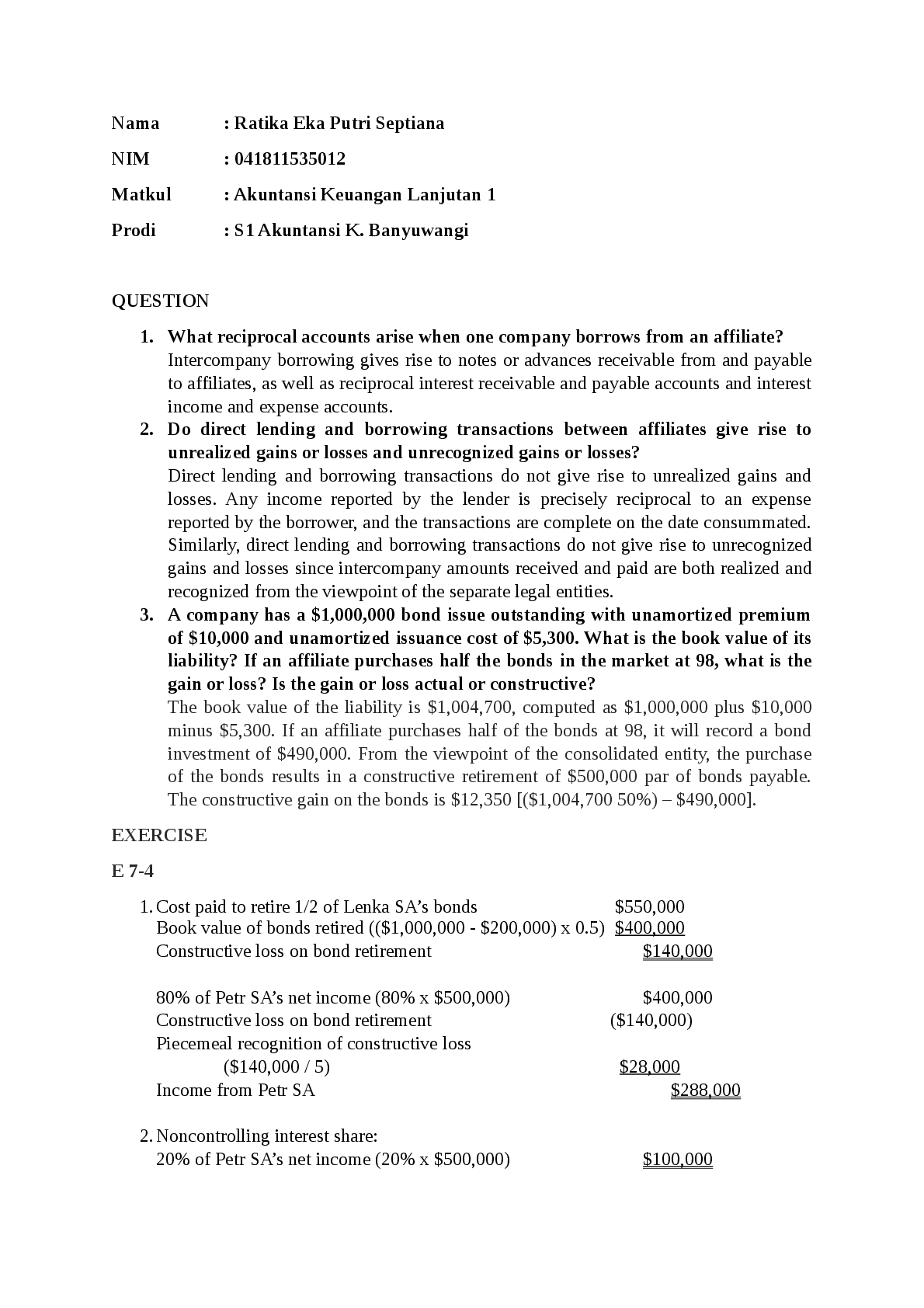

N.B.: TYPE indicates that a question is new, modified, or unchanged, as follows.

N A question new to this edition of the Test Bank.

+ A question modified from the previous edition of the Test Bank.

= A question inc

...

N.B.: TYPE indicates that a question is new, modified, or unchanged, as follows.

N A question new to this edition of the Test Bank.

+ A question modified from the previous edition of the Test Bank.

= A question included in the previous edition of the Test Bank.

A1. Professionals are required to deliver competent services.

T PAGE: 933 TYPE: N

NAT: AACSB Analytic AICPA Legal

A2. Accountants and other professionals do not face liability under the common law for any breach of contract.

F PAGE: 933 TYPE: N

NAT: AACSB Analytic AICPA Legal

A3. Generally, an accountant must possess the skills that an ordinarily prudent accountant would have.

T PAGE: 934 TYPE: N

NAT: AACSB Analytic AICPA Legal

A4. An accountant normally will be held liable to the client for a mistake in judgment.

F PAGE: 934 TYPE: N

NAT: AACSB Analytic AICPA Legal

A5. An accountant who performs an audit is liable for failing to detect misconduct even if a normal audit would not have revealed it.

F PAGE: 935 TYPE: N

NAT: AACSB Analytic AICPA Legal

A6. Under rules of professional conduct, committing a criminal act that reflects adversely on a person’s “honesty” is professional misconduct.

T PAGE: 936 TYPE: N

NAT: AACSB Analytic AICPA Legal

A7. In all cases involving allegations of negligence, the plaintiff must prove that the professional’s breach of the duty of care actually caused some injury.

T PAGE: 936 TYPE: N

NAT: AACSB Analytic AICPA Legal

A8. Under rules of professional conduct, an attorney should not engage in conduct involving “misrepresentation.”

T PAGE: 936 TYPE: +

NAT: AACSB Analytic AICPA Legal

A9. A professional’s gross negligence in performing a duty constitutes actual fraud.

F PAGE: 936 TYPE: +

NAT: AACSB Analytic AICPA Legal

A10. An innocent professional is never liable for a co-professional’s misconduct.

F PAGE: 938 TYPE: N

NAT: AACSB Analytic AICPA Legal

A11. In some states, in the absence of privity, a party cannot recover from am accountant.

T PAGE: 938 TYPE: N

NAT: AACSB Analytic AICPA Legal

A12. In most courts, accountants are subject to liability for negligence only to their clients.

F PAGE: 939 TYPE: N

NAT: AACSB Analytic AICPA Legal

A13. An attorney may be liable in negligence to any third party.

F PAGE: 939 TYPE: +

NAT: AACSB Analytic AICPA Legal

A14. The Sarbanes-Oxley Act of 2002 applies only to domestic public accounting firms that provide auditing services to “issuers.”

F PAGE: 941 TYPE: N

NAT: AACSB Analytic AICPA Critical Thinking

A15. Under the Sarbanes-Oxley Act of 2002, accountants must dispose of working papers relating to an audit or review.

F PAGE: 942 TYPE: N

NAT: AACSB Analytic AICPA Legal

A16. An accountant may be liable for a misstatement or omission of material fact in a registration statement.

T PAGE: 942 TYPE: N

NAT: AACSB Analytic AICPA Legal

A17. An accountant is not liable for a misstatement in a registration statement to a purchaser of securities if the misstatement was not of a material fact.

T PAGE: 942 TYPE: N

NAT: AACSB Analytic AICPA Legal

A18. An accountant is not liable for a false statement that affects the price of a security if the buyer or seller of the security knew the statement was false.

T PAGE: 945 TYPE: N

NAT: AACSB Analytic AICPA Legal

A19. For a plaintiff to recover damages under Section 10(b) of the Securities Exchange Act of 1934 and SEC Rule 10b-5, ordinary negligence is enough.

F PAGE: 946 TYPE: N

NAT: AACSB Analytic AICPA Legal

A20. In no states are communications between an accountant and his or her client privileged.

F PAGE: 949 TYPE: +

NAT: AACSB Analytic AICPA Legal

MULTIPLE CHOICE QUESTIONS

A1. Leslie, an accountant, enters into a contract to provide services to Marty. Leslie does not finish the work within the contract’s deadline. Leslie is

a. liable for breach of contract.

b. not liable, because Leslie is a professional.

c. not liable, because Leslie’s failure must have been Marty‘s fault.

d. not liable, because the work took longer than foreseen.

A PAGE: 933 TYPE: =

NAT: AACSB Reflective AICPA Legal

A2. Lucille, an accountant, is subject to the ac¬counting conventions, rules, and procedures that constitute generally ac¬cepted accounting principles (GAAP). GAAP are determined by

a. the International Accounting Standards Board.

b. the American Bar Association.

c. the American Institute of Certified Public Accountants.

d. the Financial Accounting Standards Board.

D PAGE: 934 TYPE: +

NAT: AACSB Reflective AICPA Critical Thinking

A3. Jim, an accountant, contracts to perform services for Kasey. Jim acts in good faith and conforms with generally accepted accounting principles, but makes a mistake in judgment. Jim is most likely

a. liable if Jim failed to discover a defalcation.

b. liable if Jim failed to discover a fraud.

c. liable if Jim failed to discover an impropriety.

d. not liable.

D PAGE: 934 TYPE: =

NAT: AACSB Reflective AICPA Legal

A4. Dwayne can be described as “a reasonably competent general practitioner of ordinary skill, experience, and capacity.” This is the normal standard for judging the performance of

a. a client.

b. an accountant.

c. an attorney.

d. a tax preparer.

C PAGE: 935 TYPE: +

NAT: AACSB Reflective AICPA Legal

A5. Penelope is an attorney. Penelope’s conduct is governed by rules of professional conduct established by the state in which she is licensed, and the Model Rules of Professional Conduct drafted by

a. federal courts.

b. the American Bar Association.

c. the American Institute of Certified Public Accountants.

d. the International Accounting Standards Board.

B PAGE: 935 TYPE: +

NAT: AACSB Reflective AICPA Critical Thinking

A6. National Business Systems Corporation (NBS) files a suit against Molly, its former accountant, alleging constructive fraud. NBS need not prove

a. detrimental reliance.

b. intent to deceive.

c. justifiable reliance.

d. materiality.

B PAGE: 936 TYPE: =

NAT: AACSB Reflective AICPA Legal

A7. Jim, an attorney, allows a statute of limitations to lapse on a claim by Midwest Manufacturing Company, a client. Jim

a. can be held liable for malpractice.

b. has violated an ethical standard but cannot be held liable.

c. is subject to criminal penalties under the statute of limitations.

d. will be automatically disbarred.

A PAGE: 936 TYPE: =

NAT: AACSB Reflective AICPA Legal

A8. Grover Nut Company files a suit against Hud, its former account¬ant, alleging actual fraud. Grover must prove

a. intent to deceive.

b. misrepresentation of a non-material fact.

c. the lack of an injury.

d. unjustifiable reliance.

A PAGE: 936 TYPE: =

NAT: AACSB Reflective AICPA Legal

A9. Bob, an accountant, intentionally misstates a material fact to mislead Consolidated Industries, Inc., a client. Consolidated justifiably relies on the misstatement to its detriment. Bob is most likely liable for

a. actual fraud.

b. constructive fraud.

c. destructive fraud.

d. virtual fraud.

A PAGE: 936 TYPE: =

NAT: AACSB Reflective AICPA Legal

A10. Lebron accuses Moe, an attorney, of committing malpractice. Malpractice is

a. a breach of ethics.

b. a defalcation.

c. a mistake in judgment.

d. professional negligence.

D PAGE: 936 TYPE: =

NAT: AACSB Reflective AICPA Legal

A11. Marquis Company’s liabilities exceed its assets, but the firm’s employees falsify its books to reflect a positive net worth. Marquis hires Nan & Ollie, an accounting firm, to prepare a balance sheet, which is certified to show a net worth. Pure Credit Corporation relies on the balance sheet to make a loan to Marquis. When the firm defaults, Pure Credit files a suit against Nan & Ollie. Under the Ultramares rule, the accounting firm is most likely

a. liable because Nan & Ollie owed a duty of care to all third parties.

b. liable because Nan & Ollie owed a duty of care to Marquis.

c. liable because Nan & Ollie owed a duty to any foreseeable user.

d. not liable because Nan & Ollie and Pure Credit were not in privity.

D PAGE: 938 TYPE: =

NAT: AACSB Reflective AICPA Legal

A12. Faith and Gordon are accountants who work together. Faith and Gordon can limit their potential liability for each other’s misconduct by organizing their business as

a. a foreign corporation.

b. a non-professional corporation.

c. an unincorporated corporation.

d. a professional corporation.

D PAGE: 938 TYPE: N

NAT: AACSB Reflective AICPA Legal

A13. Rollo is an attorney whose clients include Superior Credit Company. If Rollo is negligent in his work for Superior, under the Restatement (Second) of Torts, Rollo may be liable to Superior and

a. any third party.

b. no third party.

c. third parties who are foreseen users of the work.

d. third parties who are reasonably foresee¬able users of the work.

C PAGE: 939 TYPE: =

NAT: AACSB Reflective AICPA Legal

A14. Quin, an accountant, prepares for Reddy, Inc., a financial state¬ment that omits a material fact. The statement is included in Reddy’s registration statement with the Securities and Exchange Commission. Timor, who reads the statement, and Ubi, who does not, each buy Reddy stock. Velma reads the statement but does not buy the stock. Under Section 11 of the Securities Act of 1933, Quin may be liable to

a. no one.

b. Timor and Ubi.

c. Timor, Ubi, and Velma.

d. Ubi only.

B PAGE: 942 TYPE: +

NAT: AACSB Reflective AICPA Legal

A15. Craig is an accountant whose clients include Digby National Corporation. Elbert is Craig’s attorney. Working papers that Craig develops when preparing financial reports for Digby are owned by

a. Craig.

b. Digby.

c. Elbert.

d. no one—the papers must be destroyed immediately after use.

A PAGE: 942 TYPE: =

NAT: AACSB Reflective AICPA Legal

A16. Pat, an accountant, includes a false statement in a report for Quantity, Inc., that is filed with the Securities and Exchange Commis¬sion. Quantity publishes a misleading ad about its future prospects. Rita sees the ad and calls Stan, who buys stock in Quantity. Under Section 18 of the Securities Ex¬change Act of 1934, liability may attach to

a. Pat’s report.

b. Quantity’s ad.

c. Rita’s call.

d. Stan’s purchase.

A PAGE: 945 TYPE: =

NAT: AACSB Reflective AICPA Legal

A17. Longhaul Freight, Inc., files a suit against Midge, an accountant, under the antifraud provisions of the Securities Exchange Act of 1934 and Rule 10b-5 of the Securities and Exchange Commission. To succeed, Longhaul must show that Midge

a. acted with scienter.

b. bought or sold a security.

c. is incompetent.

d. knows nothing about securities.

A PAGE: 946 TYPE: =

NAT: AACSB Reflective AICPA Legal

A18. Flynn, an accountant, helps Grange Supply Company prepare and file a false federal corporate income tax return. Under the In¬ternal Revenue Code, this is

a. a felony punishable by a fine and imprisonment.

b. a felony punishable only by a fine.

c. a misdemeanor punishable only by a fine.

d. a civil violation subject to a liability suit but not a crime.

A PAGE: 948 TYPE: =

NAT: AACSB Reflective AICPA Legal

A19. Feder prepares federal corporate income tax returns for Giant Stores, Inc., and other firms. Under the Internal Revenue Code, with respect to an understatement of a client’s tax liability, Feder may be liable for

a. negligent or willful misconduct.

b. no misconduct.

c. only negligent misconduct.

d. only willful misconduct.

A PAGE: 948 TYPE: =

NAT: AACSB Reflective AICPA Legal

A20. Pace is an attorney, whose clients include Quikfeet Running Shoes Company. Unless Quikfeet has violated securities law, the contents of Pace’s file on Quikfeet may be disclosed to someone other than Quikfeet

a. only to a third party who is a foreseeable user of the information.

b. only under a court order (with or without Quikfeet’s consent).

c. only with Quikfeet’s consent.

d. under any circumstances.

C PAGE: 949 TYPE: =

NAT: AACSB Reflective AICPA Legal

ESSAY QUESTIONS

A1. Bowie, a certified public accountant, prepares and certifies Candy Products Corporation’s financial statements. These statements are in¬cluded in Candy’s registration statement filed with the Securities and Exchange Commission before Candy’s offering of securities. Dona buys a security covered by the registration statement. Based on this transaction, Dona files a suit against Bowie under Section 11 and Section 10(b) of the Securities Exchange Act of 1934. To succeed in the suit, what must Dona prove? Bowie responds that Dona was not in priv¬ity with him and that even if she had been in privity, she cannot prove his lack of due diligence. Can Bowie prevail on these grounds? Why or why not?

A2. Sian, an accountant, prepares a tax return for a client, Toy Sales Company. Vita, who is not an accountant, prepares a tax return for Wu’s business, Xtra Delivery Service. Is an accountant who prepares a tax return for a client liable for any false statements in the return? Is a person who is not an accountant and who prepares a tax return for some¬one else liable for any false statements in the return?

[Show More]

Med Surg test Latest Verified Questions and all Correct Answers with Explanations Chapter 48 Assessment and Management of Patients with Obesity.png)

Correct Study Guide, Download to Score A.png)

.png)

Med Surg test Latest Verified Questions and all Correct Answers with Explanations Chapter 48 Assessment and Management of Patients with Ob.png)