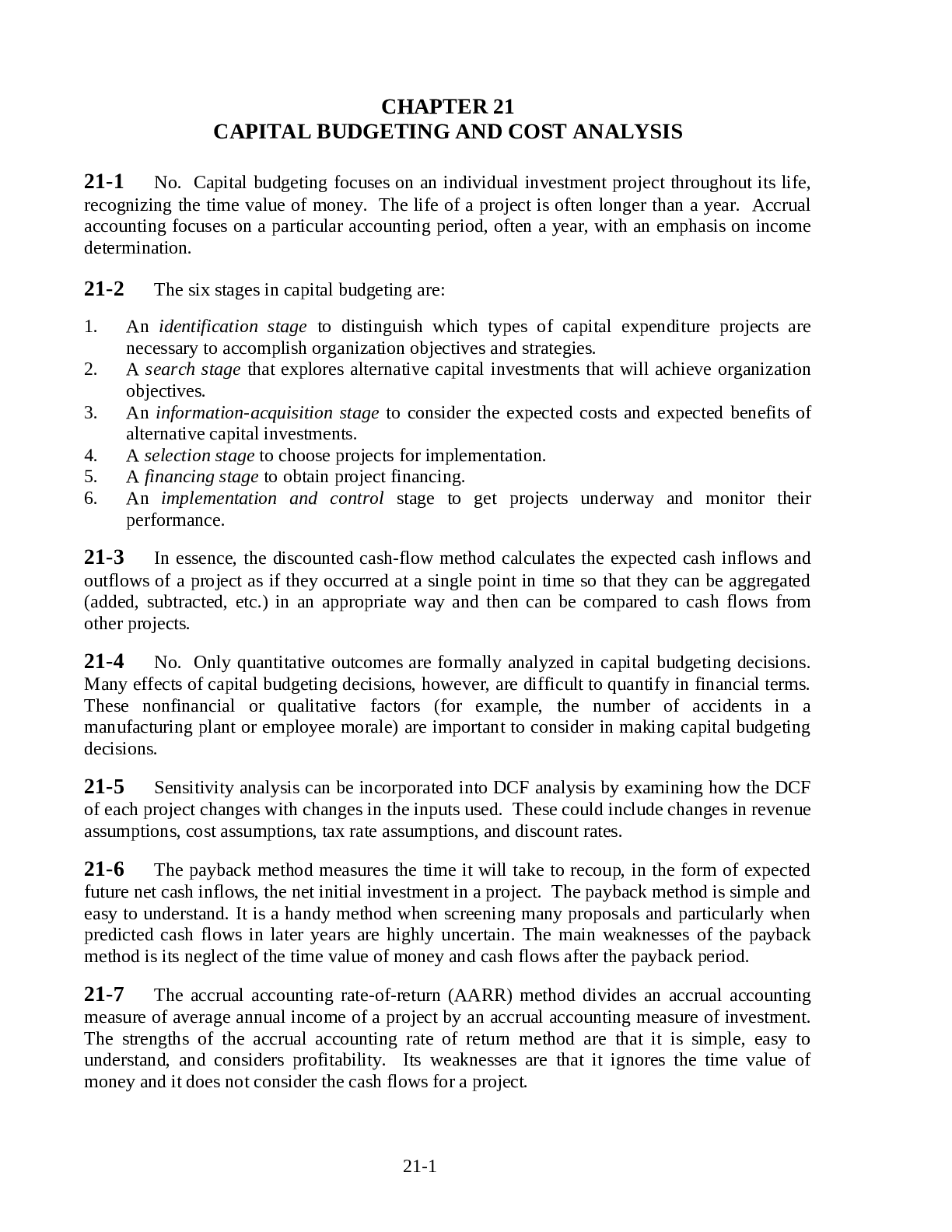

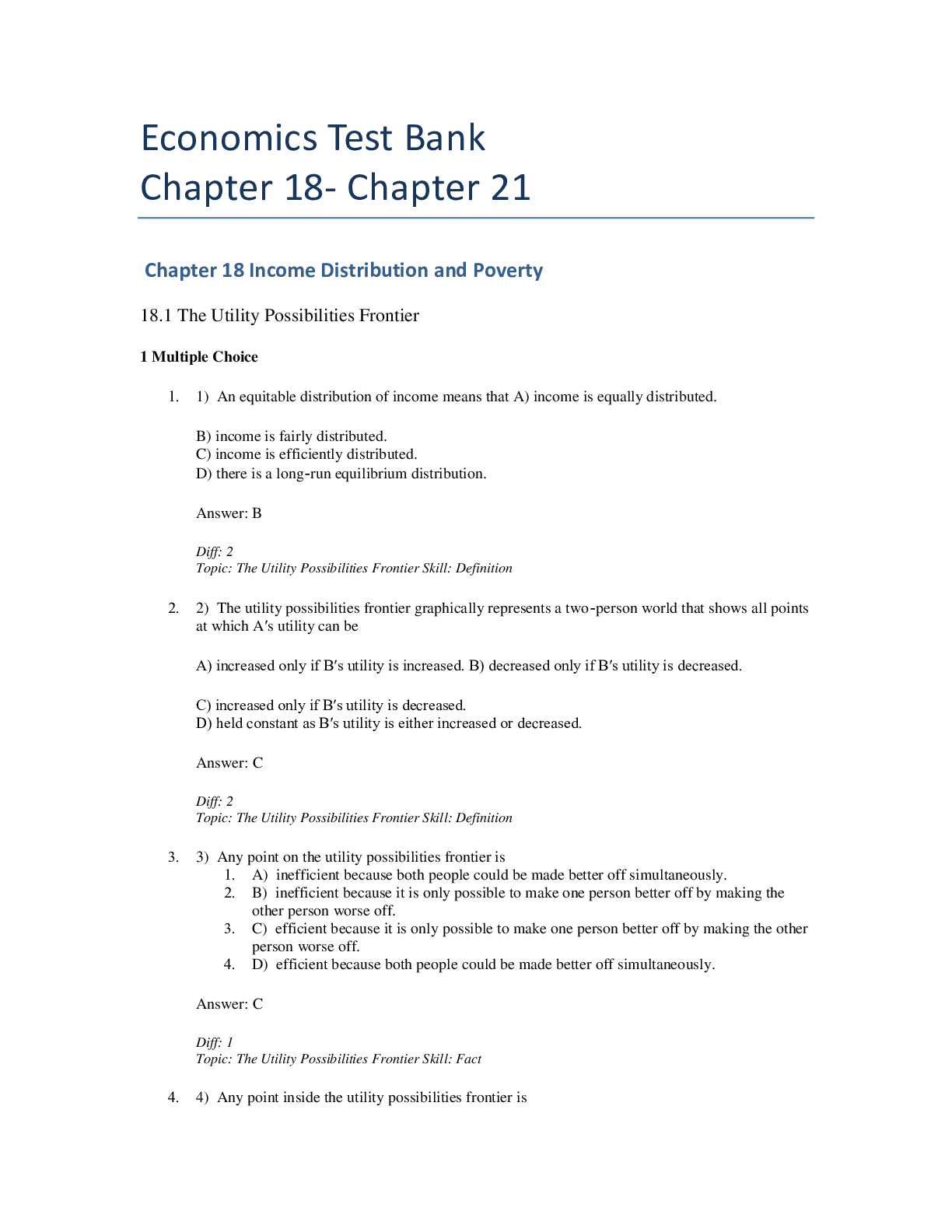

Financial Accounting > SOLUTIONS MANUAL > CHAPTER 21 CAPITAL BUDGETING AND COST ANALYSIS: ANSWERS. (All)

CHAPTER 21 CAPITAL BUDGETING AND COST ANALYSIS: ANSWERS.

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 49 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jun 25, 2021

Number of pages

49

Written in

All

Additional information

This document has been written for:

Uploaded

Jun 25, 2021

Downloads

0

Views

93

Document Keyword Tags

Recommended For You

Get more on SOLUTIONS MANUAL »

Solution Manual For Operations & Supply Chain Management 8th C...

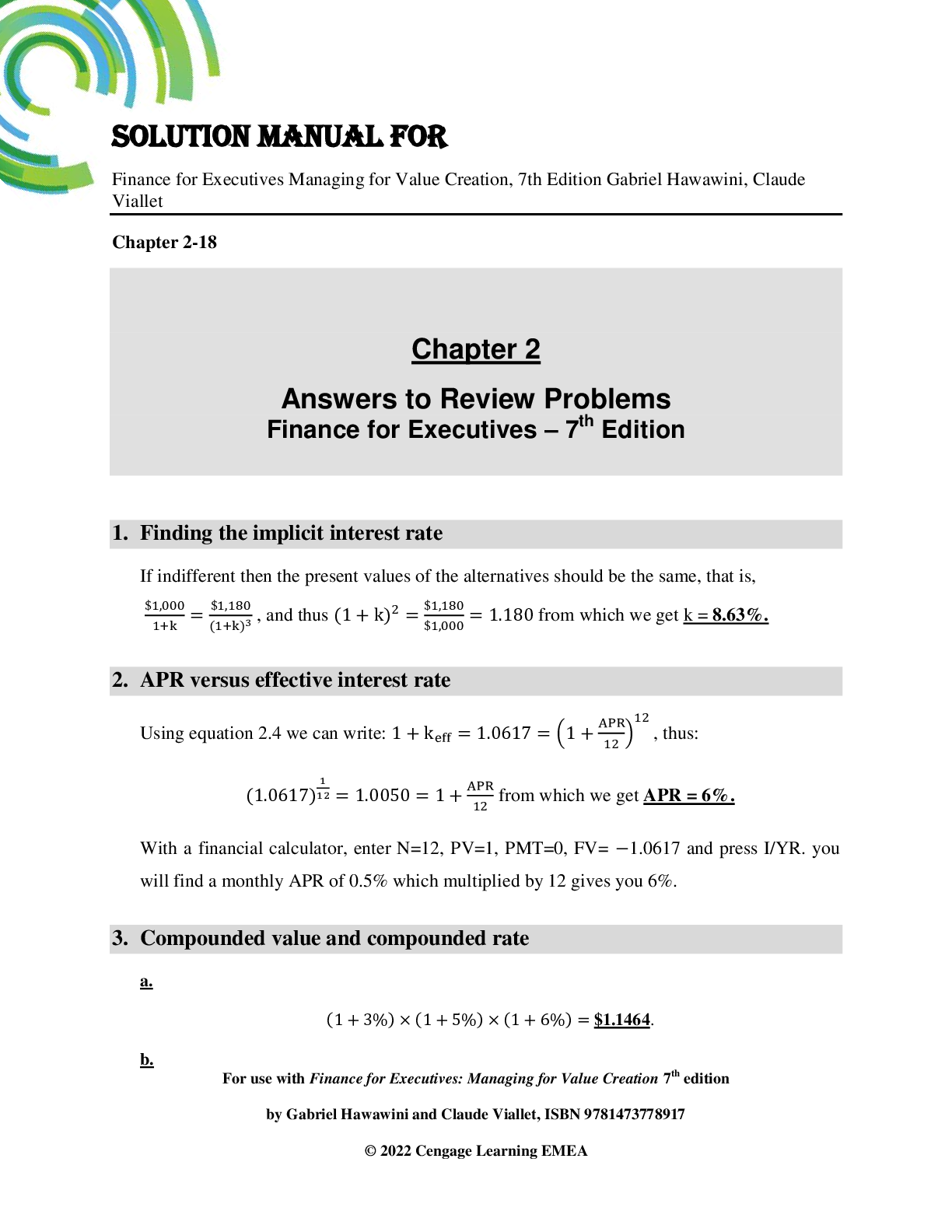

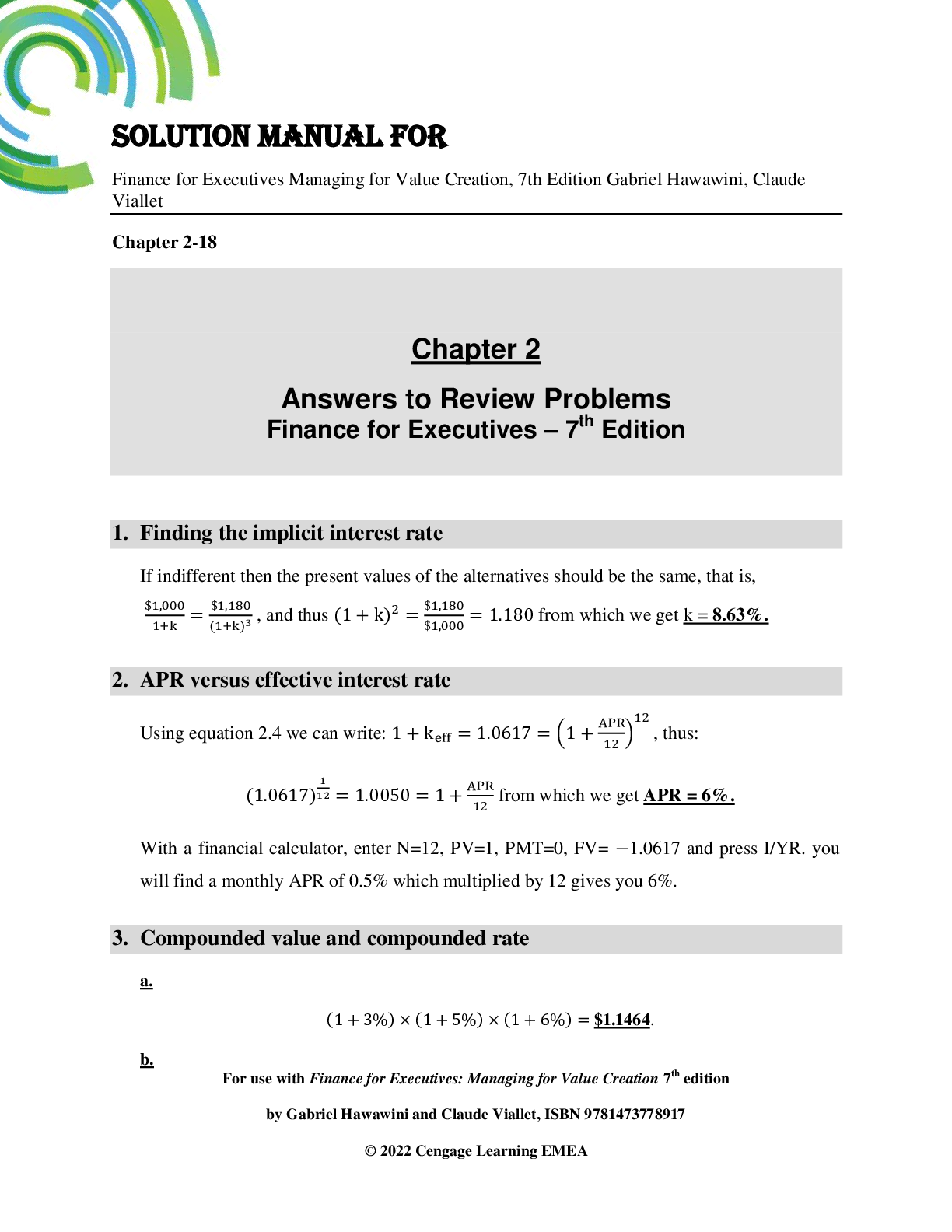

Solutions Manual for Finance for Executives Managing for Value...

Solution Manual For Finance for Executives Managing for Value...

SOLUTIONS MANUAL Fault-Tolerant Systems 2nd Edition by Israel...

TEST BANK Chapter 21: Peripheral Vascular System and Lymphatic...

.png)

TEST BANK Chapter 21: Peripheral Vascular System and Lymphatic...

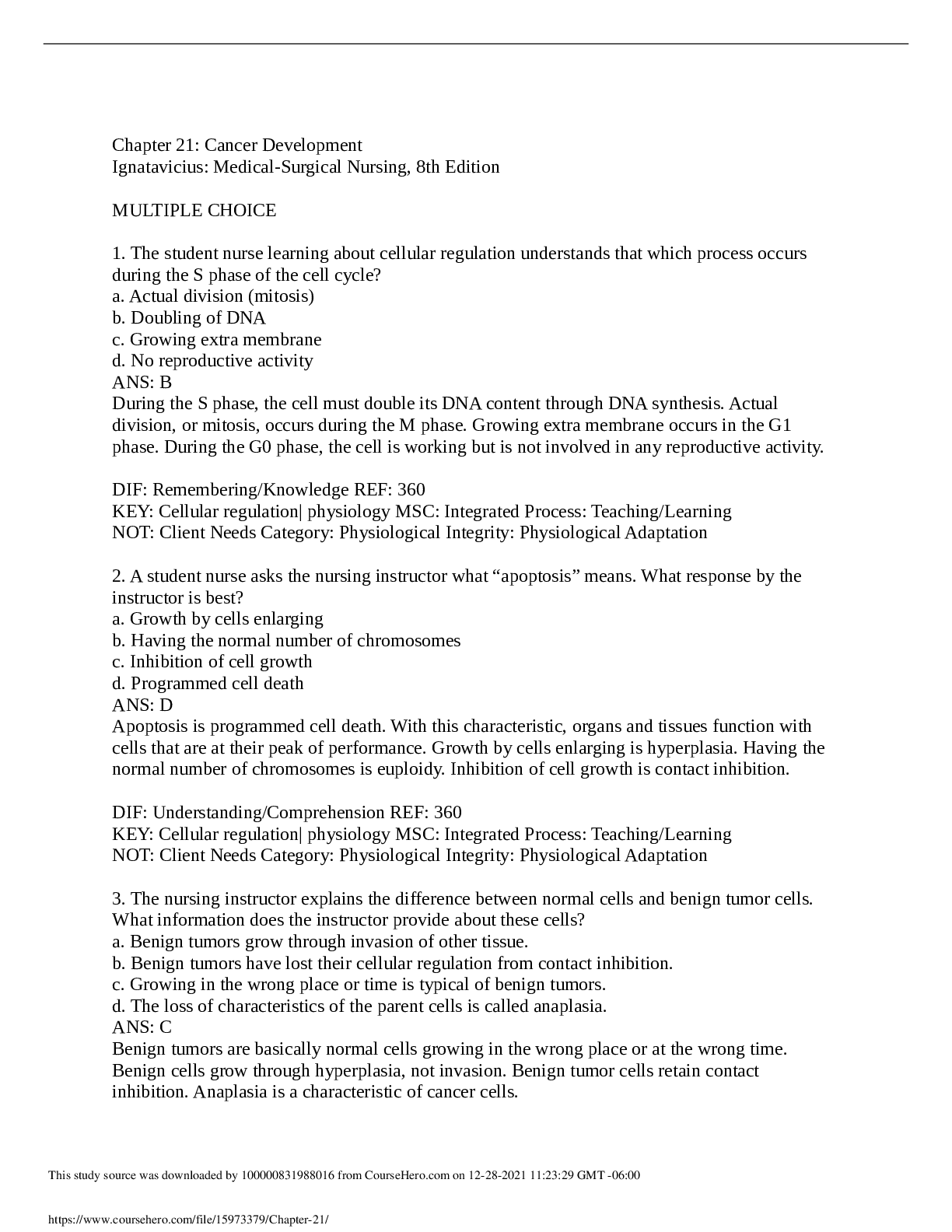

Milestone Chapter 21: Cancer Development (Concepts for Interpr...

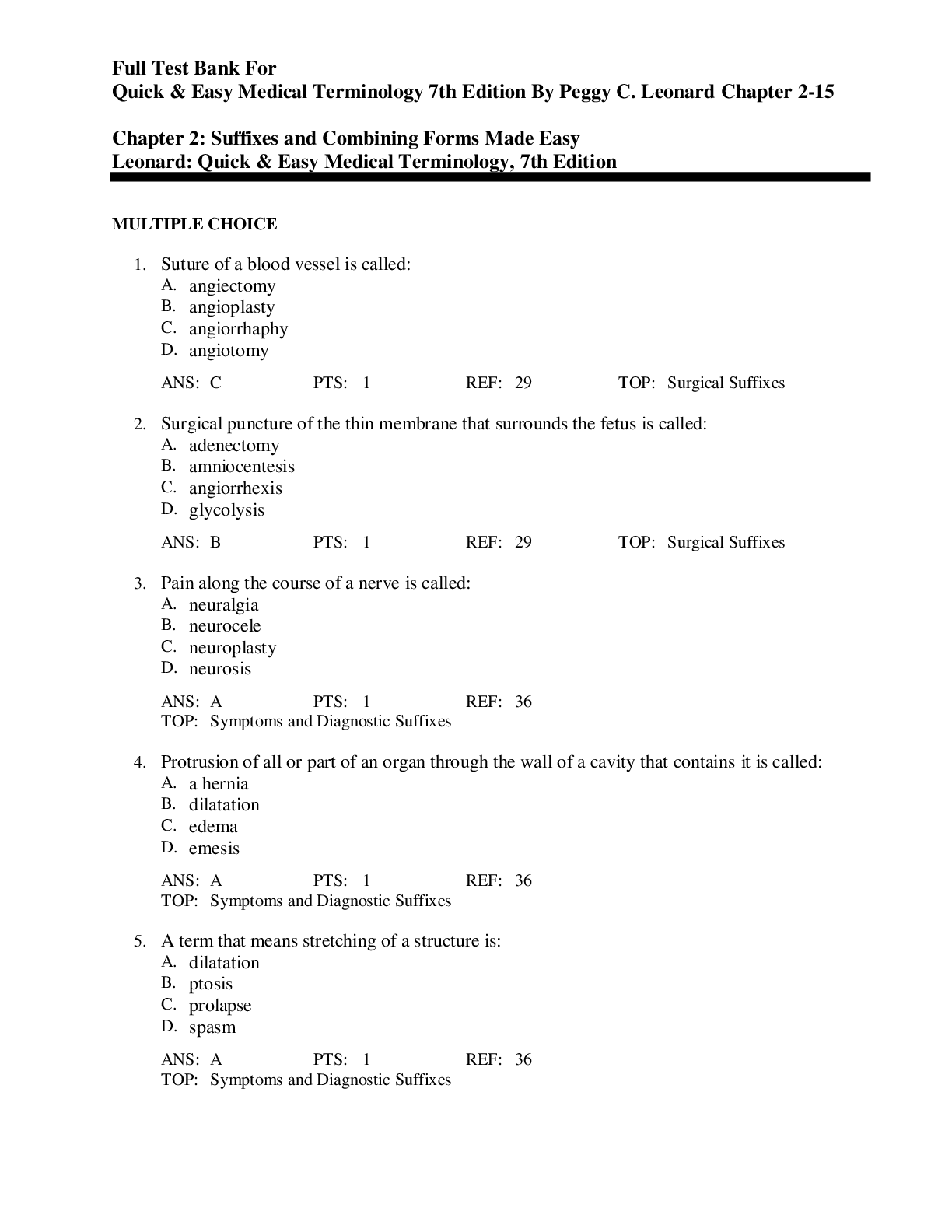

Full Test Bank For Quick & Easy Medical Terminology 7th Editio...

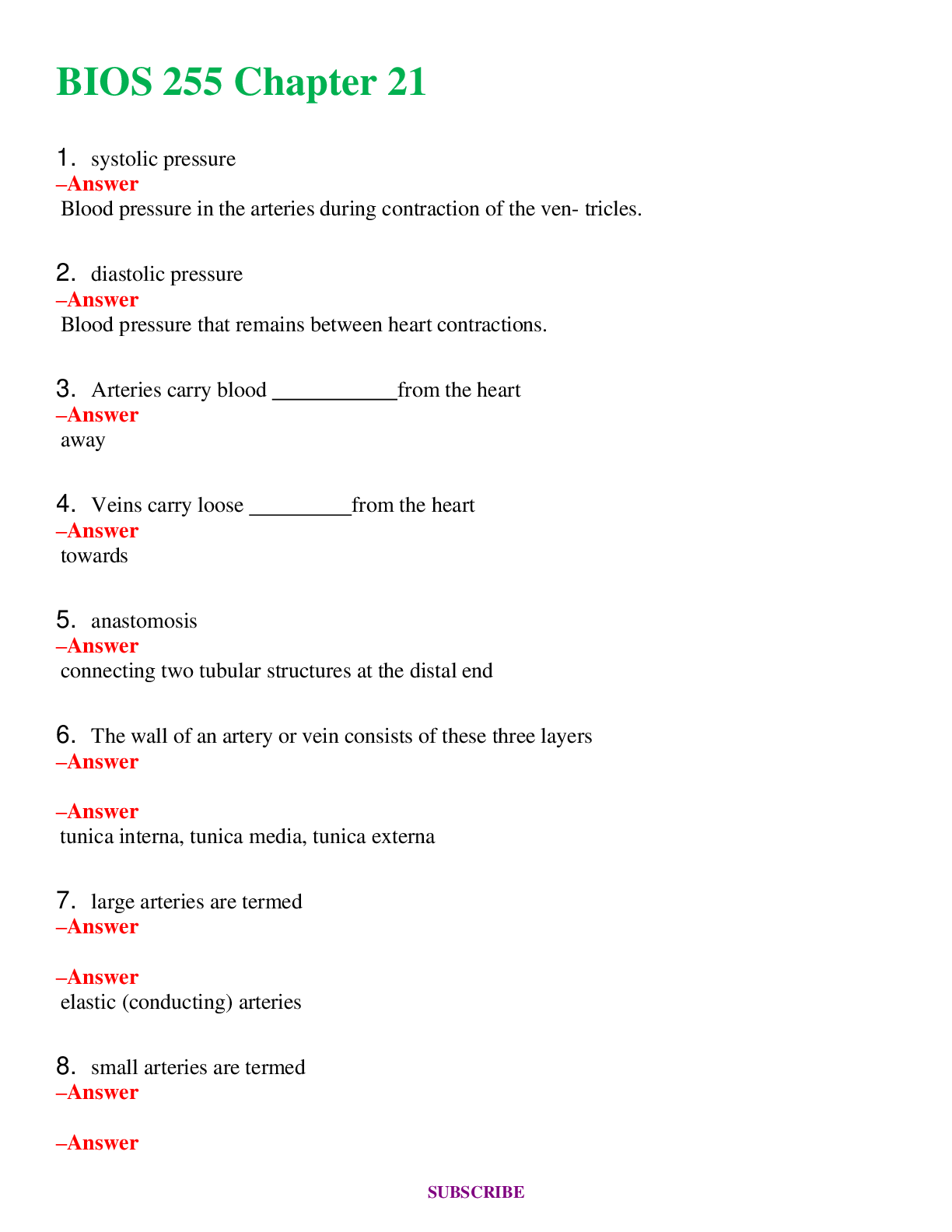

BIOS 255 Chapter 21 Questions and Answers (Verified Answers...

.png)

Print Chapter 21 The Immune System Innate and Adaptive Exam Bo...

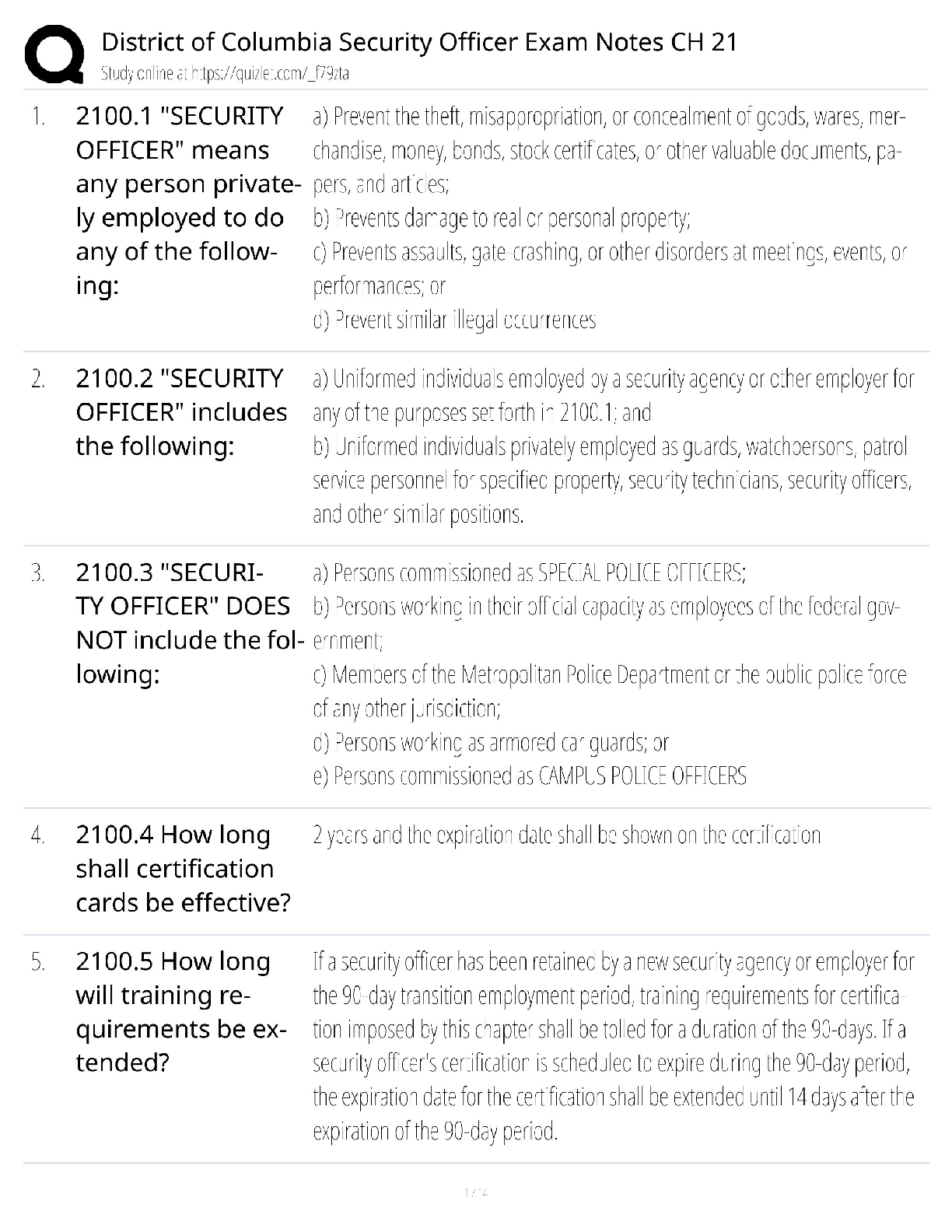

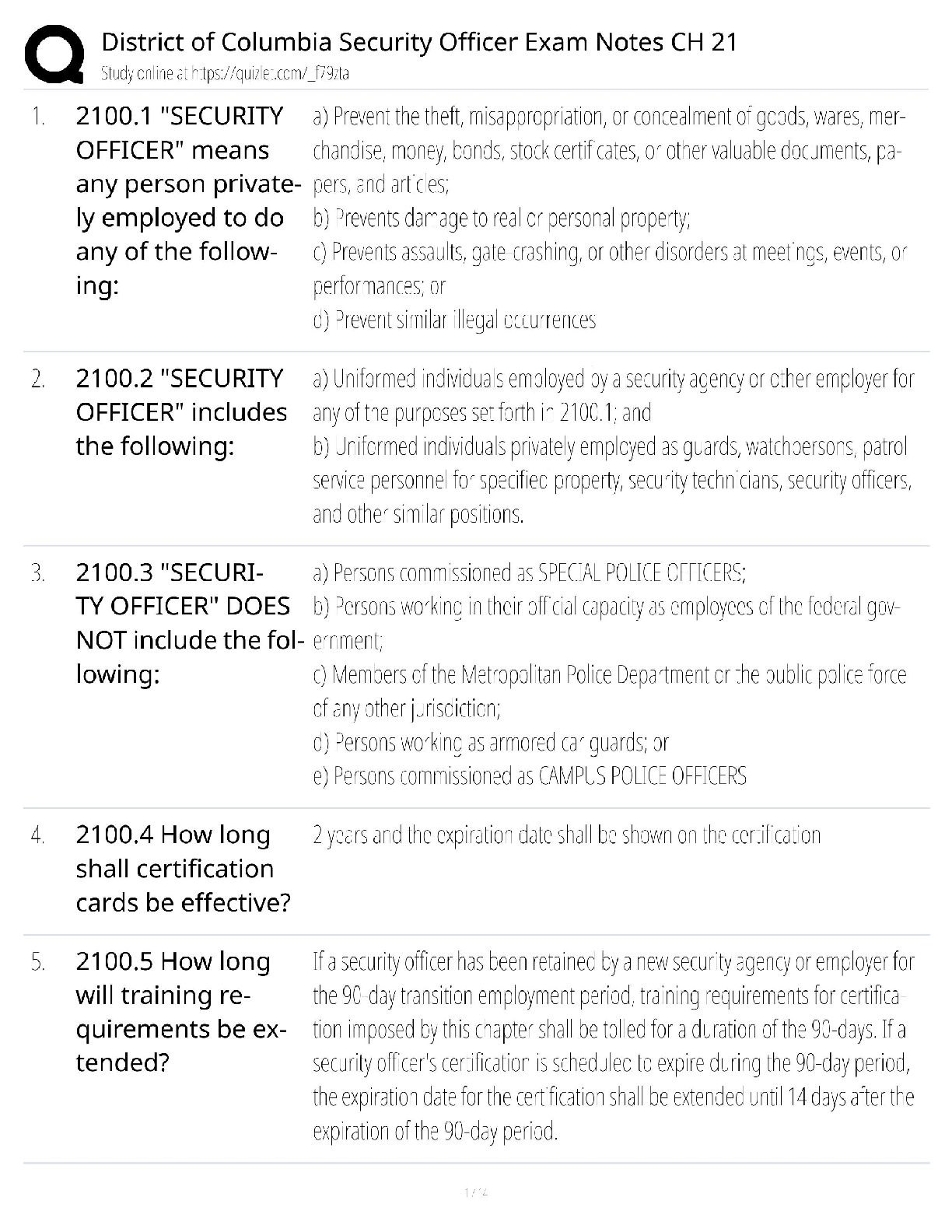

District of Columbia Security Officer Exam Notes Chapter 21...

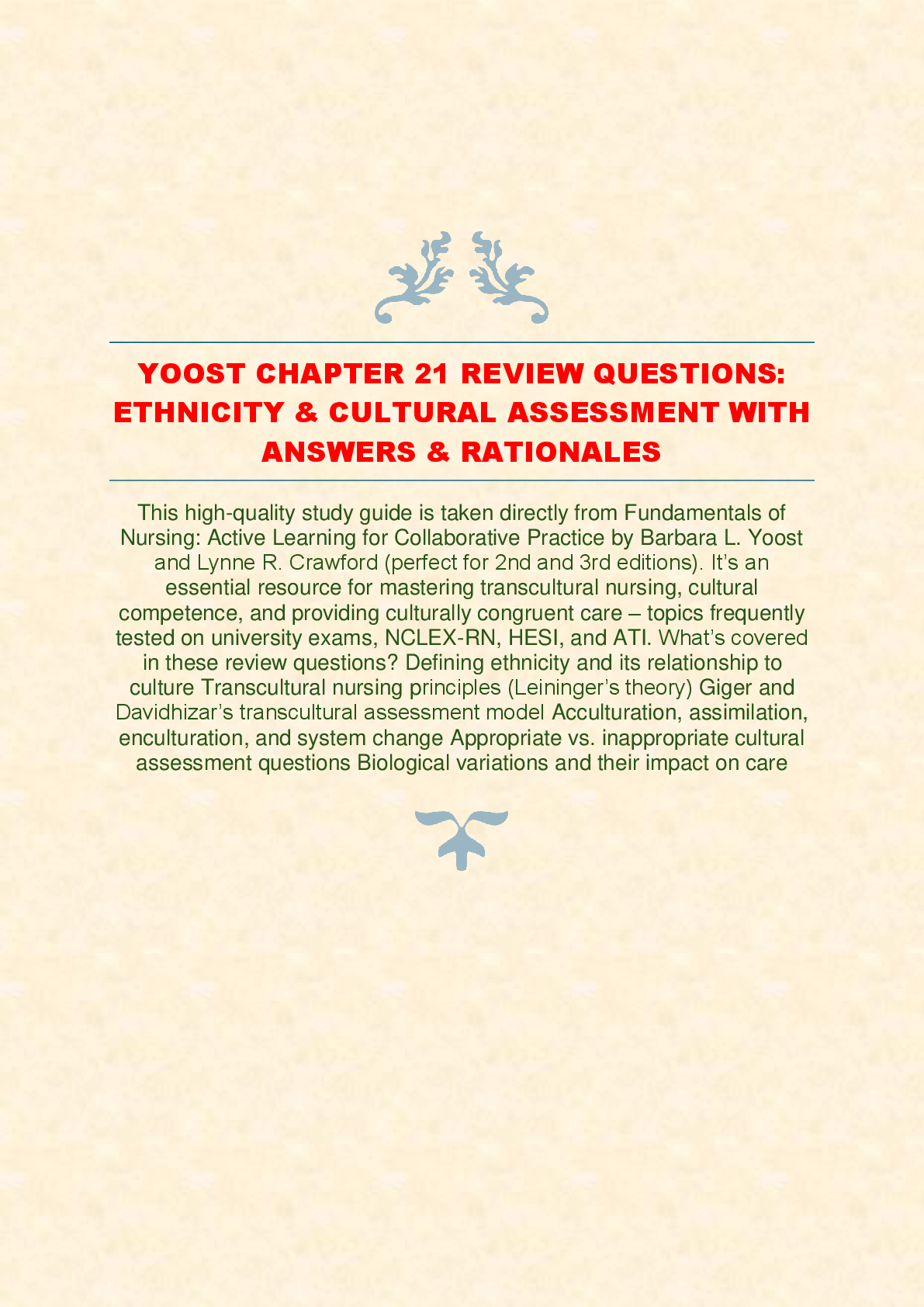

YOOST CHAPTER 21 REVIEW QUESTIONS: ETHNICITY & CULTURAL ASSES...

NURS 6501 / NURS6501: Advanced Pathophysiology - Chapter 21 St...

NR566 / NR 566: Advanced Pharmacology for Care of the Family W...