Finance > QUESTIONS & ANSWERS > Holcomb Industries sold a piece of machinery with a purchase value of $918,000 and accumulated depre (All)

Holcomb Industries sold a piece of machinery with a purchase value of $918,000 and accumulated depreciation of $856,800 for $80,000. They realized a gain of $18,800 on the sale. How would this transaction affect overall cash flows? OVERVIEW OF THE FINANCIAL STATEMENTS

Document Content and Description Below

Last updated: 5 months ago

Preview 1 out of 61 pages

Instant download

Loading document previews ...

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jul 21, 2022

Number of pages

61

Written in

All

Additional information

This document has been written for:

Uploaded

Jul 21, 2022

Downloads

0

Views

137

Document Keyword Tags

Recommended For You

Get more on QUESTIONS & ANSWERS »

Financial Management for Public, Health, and Not-for-Profit Or...

.png)

Fundamentals of Corporate Finance, 5e Robert Parrino, David K...

.png)

Financial Management for Public, Health, and Not-for-Profit Or...

![Preview of Foundations of Finance, 10th Edition, By Arthur Keown, John Petty | [eBook] [PDF]](https://scholarfriends.com/storage/[PDF] [eBook] for Foundations of Finance, 10th Edition, By Arthur Keown, John Martin, J.png)

Foundations of Finance, 10th Edition, By Arthur Keown, John Pe...

.png)

Fundamentals of Corporate Finance, 5e Robert Parrino, David K...

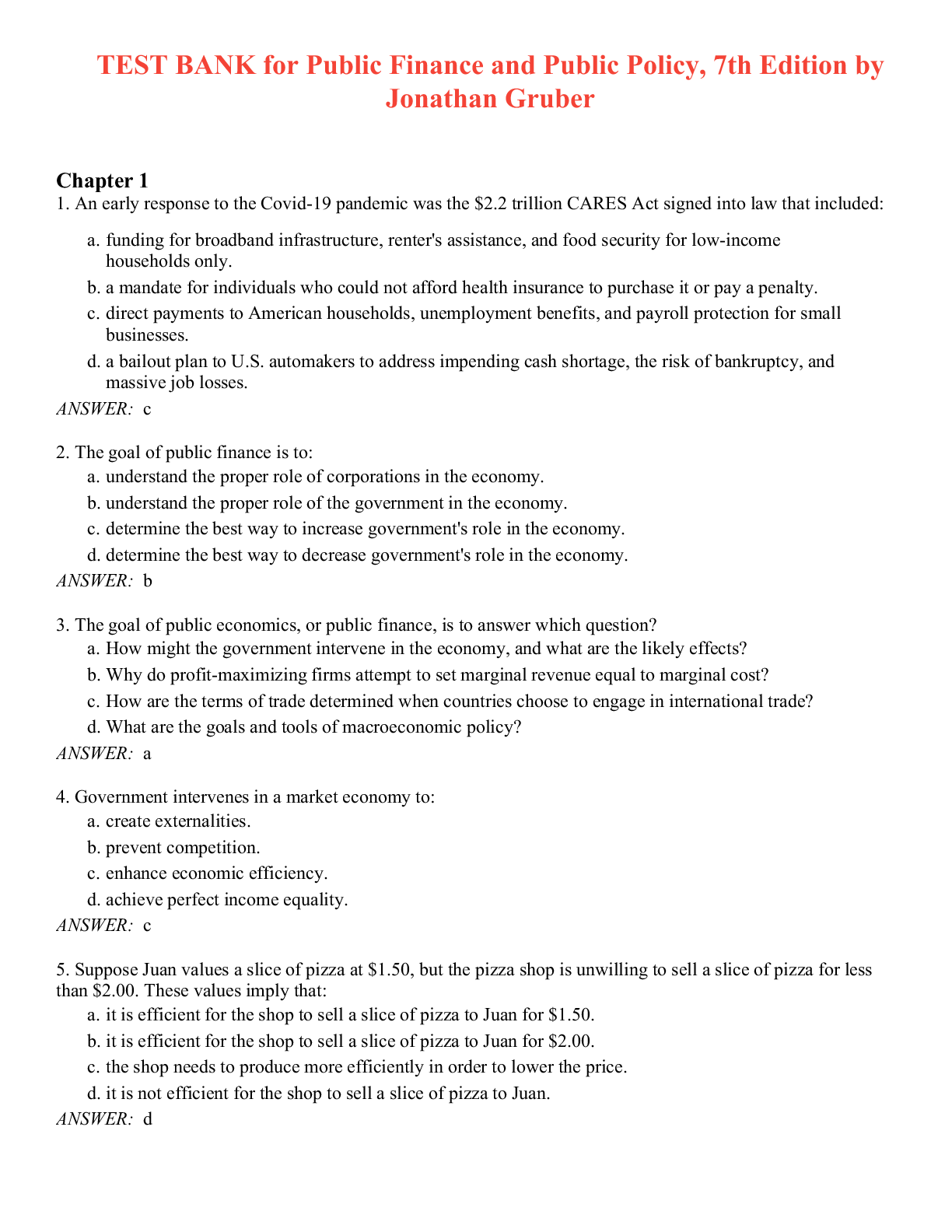

TEST BANK for Public Finance and Public Policy, 7th Edition by...

Finance Applications & Theory, 6e Marcia Cornett, Troy Adair,...

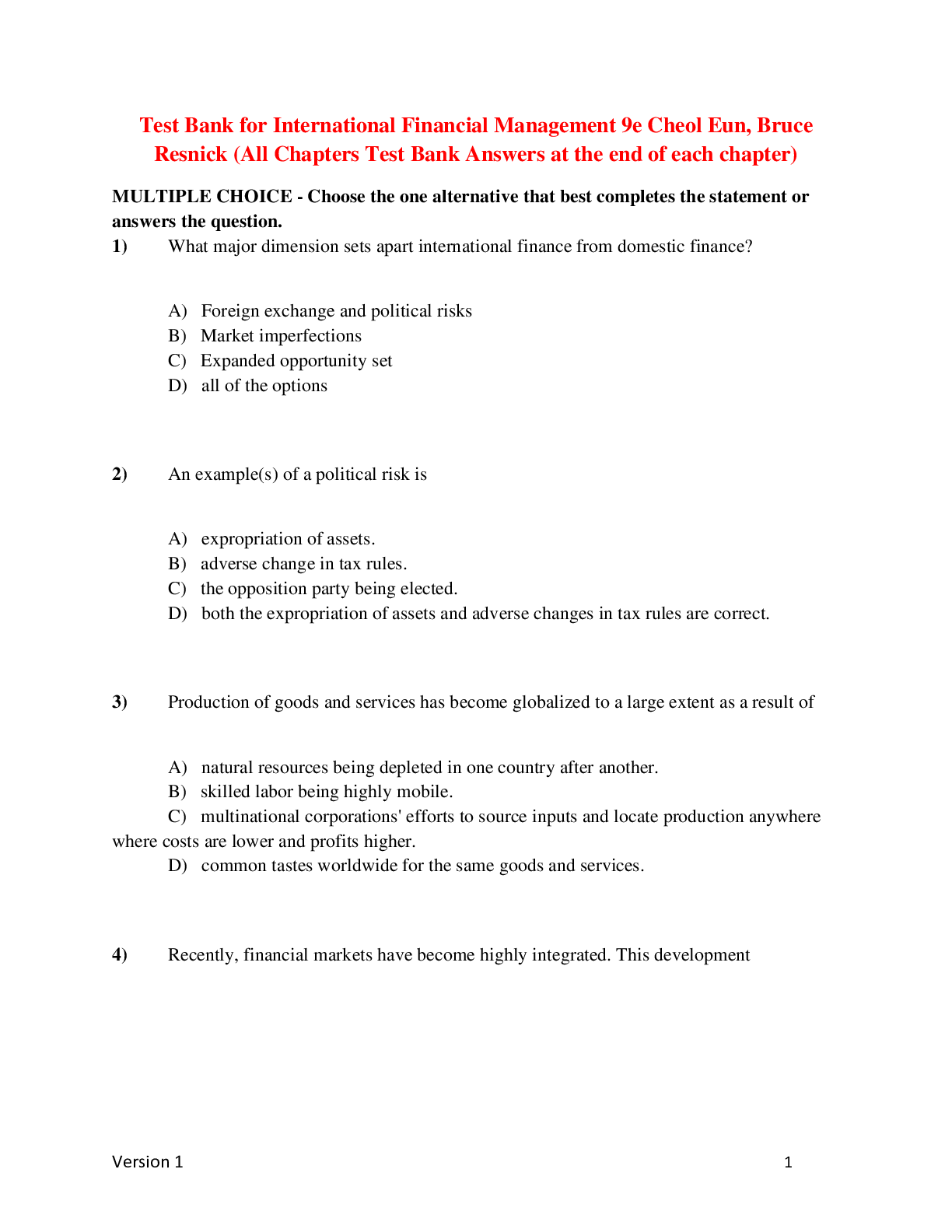

International Financial Management 9e Cheol Eun, Bruce Resnick...

International Financial Management 9e Cheol Eun, Bruce Resnick...

An Introduction to Derivative Securities, Financial Markets, a...

.png)

Introduction to Finance Markets, Investments, and Financial Ma...

![Preview of Corporate Financial Management, 6th Edition, By Glen Arnold, Deborah Lewis [PDF] [eBook]](https://scholarfriends.com/storage/[PDF] [eBook] for Corporate Financial Management, 6th Edition, By Glen Arnold, Deborah Lewis.png)

Corporate Financial Management, 6th Edition, By Glen Arnold, D...

![Preview of eBook [PDF] Corporate Finance The Core, 5th Edition By Jonathan Berk, Peter Demarzo](https://scholarfriends.com/storage/[PDF] [eBook] for Corporate Finance The Core, 5th Edition By Jonathan Berk, Peter Demarzo.png)

eBook [PDF] Corporate Finance The Core, 5th Edition By Jonatha...

![Preview of International Financial Reporting 7e Alan Melville [eBook] [PDF]](https://scholarfriends.com/storage/[eBook] [PDF] for International Financial Reporting 7e Alan Melville.png)

International Financial Reporting 7e Alan Melville [eBook] [PD...

Fundamentals of Corporate Finance, 11e Richard Brealey, Stewar...

![Preview of Financial Management Theory & Practice, 16e By Brigham, Eugene Ehrhardt, Michael [eBook] [](https://scholarfriends.com/storage/[eBook] [PDF] for Financial Management Theory & Practice, 16e By Brigham, Eugene Ehrhardt, Michael.png)

Financial Management Theory & Practice, 16e By Brigham, Eugene...

Test Bank for Financial Reporting and Analysis, 8th Edition Re...

Financial Reporting and Analysis, 8e Lawrence Revsine, Daniel...

Corporate Financial Management, 6e Glen Arnold, Deborah Lewis...