Critical Thinking > QUESTIONS & ANSWERS > CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION: answers (All)

CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION: answers

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 44 pages

Instant download

.png)

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jun 25, 2021

Number of pages

44

Written in

All

Additional information

This document has been written for:

Uploaded

Jun 25, 2021

Downloads

0

Views

131

Document Keyword Tags

Recommended For You

Get more on QUESTIONS & ANSWERS »

Test Bank For Essential Cosmic Perspective, The, 9th Edition b...

Test Bank Chapter 11 Depreciation, Impairments, and Depletion.

Test Bank Chapter 11 Depreciation, Impairments, and Depletion.

COMS 101 Quiz chapter 11 Test Bank Complete Answers, Latest Gu...

COMS 101 Quiz chapter 11 (set 3) Liberty University Complete A...

![Preview of [SOLVED] HIEU 201 / HIEU201 Chapter 11 Quiz (LATEST 2022)](https://scholarfriends.com/storage/HIEU_201_Chapter_11_Quiz.png)

[SOLVED] HIEU 201 / HIEU201 Chapter 11 Quiz (LATEST 2022)

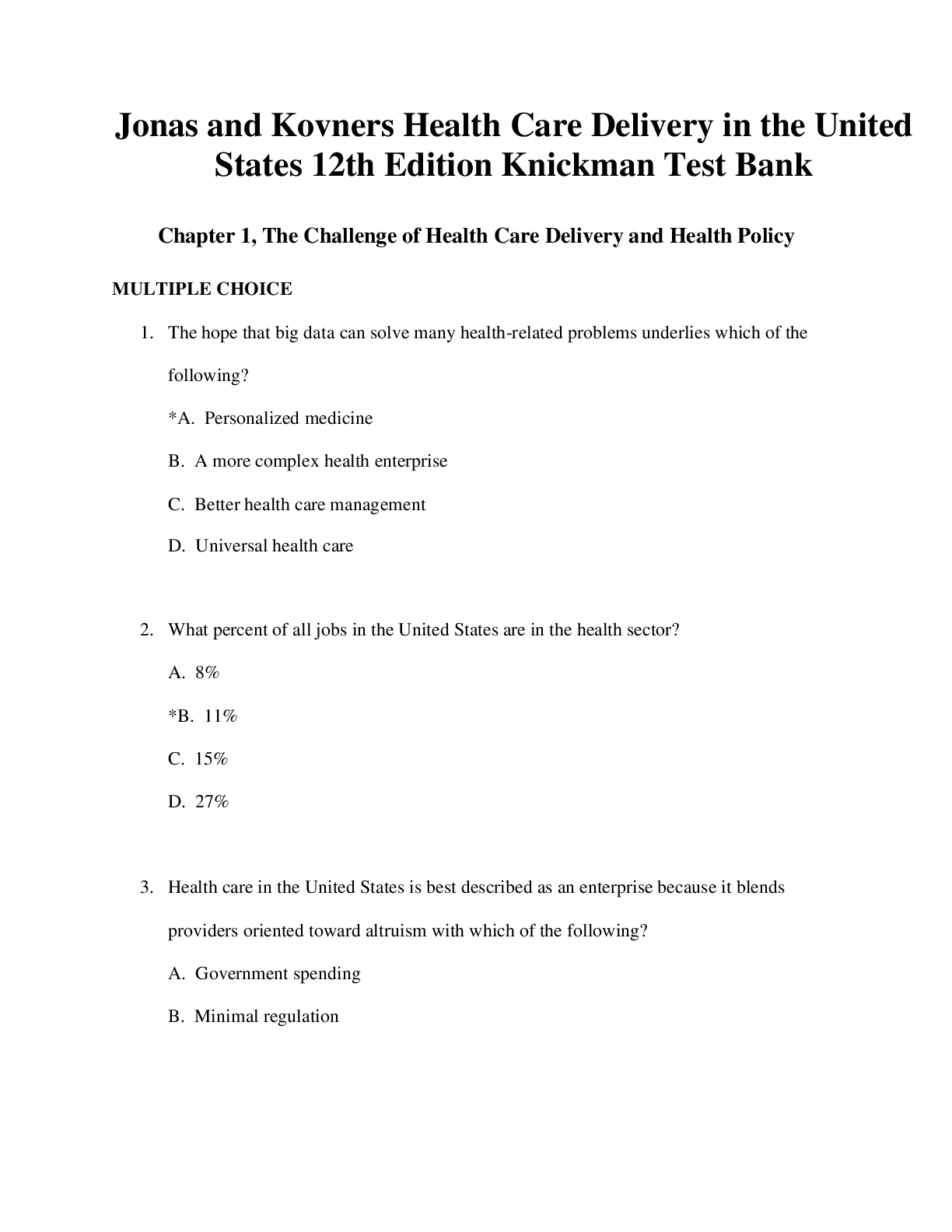

Test Bank for Jonas and Kovners Health Care Delivery in the Un...

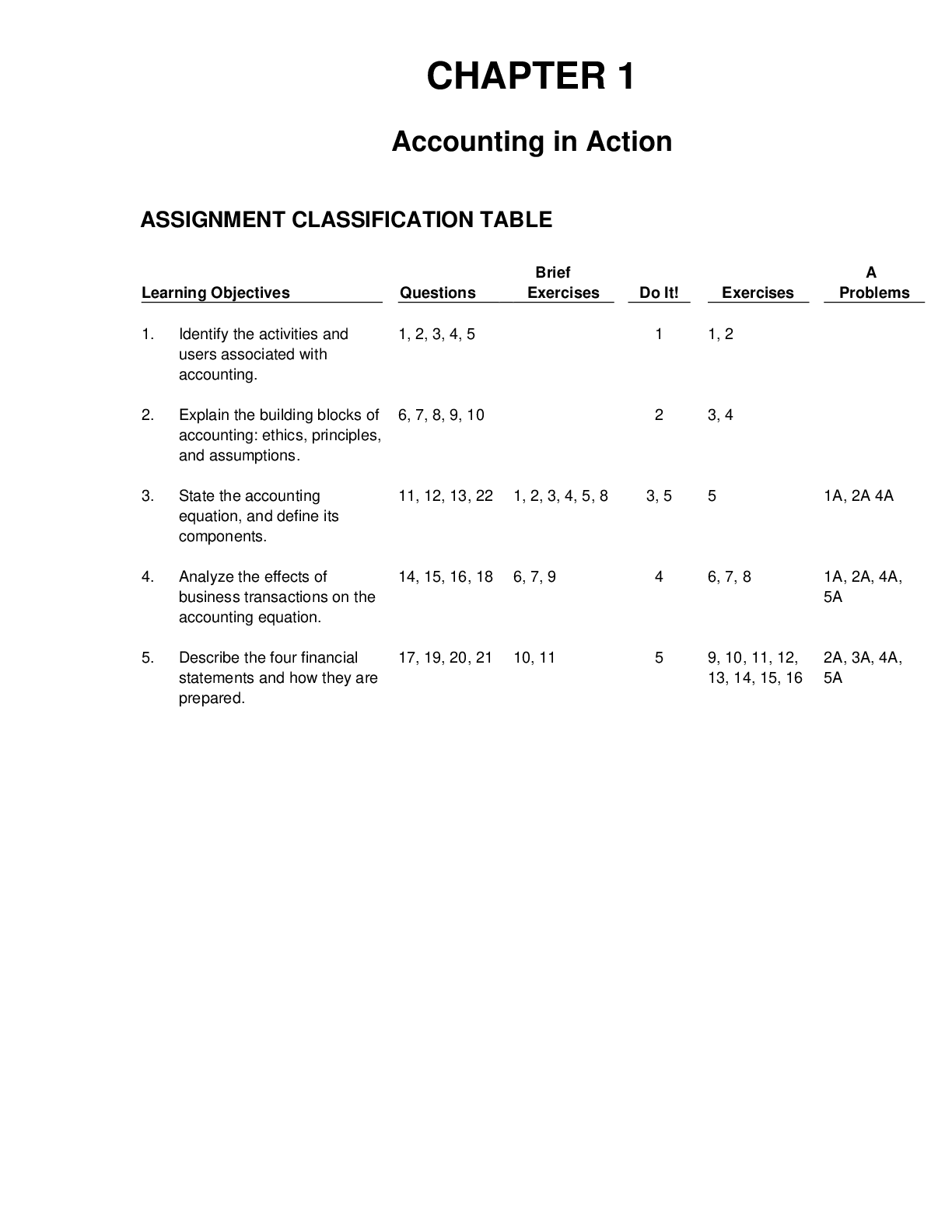

Principles of Financial Accounting (chapter 1-18) 12e Jerry We...

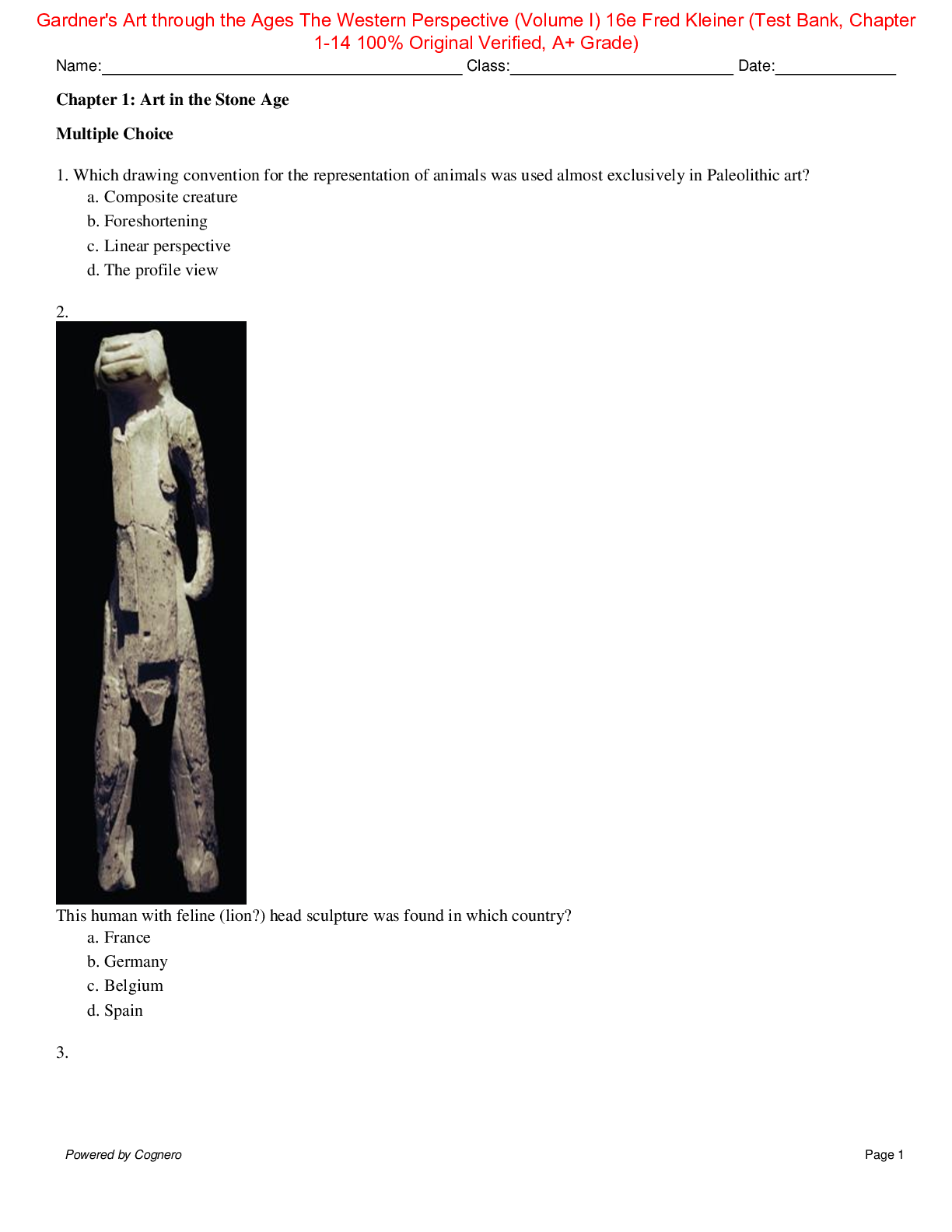

Test Bank for Gardner's Art through the Ages The Western Persp...

Practice Chapter 11 - Economic Growth and the Wealth of Nation...

.png)

Massachusetts Institute of Technology - 21F. 551Chapter-11-Wor...

.png)

WGU C201 Business Acumen Chapter 11, 12, 13: Marketing Already...

.png)

The Lipid Bilayer CHAPTER 11 MEMBRANE STRUCTURE University of...

BIOS 225 Chapter 11 Questions and Answers (Verified Answers...

BIOS 135 Chapter 11 Questions and Answers (Verified Answers)

.png)