Financial Accounting > LECTURE SLIDES/NOTES > ACCT 3330-ch21 (All)

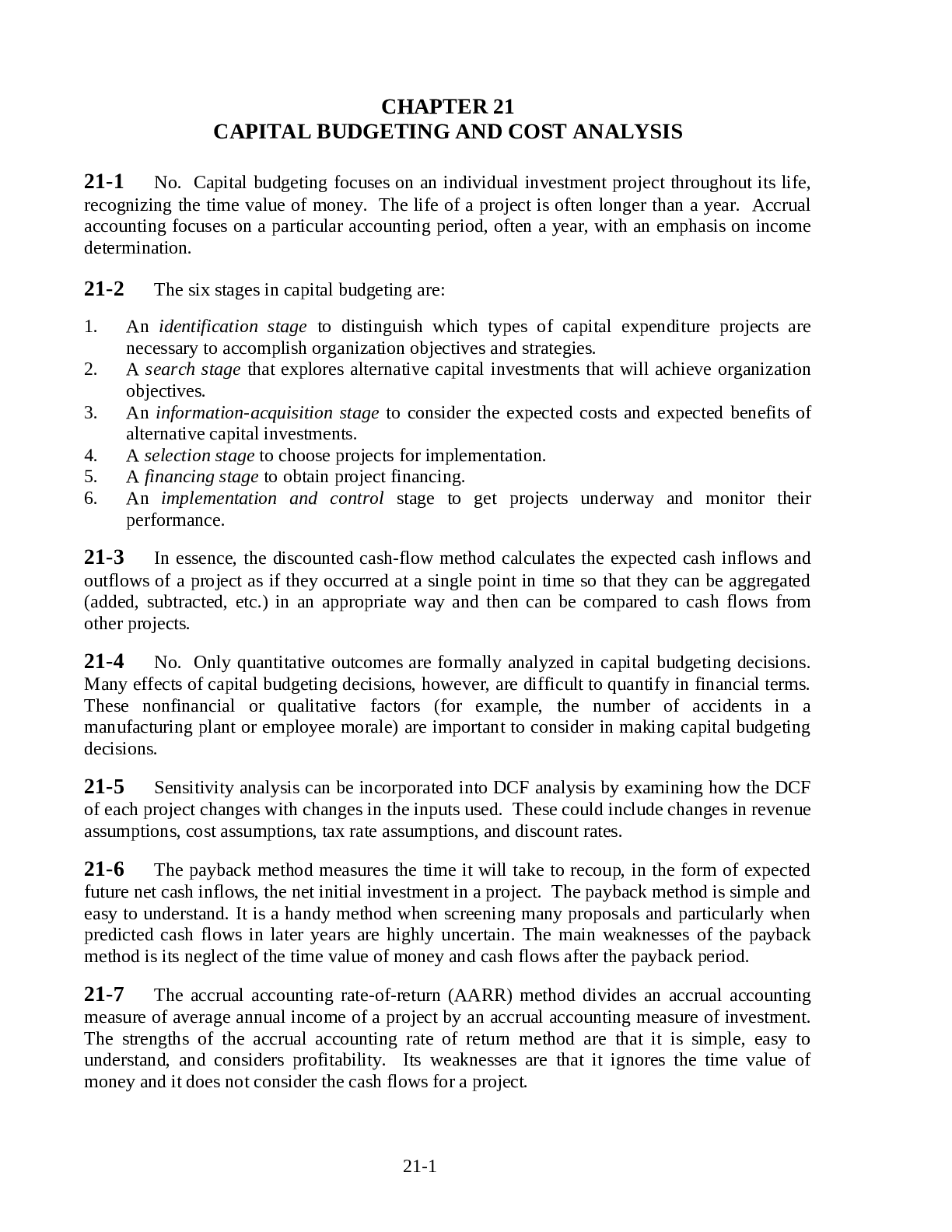

ACCT 3330-ch21

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 49 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jun 19, 2021

Number of pages

49

Written in

All

Additional information

This document has been written for:

Uploaded

Jun 19, 2021

Downloads

0

Views

162

Document Keyword Tags

Recommended For You

Get more on LECTURE SLIDES/NOTES »

California State University, San Bernardino - ACCT 536ACCT 536...

Learning Sage 50 Accounting 2020 A Modular Approach 21st Editi...

Chapter 26 Respiratory System, BH7 HEME, L7 CARDIAC, L7 26: Nu...

Test Bank - Lewis's Medical Surgical Nursing ch20 & ch21

Test Bank - Lewiss Medical Surgical Nursing ch20 & ch21.

Test Bank - Lewiss Medical Surgical Nursing ch20 & ch21.pdf

NR 226: Exam 1 (Ch. 21 (Managing Care) Ch. 22 (Ethics and Valu...

MCB Practice Quiz Ch20, Ch21,Ch22,Ch23,Ch24,Ch25,Ch26. Questio...

Marquis Leadership 8e Ch 21: Managing Conflict -Exam Graded A+

Week 3-National Certification Study Plan Holly Bowling College...

A&P Ch. 21 Integumentary System with 100% Verified Solutions |...

Financial Accounting with International Financial Reporting St...

.png)