Accounting > Solutions Guide > CHAPTER 22 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, AND MULTINATIONAL CONSIDERATIONS: ANSWERS (All)

CHAPTER 22 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, AND MULTINATIONAL CONSIDERATIONS: ANSWERS

Document Content and Description Below

Last updated: 10 months ago

Preview 1 out of 48 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jun 25, 2021

Number of pages

48

Written in

All

Additional information

This document has been written for:

Uploaded

Jun 25, 2021

Downloads

0

Views

213

Document Keyword Tags

Recommended For You

Get more on Solutions Guide »

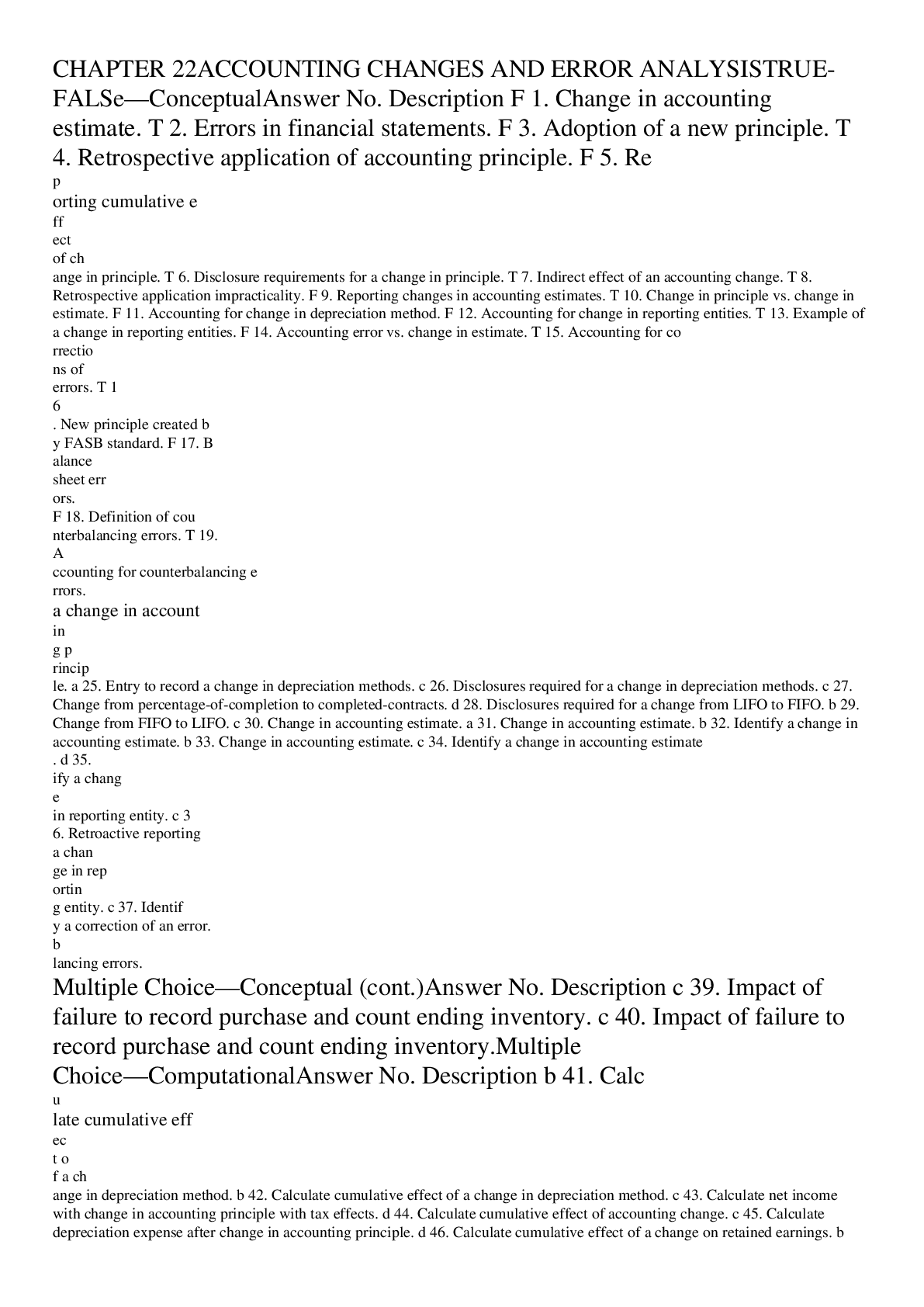

Test Bank CHAPTER 22 ACCOUNTING CHANGES AND ERROR ANALYSIS

Test Bank for Primary Care 6th Edition Buttaro Chapter 1 to C...

Primary Care 6th Edition Buttaro Test Bank Chapter 1 to Chapte...

Giger & Davidhizar: Transcultural Nursing: Assessment and Inte...

Obstetrician Chapter 22: Nursing Management of the Postpartum...

NR 304 Week 4 Musculoskeleton Review Questions with correct an...

HA Chapter 22 Actual Questions and Verified Answers ( Included...

NURS 6501 / NURS6501: Advanced Pathophysiology - Chapter 22 St...

NR566 / NR 566: Advanced Pharmacology for Care of the Family W...

.png)

Chapter 22_ Parenteral Medications _ Nursing School Test Banks...

NUR1021 1211c Chapter 22 real exam questions and answers solut...

Pharmacology Exam 4 Review: Chapter 20 Anxiolytics and Hypnoti...

NR 566 Week 6 Study Guide {2022} | Chapter 22: Drugs Affecting...