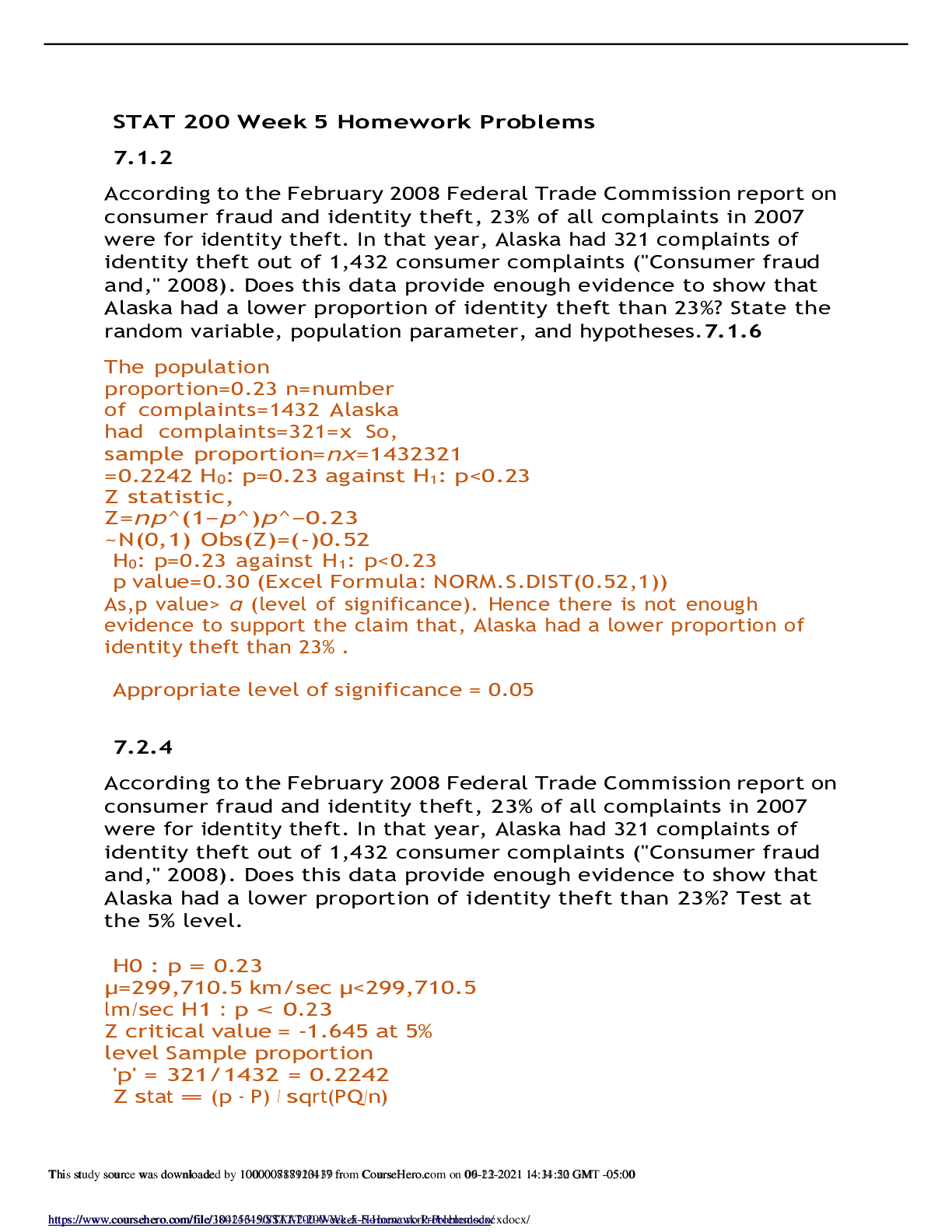

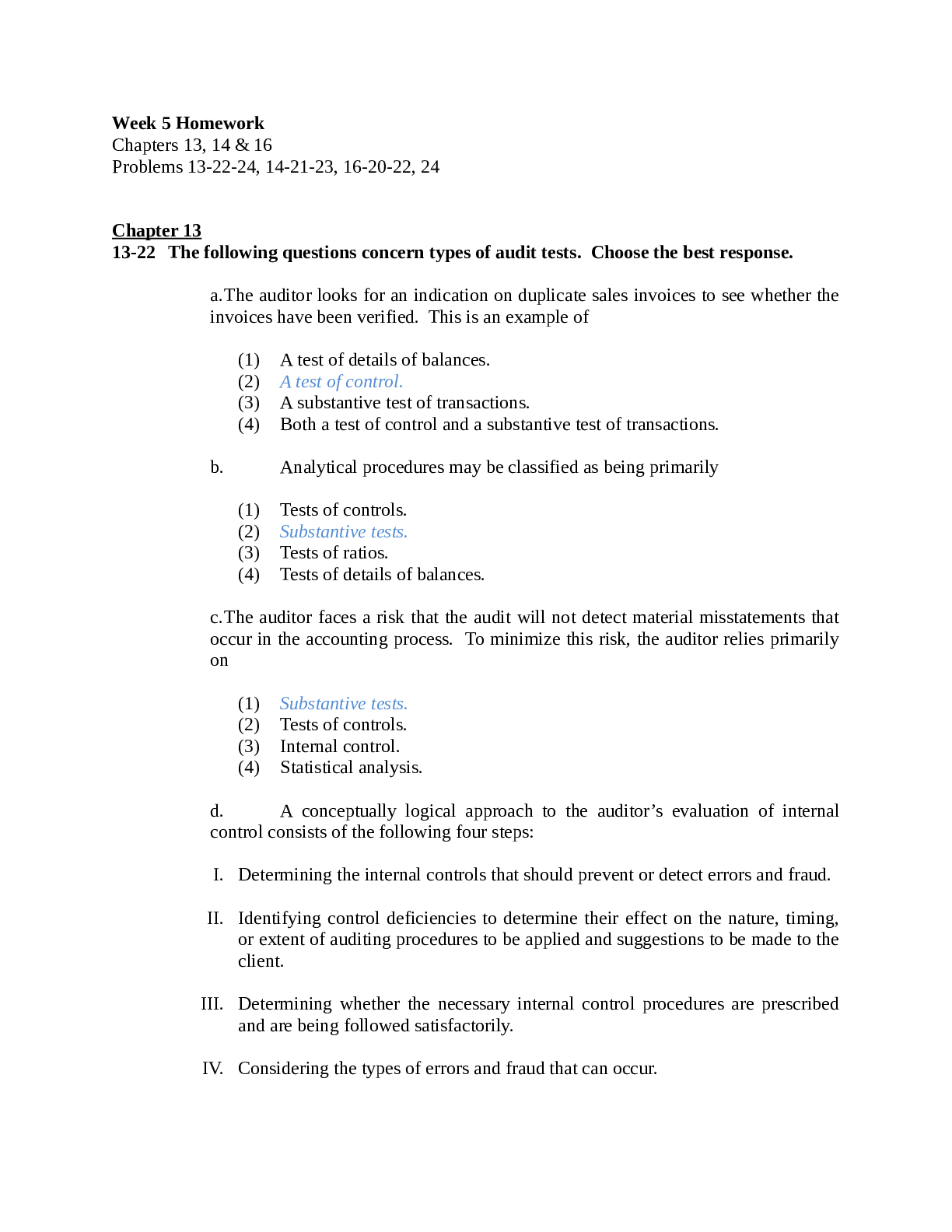

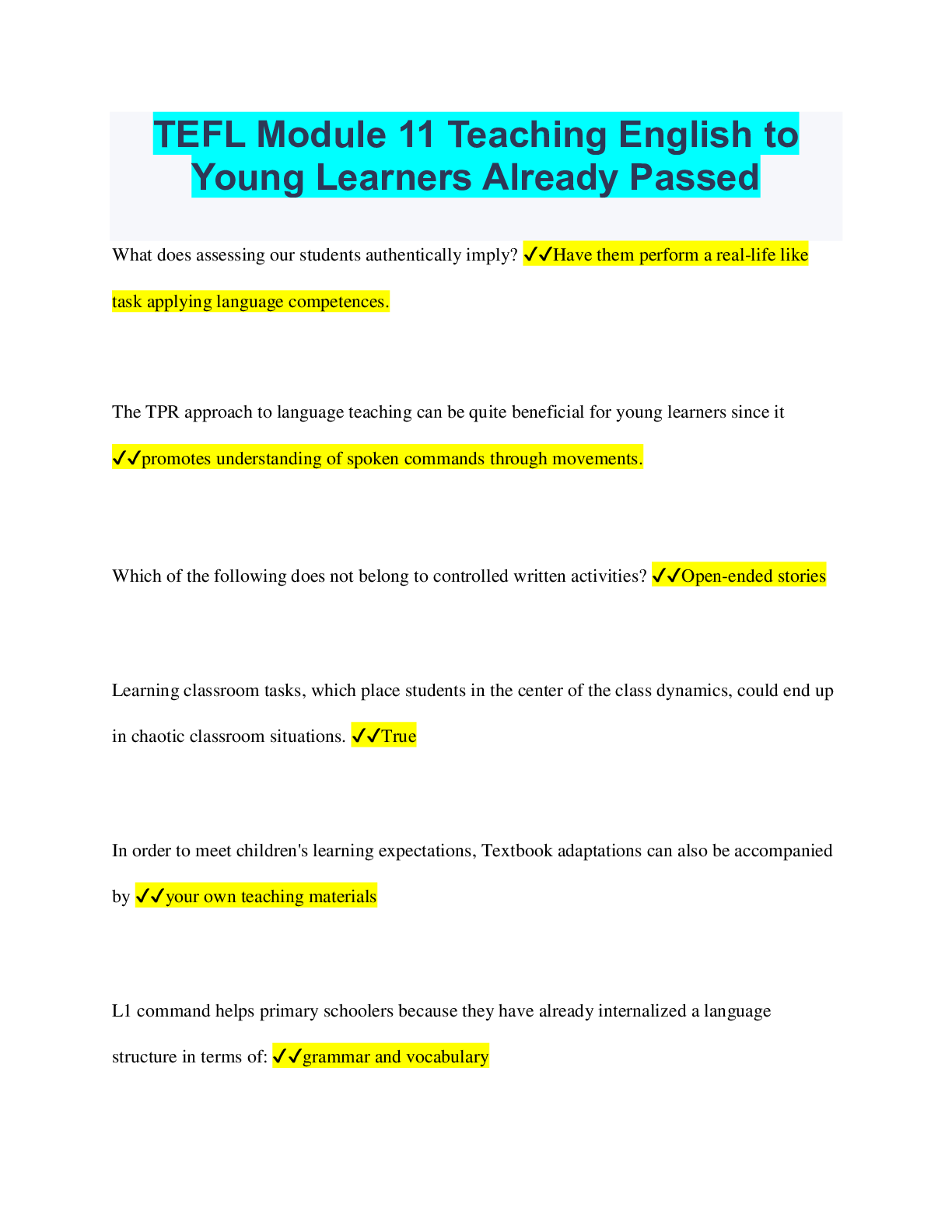

Financial Accounting > QUESTIONS & ANSWERS > ACCT 212 Week 5 Homework Questions and Well Explained Answers Recommended for Scoring A+ (All)

ACCT 212 Week 5 Homework Questions and Well Explained Answers Recommended for Scoring A+

Document Content and Description Below

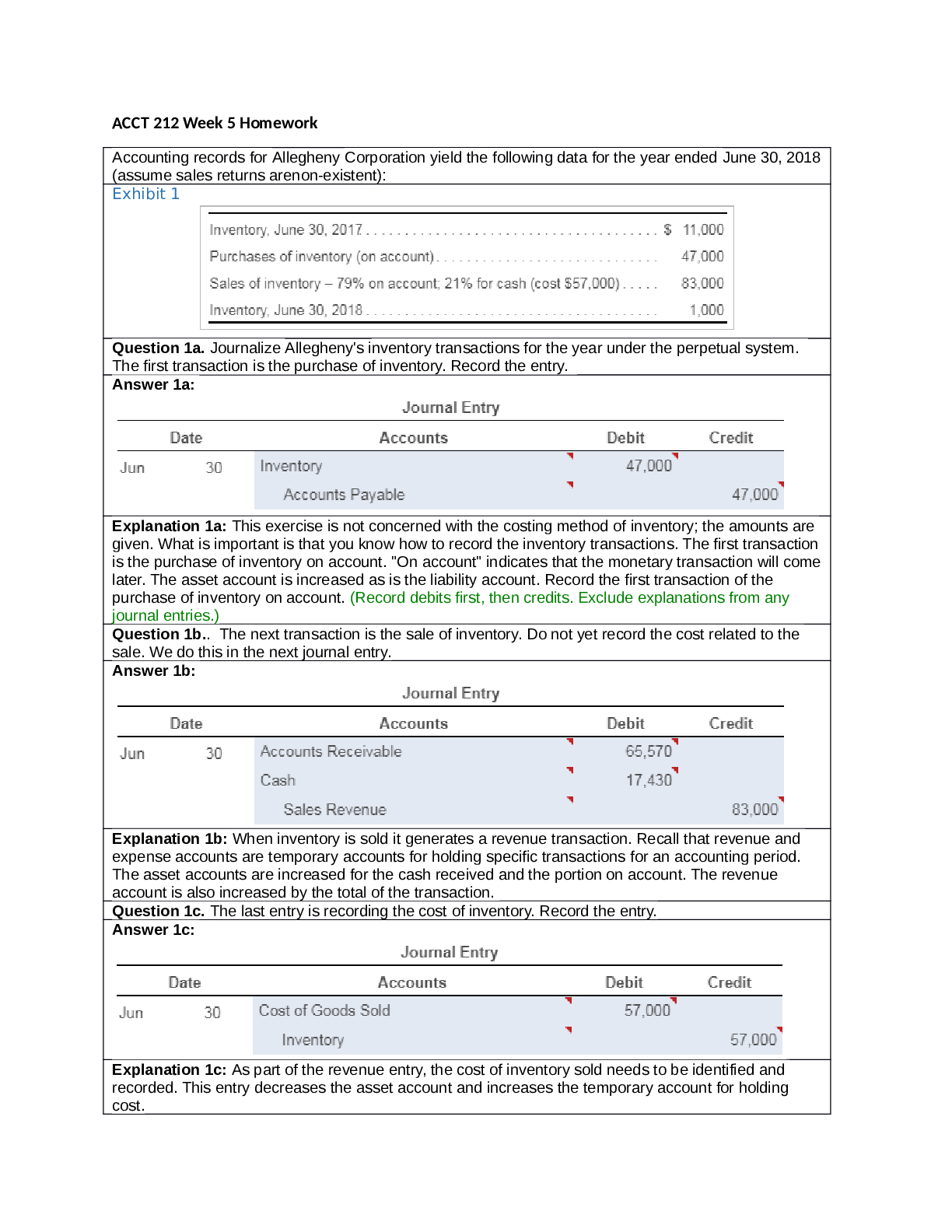

Accounting records for Allegheny Corporation yield the following data for the year ended June 30, 2018 (assume sales returns arenon-existent): Exhibit 1 Question 1a. Journalize Allegheny's inventor... y transactions for the year under the perpetual system. The first transaction is the purchase of inventory. Record the entry. Answer 1a: Explanation 1a: This exercise is not concerned with the costing method of inventory; the amounts are given. What is important is that you know how to record the inventory transactions. The first transaction is the purchase of inventory on account. "On account" indicates that the monetary transaction will come later. The asset account is increased as is the liability account. Record the first transaction of the purchase of inventory on account. (Record debits first, then credits. Exclude explanations from any journal entries.) Question 1b.. The next transaction is the sale of inventory. Do not yet record the cost related to the sale. We do this in the next journal entry. Answer 1b: Explanation 1b: When inventory is sold it generates a revenue transaction. Recall that revenue and expense accounts are temporary accounts for holding specific transactions for an accounting period. The asset accounts are increased for the cash received and the portion on account. The revenue account is also increased by the total of the transaction. Question 1c. The last entry is recording the cost of inventory. Record the entry. Answer 1c: Explanation 1c: As part of the revenue entry, the cost of inventory sold needs to be identified and recorded. This entry decreases the asset account and increases the temporary account for holding cost. Question 1d. Report ending inventory, sales, cost of goods sold, and gross profit on the appropriate financial statement. Answer 1d: Explanation 1d: The balance sheet reports assets, liabilities and equity of a company at the end of an accounting period. Report the appropriate asset account on the balance sheet. Question 1e. Report sales, cost of goods sold, and gross profit on the income statement: Explanation 1e: Recall that the income statement reports the earnings and expenses of a business over a period of time. Gross profit is the sales revenue reduced by the cost of goods sold. The higher the gross profit, the better for the business. Remember, gross profit is just a starting point. Business expenses have to be subtracted from gross profit to derive net profit. Answer 1e: (Click here to view Exhibit 1 Inventory, June 30, 2018 ) Ken Company's inventory records for its retail division show the following at March 31. At March 31, 11 of these units are on hand. Compute cost of goods sold and ending inventory, using each of the following four inventory methods. (Notes: Accounting uses four generally accepted inventory methods. A company can use any of these methods. The methods can have very different effects on reportedprofits, income taxes, and cash flow. Therefore, companies select their inventory method with great care.) Exhibit 2 Question 2a. Calculate the cost of goods sold and ending inventory using the Specific Identification method with Seven $165 units and four $175 units still on hand at the end Answer 2a: Specific identification, with seven $165 units and four $175 units still on hand at the end Beginning inventory = 9 -7 =2 (See Cost $165) 15 Purchase = Same (See Cost $166) 26 Purchase = 13 - 4 (See Cost $175) 2 Now let's calculate the ending inventory using the specific identification method. We have been told that the following are still on hand at the end of the period: seven $165 unit(s) and four $175 units. Explanation 2a: To compute cost of goods sold and the cost of ending inventory still on hand, we must assign a cost to each unit. Generally, the specific identification method is used only by businesses that deal in unique inventory items, such as automobiles, antiquefurniture, jewels, and real estate. This method is too expensive to use for inventory items that have common characteristics, such as bushels of wheat, gallons of paint, or auto tires. We have been told that the following are still on hand at the end of the period: seven $165 unit(s) and four $175 units. We know that there were 9 $165 units (beginning inventory), 5 $166 units (Mar 15 purchase), and 13 $175 units (Mar 26 purchase) available during the period. Therefore, we can determine how many of each specific unit was sold. Question 2b. Now let's calculate the the cost of goods sold and ending inventory using the Average cost method Answer 2b: Cost f Goods Available = $2,735+$1,855=$4590 Number of Units Available = 9+5+13?? (See Above) = 27 (Maybe 16+11) Average Cost = (165+166+175)/3=$170 The average cost per unit you calculated above will be used to compute the cost of goods sold. Now calculate ending inventory using the average cost method. Explanation 2b: The average cost method, is based on the average cost of inventory (available for sale) during the period. All of the units available forsale, regardless of their purchase price, are given the same unit cost under this method. Begin by calculating the average cost per unit that will be assigned to each unit in ending inventory and cost of goods sold. We know from See Above that Ken had 27 (9+5+13) units available for sale and we also know from the information provided that there are 11 units left at the end of the period. Therefore, 16 units were sold.. (Round your answer to the nearest whole dollar.) Question 2c. Now let's calculate the cost of goods sold and ending inventory using the First-in, firstout (FIFO) method. Remember, Ken Company's inventory records for its retail division show the following at March 31. At March 31, 11 of these units are on hand. Answer 2c: Determine the amount of inventory in each of the last two layers. Think carefully, there are 11 units in ending inventory. Is that greater than or less than the amount of inventory purchased on the 26th? Use the discussion above to help you determine the ending inventory cost layers. (Enter an amount in each input area, including a "0" for zero balances.) Explanation 2c: Under the FIFO method, the first costs into inventory are the first costs assigned to cost of goods sold—hence, the name first-in, first-out. Under FIFO, the cost of ending inventory is always based on the latest costs incurred. When using FIFO we look at the beginning inventory and each purchase of inventory as being separate layers, with each layer having its own cost. Remember, with FIFO the units sold are assigned the oldest costs first, so the units remaining in ending inventory will have the most recent costs assigned to them. In this exercise, the most recent cost is from the purchase on the 26th. Remember, the units sold are assigned the oldest costs first. We know that Ken sold a total of 16 units. There were 9 units in beginning inventory; therefore, 9 of the units sold will be assigned a cost of $165 per unit. There were 5 units available from the Mar 15 purchase and 13 units available from the Mar 26 purchase. Now we need to determine the layers that remain in the ending inventory. In other words, will all the units in ending inventory be assigned the cost from the purchase on the 26th? Or will there be an additional layer, the cost from the purchase on the 15th, in ending inventory? Since each purchase is considered its own layer, only the 13 units purchased on the 26th can be assigned the cost of $175 per unit. If the units in ending inventory are equal to or less than the amount of units purchased on the 26th, all of the units in ending inventory will be assigned that unit cost. If the units in ending inventory are greater than the units that were purchased on the 26th, then 13 of the units will have a unit cost of $175, while the rest of the units will have a unit cost from the next most recent purchase, in this case the purchase on the 15th, of $166 per unit. Question 2d. Now let's calculate the cost of goods sold using the Last-in, first-out (LIFO) method Answer 2d: Now calculate ending inventory using LIFO. Explanation 2d: LIFO costing is the opposite of FIFO. Under LIFO, the last costs into inventory go immediately to cost of goods sold. Under LIFO, the cost of ending inventory is always based on the oldest costs—from beginning inventory plus the early purchases of the period. To calculate the cost of goods sold using LIFO, remember, the most recent purchases will be assigned first. Ken sold 16 units, but there were only 13 units in the most recent inventory layer. (Enter "0" for any zero balances.) We know from the step above that Ken assigned all the costs from the Mar 26 purchase and a portion of the Mar 15 purchase to cost of goods sold. Therefore, we know that we must subtract the cost of goods sold from the original inventory shown in the diagram below Beginning Inventory 9 – 0= 9x$165 Mar 15 Purchase 5 – 3=2x$166 Mar 26 Purchase 13 – 13=0x$175 Question 2e. Which method produces the highest cost of goods sold? Which method produces the lowest cost of goods sold? What causes the difference in cost of goods sold? Answer 2e: Explanation 2e: Let's review the cost of goods sold under each method to determine which method produces the highest and which method produces the lowest cost of goods sold. What are the major differences between the methods in calculating the cost of goods sold? Refer to the information given to you and determine how the trend in purchase prices would affect the cost assigned to the units sold under these methods. The Dockside Shop had the following inventory data: Question 3a. Company managers need to know the company's gross profit percentage and rate of inventory turnover for 2018 under: 1. FIFO 2. LIFO Answer 3a: Inventory turnover, the ratio of cost of goods sold to average inventory, indicates how rapidly inventory is sold. Begin by calculating average inventory under the FIFO and LIFO methods. Now calculate the inventory turnover under the FIFO and LIFO methods. (Round answer one decimal) Explanation 3a: Gross Profit sales minus cost of goods sold is a key indicator of a company's ability to sell inventory at a profit. Merchandisers strive to increase gross profit percentage, also called the gross margin percentage. Gross profit percentage is markup stated as a percentage of sales. Go ahead and calculate the gross profit percentage under the FIFO and LIFO methods. Remember that gross profit is sales revenue reduced by cost of goods sold. (Enter the percentage to the nearest tenth of a percent, X.X%.) (Sales Revenue) $144,500 – (FIFO COGS) $89,590/ (Net Sales) 144,500 = 0.38 or 38% (Sales Revenue) $144,500 – (LIFO COGS) $101,150/ (Net Sales) 144,500 = 0.30 or 30% Question 3b. Which method produces a higher gross profit percentage? A higher inventory turnover? Answer 3b: Which method produces a higher gross profit percentage? FIFO A higher inventory turnover? LIFO Explanation 3b: As stated above, gross profit sales minus cost of goods sold is a key indicator of a company's ability to sell inventory at a profit. Each percentage point of gross margin percentage equates to 1 cent of gross profit for each dollar of sales. As a result companies want to achieve the highest gross profit percentage possible. Inventory turnover is a measurement tool for determining how quickly inventory is sold. A business strives to sell its inventory as quickly as possible because the goods generate no profit until they're sold. The faster the sales, the higher the income, and vice versa for slow-moving goods. Based on the calculations you performed above and knowing that companies strive for high ratios, which method makes Dockside look better? Camp Surplus began July 2018 with 60 stoves that cost $10 each. During the month, the company made the following purchases at cost: The company sold 247 stoves, and at July 31, the ending inventory consisted of 53 stoves. The sales price of each stove was $44. Question 4a. Determine the cost of goods sold and ending inventory amounts for July under the average-cost, FIFO, and LIFO costing methods. Round the average cost per unit to two decimal places, and round all other amounts to the nearest dollar. Answer 4a: Using the calculations from the previous step, we can calculate the average cost per unit that will be assigned to each unit in ending inventory and cost of goods sold. The average cost per unit you calculated above will be used to compute the cost of goods sold and ending inventory. Let's begin with cost of goods sold. Now calculate ending inventory using the average cost method. Explanation 4a: The average cost method is based on the average cost of inventory during the period. All of the units available for sale, regardless of their purchase price, are given the same unit cost under this method. Before we calculate the average cost per unit, we need to determine the cost of goods available. Determine the units and cost of goods available as well as the number of units in ending inventory and sold. Fetermine the answers to the circled areas. 1. First Column a. The Qty for the “Beginning Inventory” is given to you as a part of the question = 60 [Show More]

Last updated: 2 years ago

Preview 1 out of 13 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

Reviews( 0 )

$10.00

Can't find what you want? Try our AI powered Search

Document information

Connected school, study & course

About the document

Uploaded On

Aug 02, 2021

Number of pages

13

Written in

Additional information

This document has been written for:

Uploaded

Aug 02, 2021

Downloads

0

Views

111

.png)

.png)