Finance > QUESTIONS & ANSWERS > Business Finance NEW YORK UNIVERSITY STERN SCHOOL OF BUSINESS Debt Instruments and Markets Profess (All)

Business Finance NEW YORK UNIVERSITY STERN SCHOOL OF BUSINESS Debt Instruments and Markets Professor Carpenter Problem Set 4: No Arbitrage Pricing and Risk-Neutral... Share Question

Document Content and Description Below

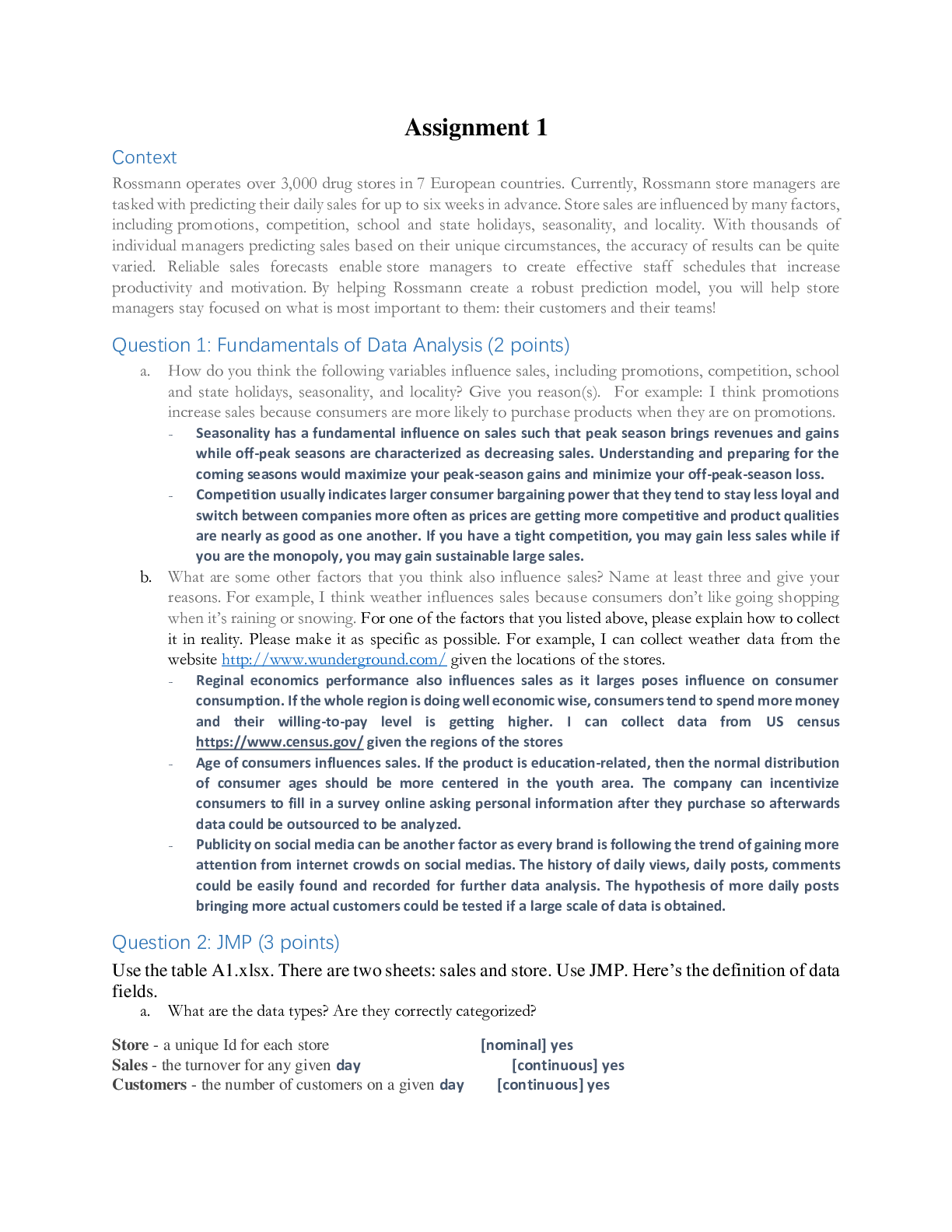

1 NEW YORK UNIVERSITY STERN SCHOOL OF BUSINESS Debt Instruments and Markets Professor Carpenter Problem Set 4: No Arbitrage Pricing and Risk-Neutral Probabilities 1) At time 0.5, the price of $1 ... par of a zero maturing at time 1 will be either $0.96 or $0.98. The current price of the zero maturing at time 1 is $0.94 and the current price of the zero maturing at time 0.5 is $0.97. Consider also a claim that pays off $1 at time 0.5 if the zero maturing at time 1 is worth $0.96, and 0 otherwise. This information is summarized in the payoff diagrams below. Time 0 Time 0.5 1 0.96 Zero maturing at time 0.5 0.97 1 Zero maturing at time 1 0.94 Claim ? 1 0.98 0 a) Determine a portfolio of the 0.5- and 1-year zeroes that has the same payoff as the claim at time 0.5. b) What is the value of the claim today in the absence of arbitrage? c) What are the risk-neutral probabilities of the two possible time 0.5 values of the zero maturing at time 1?2 2) At time 0.5, the price of $1 par of a zero maturing at time 1 will be either $0.96 or $0.98. The risk-neutral probability of the each outcome is 50%. The current price of $1 par of a zero maturing at time 0.5 is 0.97. Time 0 Time 0.5 1 Zero maturing at time 0.5 0.97 0.96 Zero maturing at time 1 ? 1 0.98 a) What is the price at time 0 of the zero maturing at time 1 in the absence of arbitrage? b) Multiple choice question. Pick one answer. Question: Which of the two zeroes above has the higher true expected return from time 0 to time 0.5? Answer 1: The 0.5-year zero. Answer 2: The 1-year zero. Answer 3: They have the same true expected return. Answer 4: There is not enough information provided to tell. 3) At time 0.5, the price of $1 par of a zero maturing at time 1 will be either $0.97 or $0.99. Consider two other assets. Asset #1 pays off $1 at time 0.5 if the price of the zero maturing at time 1 is $0.97 and pays off 0, otherwise. Asset #2 pays off $1 at time 0.5 if the price of the zero maturing at time 1 is $0.99 and pays off 0, otherwise. The prices today of Assets #1 and #2 are both $0.49. This information is summarized below. Time 0 Time 0.5 0.97 1 Zero maturing at time 1 ? 0 Asset #1 0.49 Asset #2 0.49 0.99 01 a) What is the price today of the zero maturing at time 1 in the absence of arbitrage? b) What is the price today of the zero maturing at time 0.5 in the absence of arbitrage?3 4) At time 0, the zero maturing at time 0.5 has a price of 0.97 per $1 par, and the zero maturing at time 1 has a price of 0.9409 per $1 par. At time 0.5, there will be one of two possible states: in the “up” state, the price of $1 par of a zero maturing at time 1 will be $0.96; in the “down” state, the price of this zero will be $0.98. The risk-neutral probability of the each outcome is 50%. This information is summarized below: Time 0 Time 0.5 1 0.96 Zero maturing at time 0.5 0.97 Zero maturing at time 1 0.9409 1 0.98 Consider a 0.5-year floating rate note with rate set in arrears. This note has a single payoff at time 0.5 equal to par plus a coupon based on the 0.5-year rate observed at time 0.5. In terms of the notation from class, for each $1 par, the cash flow at time 0.5 is 1+0.5r1/2. a) What is the payoff of $100,000 par of this note at time 0.5, in the up state? b) What is the payoff of $100,000 par of this note at time 0.5, in the down state? c) Use the risk-neutral probabilities to compute the value of this note at time 0. d) Write down, but do not solve, equations that determine the par amounts N0.5 and N1 of the zeroes maturing at time 0.5 and time 1 to hold in a portfolio that replicates the time 0.5 payoff of the rate-set-in-arrears floater. [Show More]

Last updated: 2 years ago

Preview 1 out of 4 pages

.png)

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

Reviews( 0 )

$7.00

Can't find what you want? Try our AI powered Search

Document information

Connected school, study & course

About the document

Uploaded On

Apr 22, 2021

Number of pages

4

Written in

Additional information

This document has been written for:

Uploaded

Apr 22, 2021

Downloads

0

Views

60

.png)

.png)