Financial Accounting > DISCUSSION POST > ACCT 525 - NMC Project Paper. 2021 (All)

ACCT 525 - NMC Project Paper. 2021

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 3 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Sep 12, 2021

Number of pages

3

Written in

All

Additional information

This document has been written for:

Uploaded

Sep 12, 2021

Downloads

0

Views

136

Document Keyword Tags

Recommended For You

Get more on DISCUSSION POST »

.png)

.png)

.png)

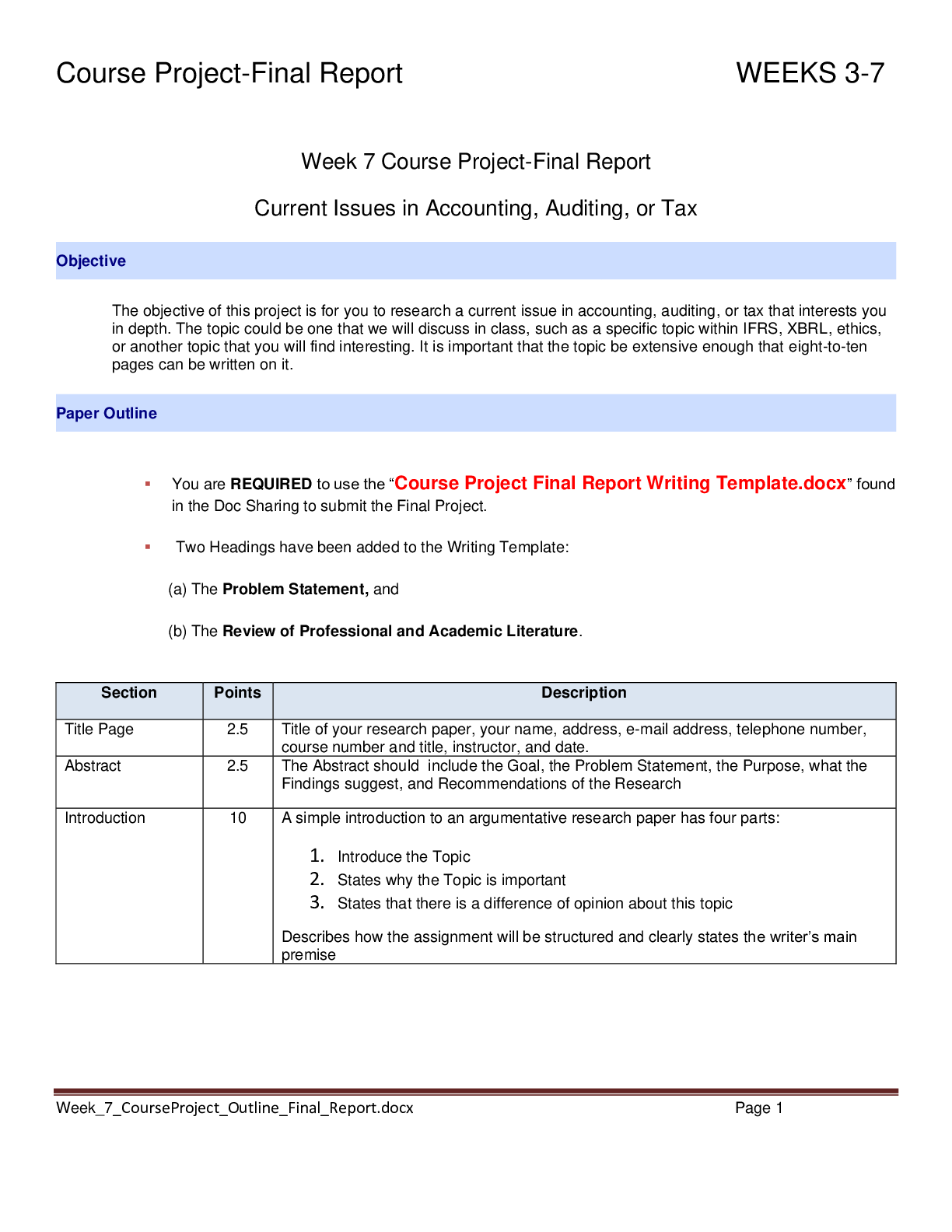

ACCT-525 Week 7 Course Project: FINAL REPORT ALL CORRECT RESEA...

ACCT 525 Current Issues In Accounting - ACCT 525 Week 7 Course...

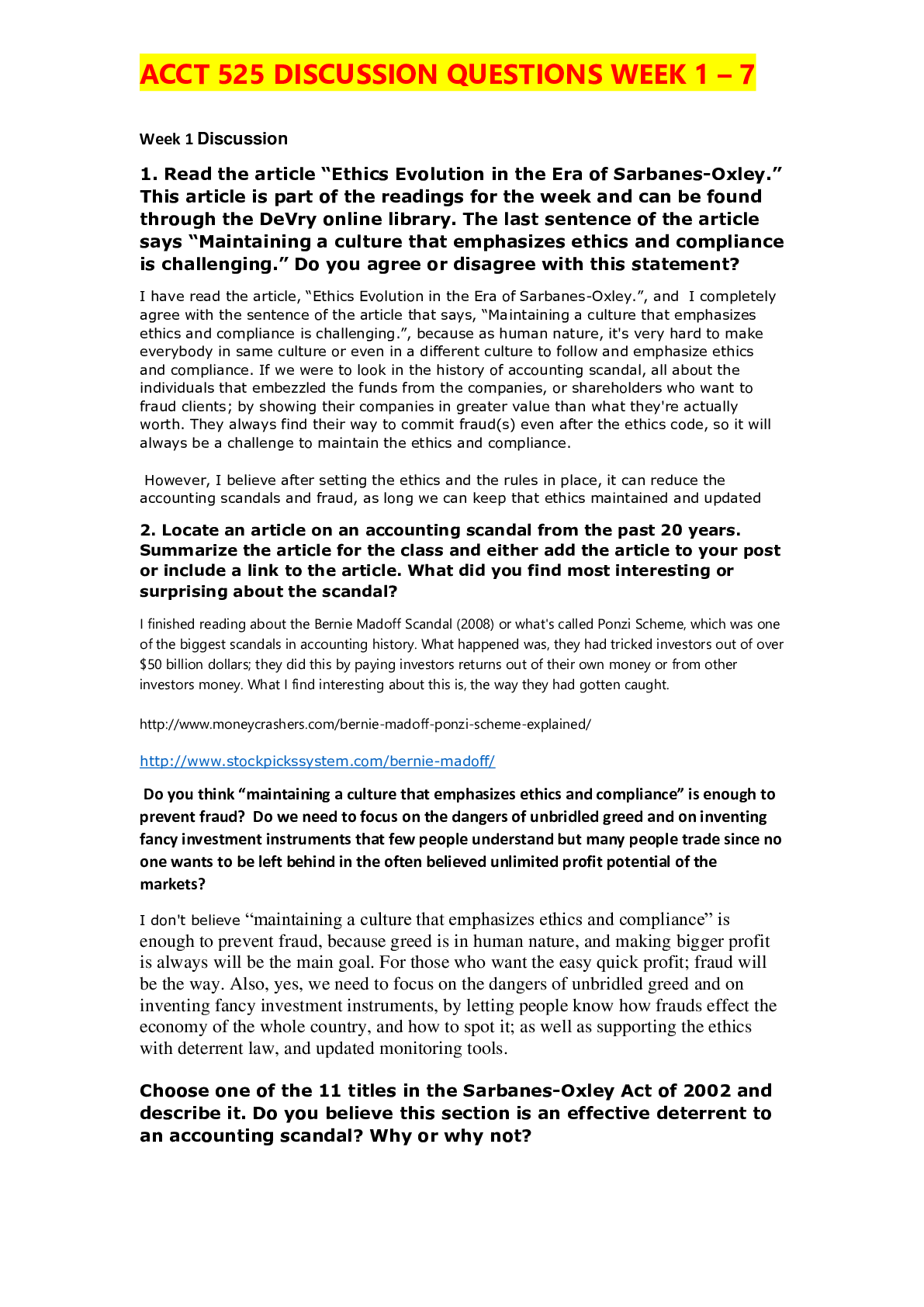

ACCT 525 Current Issues In Accounting - ACCT 525 DISCUSSION QU...

.png)

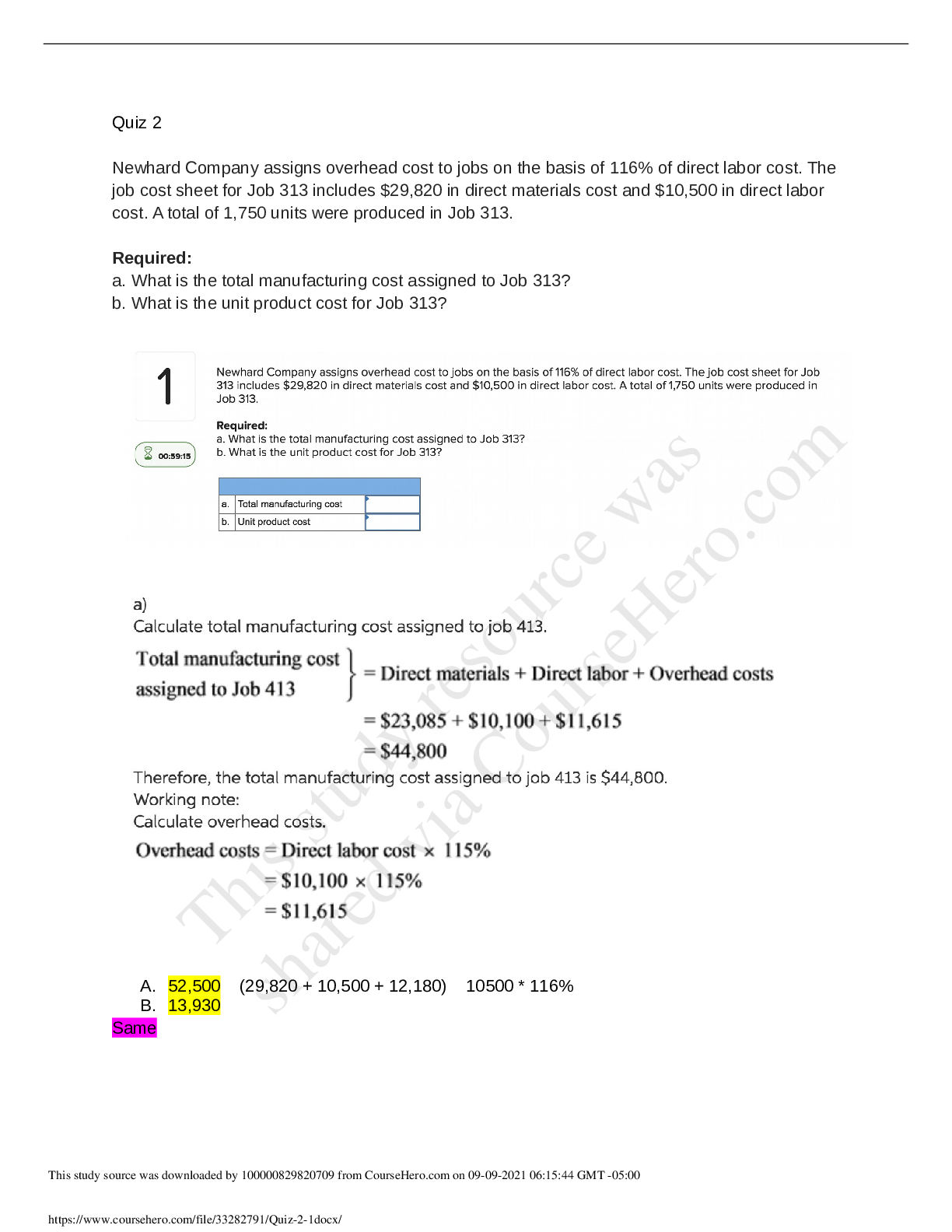

ACCT 525 Current Issues In Accounting - ACCT 525 Quiz 1 WITH U...

ACCT 525 Quiz 1 QUESTIONS AND ANSWERS WITH DETAILED EXPLANATIO...

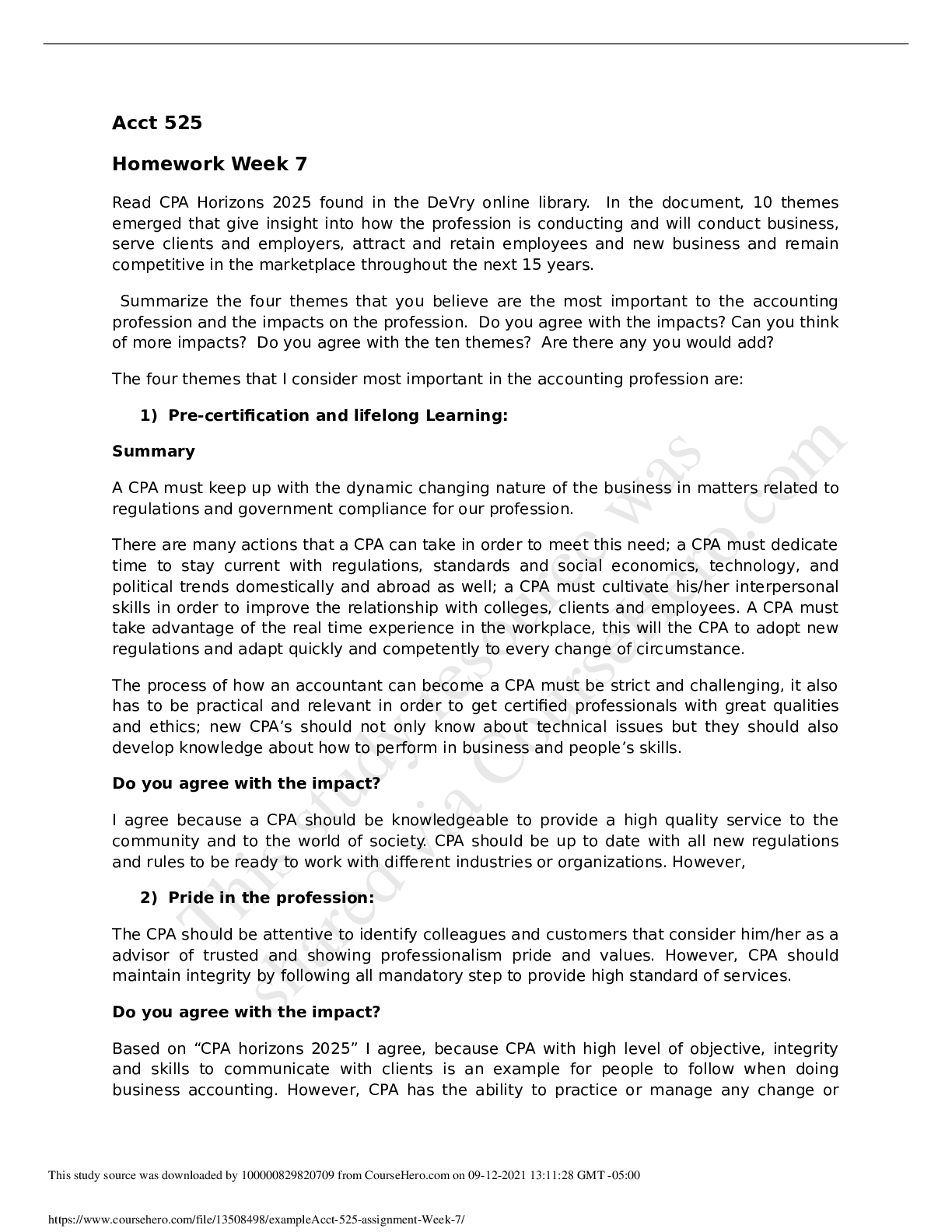

ACCT 525 Week 7 Homework Assignment ASSURED GRADE A SCORE WITH...

ACCT 525 Current Issues In Accounting - ACCT 525 Week 7 Homewo...

Financial Accounting with International Financial Reporting St...