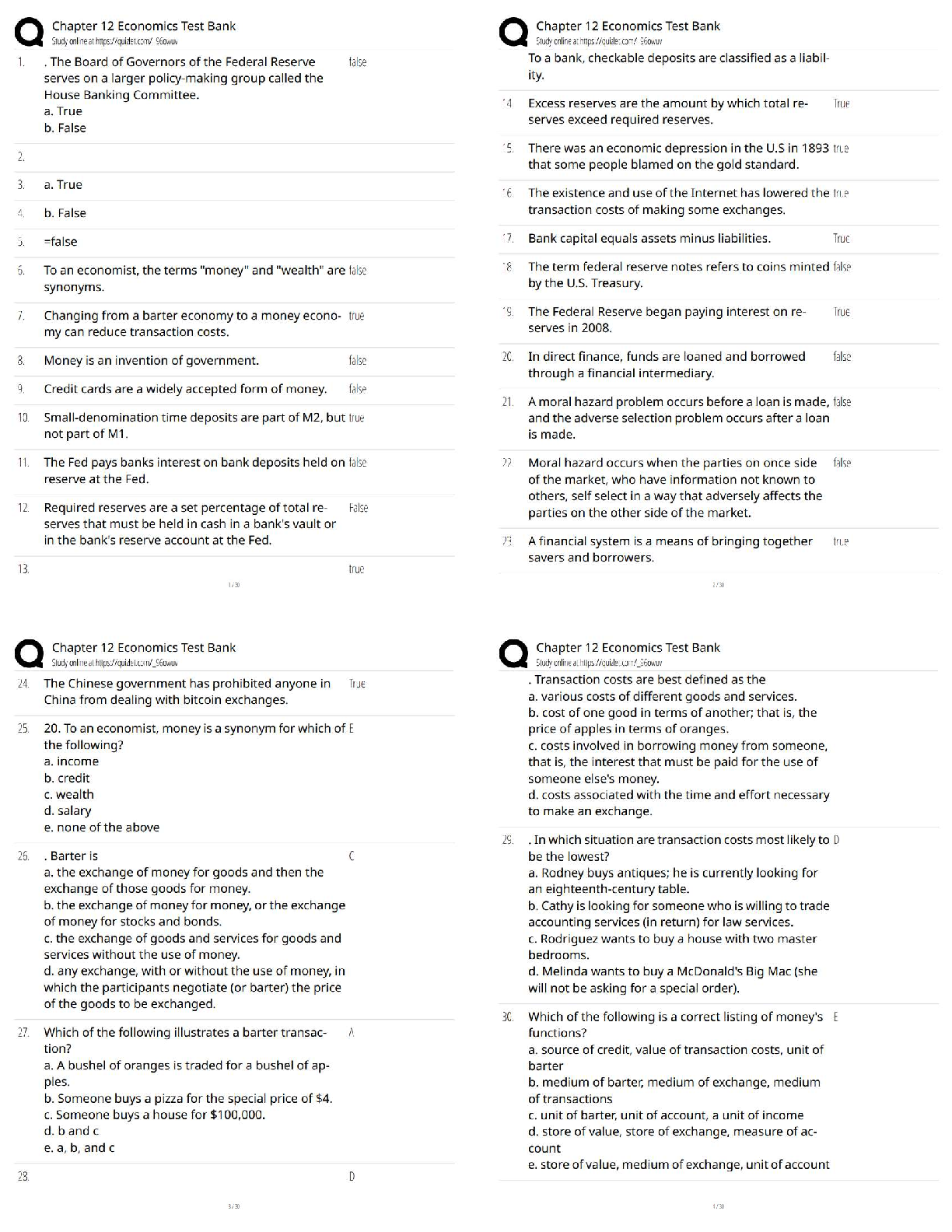

Marketing > QUESTIONS & ANSWERS > CHAPTER 12 PRICING DECISIONS AND COST MANAGEMENT: ANSWERS (All)

CHAPTER 12 PRICING DECISIONS AND COST MANAGEMENT: ANSWERS

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 49 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jun 25, 2021

Number of pages

49

Written in

All

Additional information

This document has been written for:

Uploaded

Jun 25, 2021

Downloads

0

Views

120

Document Keyword Tags

Recommended For You

Get more on QUESTIONS & ANSWERS »

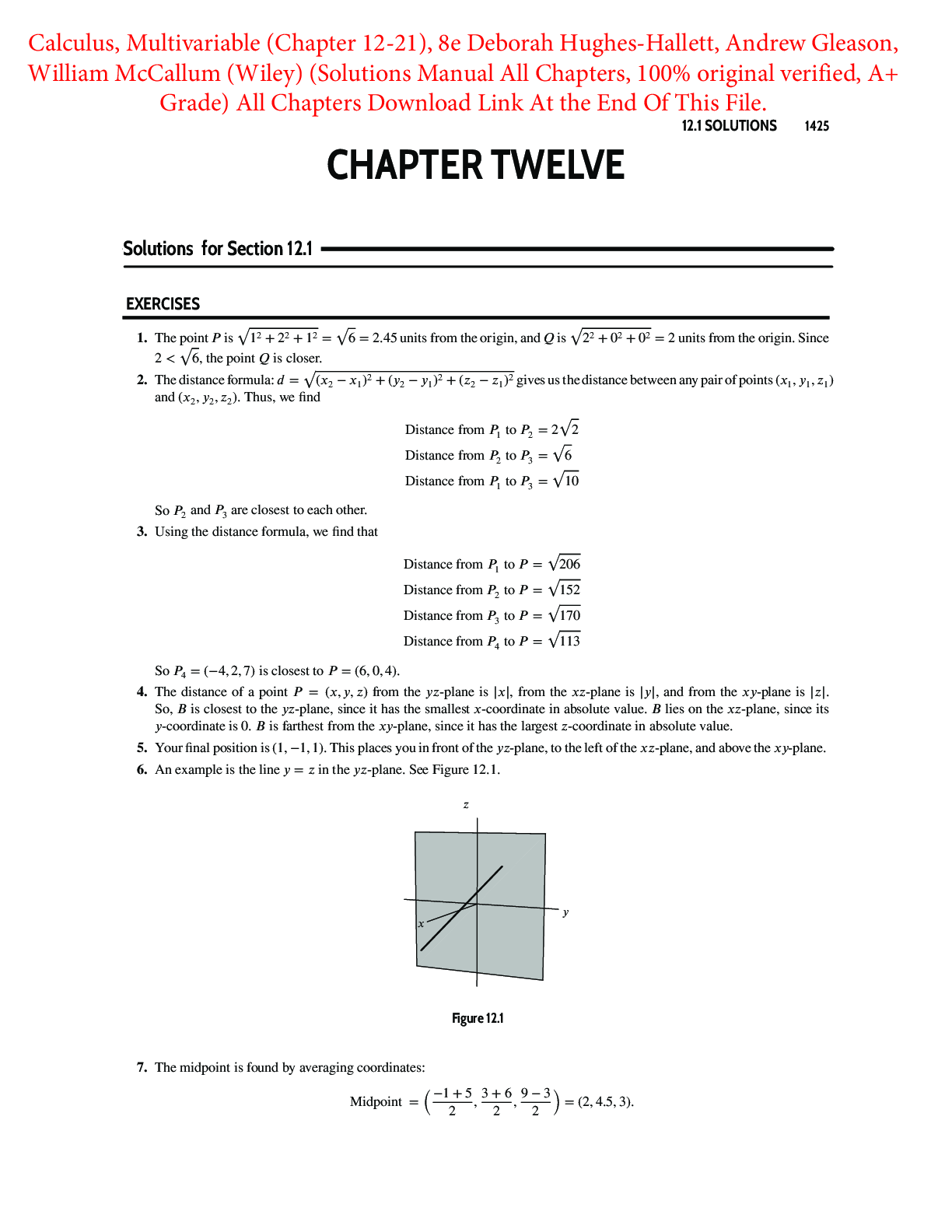

Calculus, Multivariable (Chapter 12-21) 8th Edition By Deborah...

BIOS 254 Chapter 12_13 Lecture HW Questions and Answers (Ve...

BIOS 105 Chapter 12 Questions and Answers (Verified Answers)

Chapter 11 Motivation and Emotion, Chapter 12 Stress and Healt...

![Preview of [eBook] [PDF] Business Marketing Management B2B 13th Edition By Michael Hutt, Thomas Speh,](https://browseimages.nyc3.digitaloceanspaces.com/paper-images/2025/Jul/03/e2JUBlpQ2025-07-03-02-106865bc4811a72.png)

[eBook] [PDF] Business Marketing Management B2B 13th Edition B...

eBook PDF Consumer Behavior 8th Edition By Wayne D. Hoyer, Deb...

.png)