Finance > Study Notes > AF 4207 – L6 FINANCIAL REPORTING II (All)

AF 4207 – L6 FINANCIAL REPORTING II

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 6 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jun 18, 2022

Number of pages

6

Written in

All

Additional information

This document has been written for:

Uploaded

Jun 18, 2022

Downloads

0

Views

259

Document Keyword Tags

Recommended For You

Get more on Study Notes »

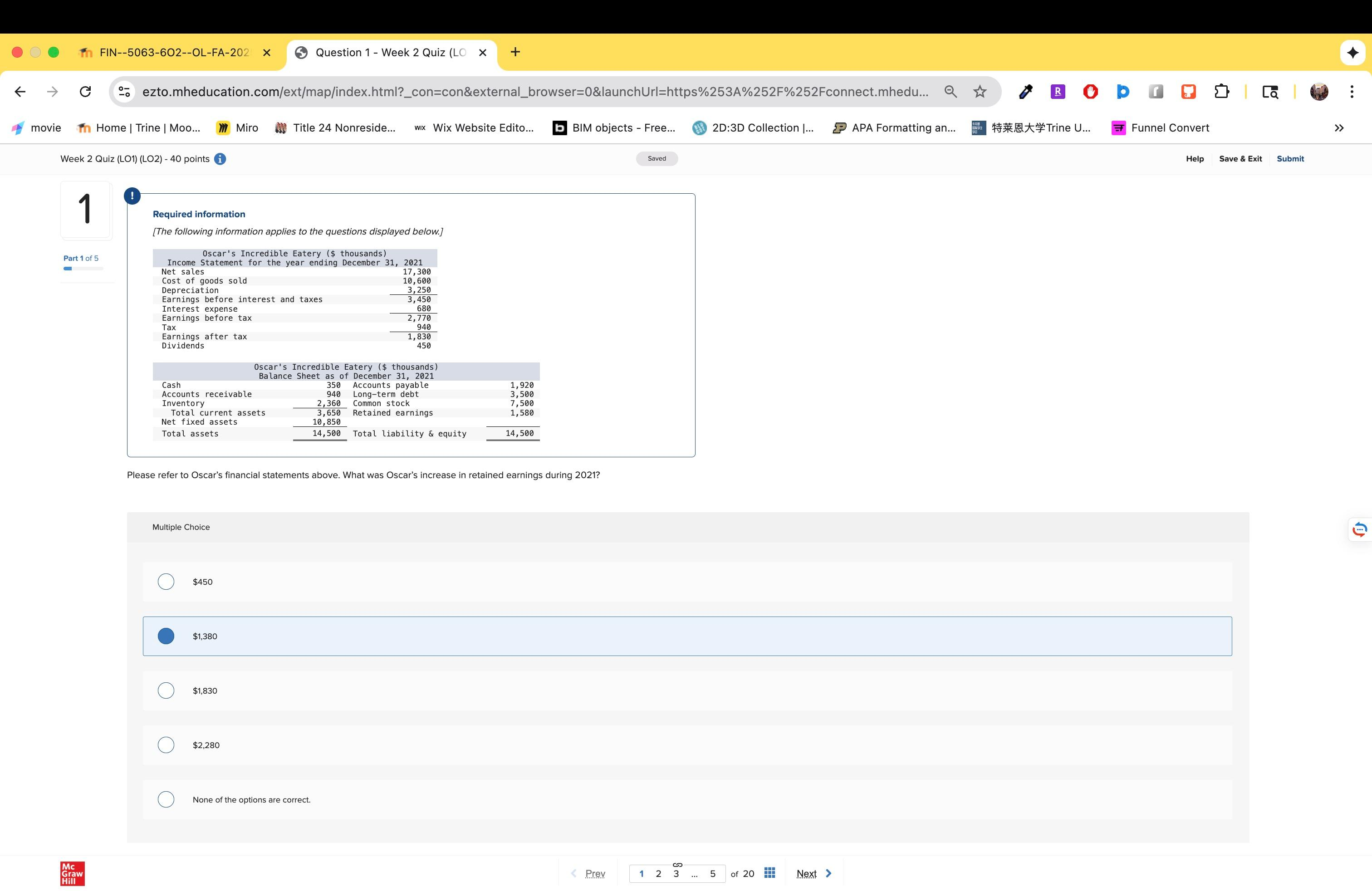

REPORTING FOR LEASES IFRS 16 AF 4207 – L6 FINANCIAL REPORTING...

Test Bank for Financial Reporting and Analysis, 8th Edition Re...

Financial Reporting and Analysis, 8e Lawrence Revsine, Daniel...

Janice Loftus, Ken Leo, Sorin Daniliuc, Noel Boys, Belinda Luke, Hong Ang, Karyn Byrnes (Test Bank).png)

Financial Reporting, 2e (Australia) Janice Loftus, Ken Leo, So...

Quiz 2 Concept Notes MY21.png)

NR304 / NR-304 Quiz 2 Concept Notes : Health Assessment II -...

NR228 / NR-228 Study Notes {Exam 1 / Exam 2 / Final Exam} : N...

NUR2407 / NUR 2407 Midterm / Final Exam Study Guide (Latest):...

.png)

MG6851 PRINCIPLES OF MANAGEMENT study notes ( BEST STUDY GUIDE...

Fundamentals of Nursing 21 Page Bundle - Nursing School Notes

.png)