Financial Accounting > QUESTIONS & ANSWERS > ACCT 3010 INTERMEDIATE ACCOUNTING I EXAM 2 TEST QUESTIONS and ANSWERS (All)

ACCT 3010 INTERMEDIATE ACCOUNTING I EXAM 2 TEST QUESTIONS and ANSWERS

Document Content and Description Below

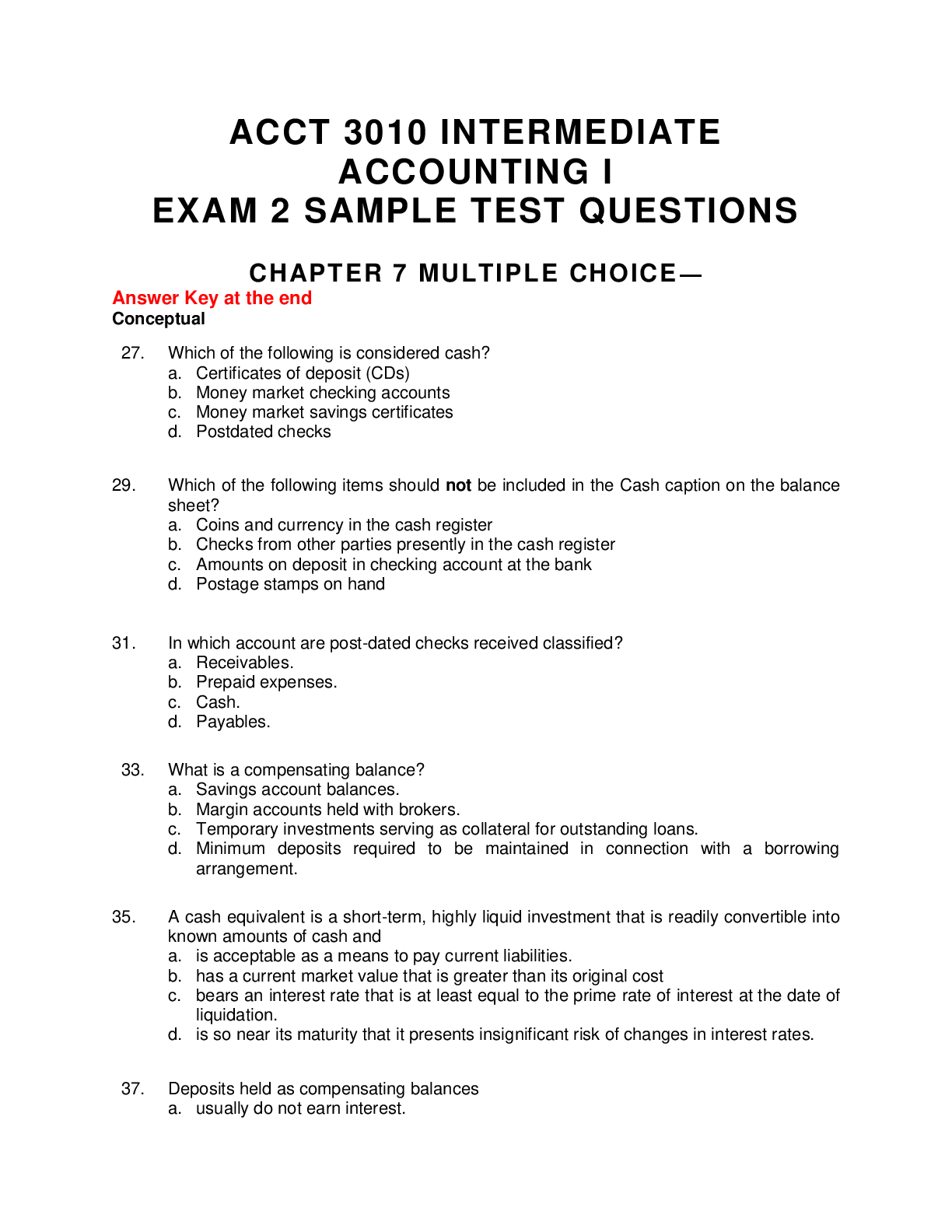

CHAPTER 7 MULTIPLE CHOICE— Answer Key at the end Conceptual 27. Which of the following is considered cash? a. Certificates of deposit (CDs) b. Money market checking accounts c. Money mark ... et savings certificates d. Postdated checks 29. Which of the following items should not be included in the Cash caption on the balance sheet? a. Coins and currency in the cash register b. Checks from other parties presently in the cash register c. Amounts on deposit in checking account at the bank d. Postage stamps on hand 31. In which account are post-dated checks received classified? a. Receivables. b. Prepaid expenses. c. Cash. d. Payables. 33. What is a compensating balance? a. Savings account balances. b. Margin accounts held with brokers. c. Temporary investments serving as collateral for outstanding loans. d. Minimum deposits required to be maintained in connection with a borrowing arrangement. 35. A cash equivalent is a short-term, highly liquid investment that is readily convertible into known amounts of cash and a. is acceptable as a means to pay current liabilities. b. has a current market value that is greater than its original cost c. bears an interest rate that is at least equal to the prime rate of interest at the date of liquidation. d. is so near its maturity that it presents insignificant risk of changes in interest rates. 37. Deposits held as compensating balances a. usually do not earn interest. b. if legally restricted and held against short-term credit may be included as cash. c. if legally restricted and held against long-term credit may be included among current assets. d. none of these answers are correct. 39. Which of the following statements is correct regarding receivables? a. Receivables are written promises of the purchaser to pay for goods or services. b. Receivables are claims held against customers and others for money, goods, or services. c. Receivables are non-financial assets. d. Receivables that are expected to be collected within a year are classified as noncurrent. 41. Which of the following should be recorded in Accounts Receivable? a. Receivables from officers b. Receivables from subsidiaries c. Dividends receivable d. None of these answer choices are correct. 43. When a customer purchases merchandise inventory from a business organization, she may be given a discount which is designed to induce prompt payment. Such a discount is called a(n) a. trade discount. b. nominal discount. c. enhancement discount. d. cash discount. 45. If a company employs the gross method of recording accounts receivable from customers, then sales discounts taken should be reported as a. a deduction from sales in the income statement. b. an item of "other expense" in the income statement. c. a deduction from accounts receivable in determining the net realizable value of accounts receivable. d. sales discounts forfeited in the cost of goods sold section of the income statement. 47. The accounting for cash discounts and trade discounts are a. the same. b. always recorded net. c. not the same. d. tied to the timing of cash collections on the account. 49. All of the following are problems associated with the valuation of accounts receivable except a. uncollectible accounts. b. returns. c. cash discounts under the net method. d. allowances granted. 51. Which of the following concepts relates to using the allowance method in accounting for accounts receivable? a. Bad debt expense is an estimate that is based on historical and prospective information. b. Bad debt expense is based on the actual amounts determined to be uncollectible. c. Bad debt expense is an estimate that is based only on an analysis of the receivables aging. d. Bad debt expense is management's determination of which accounts will be sent to the attorney for collection. 53. What is the normal journal entry for recording bad debt expense under the allowance method? a. Debit Allowance for Doubtful Accounts, credit Accounts Receivable. b. Debit Allowance for Doubtful Accounts, credit Bad Debt Expense. c. Debit Bad Debt Expense, credit Allowance for Doubtful Accounts. d. Debit Accounts Receivable, credit Allowance for Doubtful Accounts. 55. Which of the following is included in the normal journal entry to record the collection of accounts receivable previously written off when using the allowance method? a. Debit Allowance for Doubtful Accounts, credit Accounts Receivable. b. Debit Allowance for Doubtful Accounts, credit Bad Debt Expense. c. Debit Bad Debt Expense, credit Allowance for Doubtful Accounts. d. Debit Accounts Receivable, credit Allowance for Doubtful Accounts. 57. Which of the following methods of determining bad debt expense does not properly match expense and revenue? a. Charging bad debts with a percentage of sales under the allowance method. b. Charging bad debts with an amount derived from a percentage of accounts receivable under the allowance method. c. Charging bad debts with an amount derived from aging accounts receivable under the allowance method. d. Charging bad debts as accounts are written off as uncollectible. 59. Which of the following is a generally accepted method of determining the amount of the adjustment to bad debt expense? a. A percentage of sales adjusted for the balance in the allowance b. A percentage of sales not adjusted for the balance in the allowance c. A percentage of accounts receivable not adjusted for the balance in the allowance d. An amount derived from aging accounts receivable and not adjusted for the balance in the allowance. 61. At the beginning of 2013, Gannon Company received a three-year zero-interest-bearing $1,000 trade note. The market rate for equivalent notes was 8% at that time. Gannon reported this note as a $1,000 trade note receivable on its 2013 year-end statement of financial position and $1,000 as sales revenue for 2013. What effect did this accounting for the note have on Gannon's net earnings for 2013, 2014, 2015, and its retained earnings at the end of 2015, respectively? a. Overstate, overstate, understate, zero b. Overstate, understate, understate, understate c. Overstate, overstate, overstate, overstate d. None of these answer choices are correct. 63. Antique Company has notes receivable that have a fair value of $920,000 and a carrying amount of $710,000. Antique decides on December 31, 2014, to use the fair value option for these recently-acquired receivables. The adjusting entry to record this change will include a: a. debit to Unrealized Holding Gain or LossIncome for $210,000. b. credit to Notes Receivable for $210,000. c. credit to Unrealized Holding Gain or LossIncome for $210,000. d. debit to Notes Receivable for $920,000. 65. Why would a company sell receivables to another company? a. To improve the quality of its credit granting process. b. To limit its legal liability. c. To accelerate access to amounts collected. d. To comply with customer agreements. 67. What is "recourse" as it relates to selling receivables? a. The obligation of the seller of the receivables to pay the purchaser in case the debtor fails to pay. b. The obligation of the purchaser of the receivables to pay the seller in case the debtor fails to pay c. The obligation of the seller of the receivables to pay the purchaser in case the debtor returns the product related to the sale. d. The obligation of the purchaser of the receivables to pay the seller if all of the receivables are collected. 69. Which of the following statements is incorrect regarding the classification of accounts and notes receivable? a. Segregation of the different types of receivables is required if they are material. b. Disclose any loss contingencies that exist on the receivables. c. Any discount or premium resulting from the determination of present value in notes receivable transactions is an asset or liability respectively. d. Valuation accounts should be ap¬propriately offset against the proper receivable accounts. 71. The accounts receivable turnover ratio measures the a. number of times the average balance of accounts receivable is collected during the period. b. percentage of accounts receivable turned over to a collection agency during the period. c. percentage of accounts receivable arising during certain seasons. d. number of times the average balance of inventory is sold during the period. 73. Which of the following items should be included in accounts receivable reported on the balance sheet? a. Notes receivable. b. Interest receivable. c. Allowance for doubtful accounts. d. Advances to related parties and officers. 75. What is a possible reason for accounts receivable turnover to increase from one year to the next year a. Decreased credit sales during a recession. b. Write-off uncollectible receivables. c. Granting credit to customers with lower credit quality. d. Improved collection process. *77. Which of the following is an appropriate reconciling item to the balance per bank in a bank reconciliation? a. Bank service charge. b. Deposit in transit. c. Bank interest. d. Chargeback for NSF check. *79. A Cash Over and Short account a. is not generally accepted. b. is debited when the petty cash fund proves out over. c. is debited when the petty cash fund proves out short. d. is a contra account to Cash. *81. When preparing a bank reconciliation, bank credits are a. added to the bank statement balance. b. deducted from the bank statement balance. c. added to the balance per books. d. deducted from the balance per books. Multiple Choice Answers—Conceptual Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. CHAPTER 7 MULTIPLE CHOICE—Computational 83. On January 1, 2014, Lynn Company borrows $2,000,000 from National Bank at 11% annual interest. In addition, Lynn is required to keep a compensatory balance of $200,000 on deposit at National Bank which will earn interest at 5%. The effective interest that Lynn pays on its $2,000,000 loan is a. 10.0%. b. 11.0%. c. 11.5%. d. 11.6%. 85. Kaniper Company has the following items at year-end: Cash in bank $30,000 Petty cash 300 Short-term paper with maturity of 2 months 5,500 Postdated checks 1,400 Kaniper should report cash and cash equivalents of a. $30,000. b. $30,300. c. $35,800. d. $37,200. 87. Steinert Company has the following items at year-end: Cash in bank $35,000 Petty cash 500 Short-term paper with maturity of 2 months 8,200 Postdated checks 2,100 Steinert should report cash and cash equivalents of a. $35,000. b. $35,500. c. $43,700. d. $45,800. 89. AG Inc. made a $15,000 sale on account with the following terms: 1/15, n/30. If the company uses the net method to record sales made on credit, how much should be recorded as revenue? a. $14,700. b. $14,850. c. $15,000. d. $15,150. 91. AG Inc. made a $15,000 sale on account with the following terms: 2/10, n/30. If the company uses the net method to record sales made on credit, what is/are the debit(s) in the journal entry to record the sale? a. Debit Accounts Receivable for $14,700. b. Debit Accounts Receivable for $14,700 and Sales Discounts for $300. c. Debit Accounts Receivable for $15,000. d. Debit Accounts Receivable for $15,000 and Sales Discounts for $300. 93. On April 2, Kelvin sold $30,000 of inventory items on credit with the terms 1/10, net 30. Payment on $18,000 sales was received on April 8 and the remaining payment on $12,000 sales was received on April 27. Assuming Kelvin uses the net method of accounting for sales discounts, the entry recorded on April 27 would include a: a. debit to Cash and credit to Accounts Receivable for $11,880. b. debit to Accounts Receivable and credit to Sales Revenue for $30,000. c. debit to Accounts Receivable and credit to Sales Discount Forfeited for $120. d. debit to Cash and credit to Sales Discount Forfeited for $300. 95. Jenny Manufactures sold toys listed at $240 per unit to Jack Inc. for $204, a trade discount of 15 percent. Jack Inc. in turn sells the toys in the market at $225. Jenny should record the receivable and related sales revenue (per unit) at: a. $240. b. $225. c. $204. d. $191. 97. Wellington Corp. has outstanding accounts receivable totaling $1.27 million as of December 31 and sales on credit during the year of $6.4 million. There is also a debit balance of $3,000 in the allowance for doubtful accounts. If the company estimates that 1% of its net credit sales will be uncollectible, what will be the balance in the allowance for doubtful accounts after the year-end adjustment to record bad debt expense? a. $12,700. b. $15,700. c. $61,000. d. $67,000. 99. Wellington Corp. has outstanding accounts receivable totaling $5 million as of December 31 and sales on credit during the year of $25 million. There is also a debit balance of $20,000 in the allowance for doubtful accounts. If the company estimates that 8% of its outstanding receivables will be uncollectible, what will be the balance in the allowance for doubtful accounts after the year-end adjustment to record bad debt expense? a. $2,000,000. b. $ 380,000. c. $ 400,000. d. $ 420,000. 101. Before year-end adjusting entries, Dunn Company's account balances at December 31, 2014, for accounts receivable and the related allowance for uncollectible accounts were $1,200,000 and $90,000, respectively. An aging of accounts receivable indicated that $125,000 of the December 31 receivables are expected to be uncollectible. The net realizable value of accounts receivable after adjustment is a. $1,165,000. b. $1,075,000. c. $985,000. d. $1,110,000. 103. The following information is available for Murphy Company: Allowance for doubtful accounts at December 31, 2013 $ 16,000 Credit sales during 2014 800,000 Accounts receivable deemed worthless and written off during 2014 18,000 As a result of a review and aging of accounts receivable in early January 2015, it has been determined that an allowance for doubtful accounts of $11,000 is needed at December 31, 2014. What amount should Murphy record as "bad debt expense" for the year ended December 31, 2014? a. $9,000 b. $11,000 c. $13,000 d. $27,000 105. A trial balance before adjustments included the following: Debit Credit Sales $850,000 Sales returns and allowance $28,000 Accounts receivable 86,000 Allowance for doubtful accounts 1,520 105. If the estimate of uncollectibles is made by taking 10% of gross account receivables, the amount of the adjustment is a. $7,080. b. $8,600. c. $8,448. d. $10,120. 107. Smithson Corporation had a 1/1/14 balance in the Allowance for Doubtful Accounts of $20,000. During 2014, it wrote off $14,400 of accounts and collected $4,200 on accounts previously written off. The balance in Accounts Receivable was $400,000 at 1/1 and $480,000 at 12/31. At 12/31/14, Smithson estimates that 5% of accounts receivable will prove to be uncollectible. What is Bad Debt Expense for 2014? a. $4,000. b. $14,200. c. $18,400. d. $24,000. 109. Shelton Company has the following account balances at year-end: Accounts receivable $120,000 Allowance for doubtful accounts 7,200 Sales discounts 4,800 Shelton should report accounts receivable at a net amount of a. $108,000. b. $112,800. c. $115,200. d. $120,000. 111. McGlone Corporation had a 1/1/14 balance in the Allowance for Doubtful Accounts of $25,000. During 2014, it wrote off $18,000 of accounts and collected $5,250 on accounts previously written off. The balance in Accounts Receivable was $500,000 at 1/1 and $600,000 at 12/31. At 12/31/14, McGlone estimates that 5% of accounts receivable will prove to be uncollectible. What should McGlone report as its Allowance for Doubtful Accounts at 12/31/14? a. $12,000. b. $12,250. c. $17,250. d. $30,000. 113. On December 31, 2014, Flint Corporation sold for $100,000 an old machine having an original cost of $180,000 and a book value of $80,000. The terms of the sale were as follows: $20,000 down payment $40,000 payable on December 31 each of the next two years The agreement of sale made no mention of interest; however, 9% would be a fair rate for this type of transaction. What should be the amount of the notes receivable net of the unamortized discount on December 31, 2014 rounded to the nearest dollar? (The present value of an ordinary annuity of 1 at 9% for 2 years is 1.75911.) a. $70,364 b. $90,364. c. $80,000. d. $140,728. 115. Equestrain Roads sold $80,000, of goods and accepted the customer's $80,000 10%, 1-year note receivable in exchange. Assuming 10% approximates the market rate of return, what would be the debit in this journal entry to record the sale? a. No journal entry until cash is collected. b. Debit Notes Receivable for $80,000. c. Debit Accounts Receivable for $80,000. d. Debit Notes Receivable for $72,000. 117. Equestrain Roads accepted a customer's $50,000 zero-interest-bearing six-month note payable in a sales transaction. The product sold normally sells for $46,000. If the sale was made on June 30, how much interest revenue from this transaction would be recorded for the year ending December 31? a. $0. b. $2,000. c. $4,000. d. $5,000. 119. Jones Company has notes receivable that have a fair value of $570,000 and a carrying amount of $750,000. Jones decides on December 31, 2014, to use the fair value option for these recently-acquired receivables. Which of the following entries will be made on December 31, 2014 to record the unrealized holding gain/loss? a. Unrealized Holding Gain or LossIncome 180,000 Notes Receivable 180,000 b. Unrealized Holding Gain or LossEquity 180,000 Notes Receivable 180,000 c. Notes Receivable 180,000 Unrealized Holding Gain or LossIncome 180,000 d. Notes Receivable 180,000 Unrealized Holding Gain or LossEquity 180,000 121. Sun Inc. factors $3,000,000 of its accounts receivables with recourse for a finance charge of 3%. The finance company retains an amount equal to 10% of the accounts receivable for possible adjustments. Sun estimates the fair value of the recourse liability at $150,000. What would be recorded as a gain (loss) on the transfer of receivables? a. Gain of $90,000. b. Loss of 240,000. c. Gain of $540,000. d. Loss of $150,000. 123. Moon Inc. factors $2,000,000 of its accounts receivables with recourse for a finance charge of 4%. The finance company retains an amount equal to 8% of the accounts receivable for possible adjustments. Moon estimates the fair value of the recourse liability at $200,000. What would be the debit to Cash in the journal entry to record this transaction? a. $2,000,000. b. $1,920,000. c. $1,760,000. d. $1,560,000. 125. Geary Co. assigned $800,000 of accounts receivable to Kwik Finance Co. as security for a loan of $670,000. Kwik charged a 2% commission on the amount of the loan; the interest rate on the note was 10%. During the first month, Geary collected $220,000 on assigned accounts after deducting $760 of discounts. Geary accepted returns worth $2,700 and wrote off assigned accounts totaling $5,960. The amount of cash Geary received from Kwik at the time of the assignment was a. $603,000. b. $654,000. c. $656,600. d. $670,000. 127. On February 1, 2014, Henson Company factored receivables with a carrying amount of $500,000 to Agee Company. Agee Company assesses a finance charge of 3% of the receivables and retains 5% of the receivables. Relative to this transaction, you are to determine the amount of loss on sale to be reported in the income statement of Henson Company for February. Assume that Henson factors the receivables on a without recourse basis. The loss to be reported is a. $0. b. $15,000. c. $25,000. d. $40,000. 129. Maxwell Corporation factored, with recourse, $100,000 of accounts receivable with Huskie Financing. The finance charge is 3%, and 5% was retained to cover sales discounts, sales returns, and sales allowances. Maxwell estimates the recourse obligation at $2,400. What amount should Maxwell report as a loss on sale of receivables? a. $ -0-. b. $3,000. c. $5,400. d. $10,400. 131. Remington Corporation had accounts receivable of $100,000 at 1/1. The only transactions affecting accounts receivable were sales of $750,000 and cash collections of $700,000. The accounts receivable turnover is a. 5.0. b. 5.5. c. 6.0. d. 7.5. 133. The opening balance of Accounts Receivable for George Company was $25,000. Net sales (all on account) for the year amounted to $150,000. The Company doesn’t offer any cash discount. During the year $130,000 was collected on accounts receivable. Compute accounts receivable turnover ratio for the year. a. 4.29 times b. 3.71 times c. 2.89 times d. 7.50 times *135. If a petty cash fund is established in the amount of $250, and contains $150 in cash and $95 in receipts for disbursements when it is replenished, the journal entry to record replenishment should include credits to the following accounts a. Petty Cash, $75. b. Petty Cash, $100. c. Cash, $95; Cash Over and Short, $5. d. Cash, $100. *137. In preparing its bank reconciliation for the month of April 2014, Henke, Inc. has the following information available. Balance per bank statement, 4/30/14 $34,140 NSF check returned with 4/30/14 bank statement 450 Deposits in transit, 4/30/14 5,000 Outstanding checks, 4/30/14 5,200 Bank service charges for April 20 What should be the correct balance of cash at April 30, 2014? a. $34,370 b. $33,940 c. $33,490 d. $33,470 *139. The cash account shows a balance of $90,000 before reconciliation. The bank statement does not include a deposit of $4,600 made on the last day of the month. The bank statement shows a collection by the bank of $1,880 and a customer's check for $640 was returned because it was NSF. A customer's check for $900 was recorded on the books as $1,080, and a check written for $158 was recorded as $194. The correct balance in the cash account was a. $91,024. b. $91,096. c. $91,456. d. $95,696. CHAPTER 8 MULTIPLE CHOICE—Conceptual 21. Which of the following inventories carried by a manufacturer is similar to the merchandise inventory of a retailer? a. Raw materials. b. Work-in-process. c. Finished goods. d. Supplies. 23. Under what circumstances should a company with high rate of return on sales consider the inventory sold? a. When it can reasonably estimate the amount of returns b. When the retailer gives a confirmation that the goods won’t be returned c. When the goods are sold on installment d. When the payment for goods is received 25. Which of the following is a characteristic of a perpetual inventory system? a. Inventory purchases are debited to a Purchases account. b. Inventory records are not kept for every item. c. Cost of goods sold is recorded with each sale. d. Cost of goods sold is determined as the amount of purchases less the change in inventory. 27. Where should goods in transit that were recently purchased f.o.b. destination be included on the balance sheet? a. Accounts payable. b. Inventory. c. Equipment. d. Not on the balance sheet. 29. If a company uses the periodic inventory system, what is the impact on the current ratio of including goods in transit f.o.b. shipping point in purchases, but not ending inventory? a. Overstate the current ratio. b. Understate the current ratio. c. No effect on the current ratio. d. Not sufficient information to determine effect on the current ratio. 31. When using a perpetual inventory system, a. no Purchases account is used. b. a Cost of Goods Sold account is used. c. two entries are required to record a sale. d. All of these answer choices are correct. 33. Goods in transit which are shipped f.o.b. destination should be a. included in the inventory of the seller. b. included in the inventory of the buyer. c. included in the inventory of the shipping company. d. none of these answers are correct. 35. During 2014 Carne Corporation transferred inventory to Nolan Corporation and agreed to repurchase the merchandise early in 2015. Nolan then used the inventory as collateral to borrow from Norwalk Bank, remitting the proceeds to Carne. In 2015 when Carne repurchased the inventory, Nolan used the proceeds to repay its bank loan. This transaction is known as a(n) a. consignment. b. installment sale. c. assignment for the benefit of creditors. d. product financing arrangement. 37. Goods on consignment are a. included in the consignee's inventory. b. included in the consignor’s inventory. c. included in the consignee’s revenue. d. included in both the consignee’s and the consignor’s inventory. 39. The accountant for the Pryor Sales Company is preparing the income statement for 2014 and the balance sheet at December 31, 2014. Pryor uses the periodic inventory system. The January 1, 2014 merchandise inventory balance will appear a. only as an asset on the balance sheet. b. only in the cost of goods sold section of the income statement. c. as a deduction in the cost of goods sold section of the income statement and as a current asset on the balance sheet. d. as an addition in the cost of goods sold section of the income statement and as a current asset on the balance sheet. 41. The failure to record a purchase of mer¬chandise on account even though the goods are properly included in the physical inven¬tory results in a. an overstatement of assets and net income. b. an understatement of assets and net income. c. an understatement of cost of goods sold and liabilities and an overstatement of assets. d. an understatement of liabilities and an overstatement of owners' equity. 43. Green Co. received merchandise on consignment. As of January 31, Green included the goods in inventory, but did not record the transaction. The effect of this on its financial statements for January 31 would be a. net income, current assets, and retained earnings were overstated. b. net income was correct and current assets were understated. c. net income and current assets were overstated and current liabilities were understated. d. net income, current assets, and retained earnings were understated. 45. On June 15, 2014, Wynne Corporation accepted delivery of merchandise which it pur-chased on account. As of June 30, Wynne had not recorded the transaction or included the merchandise in its inventory. The effect of this on its balance sheet for June 30, 2014 would be a. assets and stockholders' equity were overstated but liabilities were not affected. b. stockholders' equity was the only item affected by the omission. c. assets, liabilities, and stockholders' equity were understated. d. assets and liabilities were understated but stockholders’ equity was not affected. 47. Which of the following is a product cost as it relates to inventory? a. Selling costs. b. Interest costs. c. Raw materials. d. Abnormal spoilage. 49. Which method may be used to record cash discounts a company receives for paying suppliers promptly? a. Net method. b. Gross method. c. Average method. d. Both the net method and the gross method. 51. Which of the following is correct? a. Selling costs are product costs. b. Manufacturing overhead costs are product costs. c. Interest costs for routine inventories are product costs. d. All of these answers are correct. 53. Which of the following types of interest cost incurred in connection with the purchase or manufacture of inventory should be capitalized as a product cost? a. Purchase discounts lost b. Interest incurred during the production of discrete projects such as ships or real estate projects c. Interest incurred on notes payable to vendors for routine purchases made on a repetitive basis d. All of these should be capitalized. 55. The use of a Purchase Discounts account implies that the recorded cost of a purchased inventory item is its a. invoice price. b. invoice price plus any purchase discount lost. c. invoice price less the purchase discount taken. d. invoice price less the purchase discount allowable whether taken or not. During 2014, which was the first year of operations, Oswald Company had merchandise purchases of $985,000 before cash discounts. All purchases were made on terms of 2/10, n/30. Three-fourths of the items purchased were paid for within 10 days of purchase. All of the goods available had been sold at year end. 57. Which of the following recording procedures would result in the highest net income for 2014? 1. Recording purchases at gross amounts 2. Recording purchases at net amounts, with the amount of discounts not taken shown under "other expenses" in the income statement a. 1 b. 2 c. Either 1 or 2 will result in the same net income. d. Cannot be determined from the information provided. 59. Costs which are inventoriable include all of the following except a. costs that are directly connected with the bringing of goods to the place of business of the buyer. b. costs that are directly connected with the converting of goods to a salable condition. c. buying costs of a purchasing department. d. selling costs of a sales department. 61. In situations where there is a rapid turnover, an inventory method which produces a balance sheet valuation similar to the first-in, first-out method is a. average cost. b. base stock. c. joint cost. d. prime cost. 63. An inventory pricing procedure in which the oldest costs incurred rarely have an effect on the ending inventory valuation is a. FIFO. b. LIFO. c. base stock. d. weighted-average. 65. Assuming no beginning inventory, what can be said about the trend of inventory prices if cost of goods sold computed when inventory is valued using the FIFO method exceeds cost of goods sold when inventory is valued using the LIFO method? a. Prices decreased. b. Prices remained unchanged. c. Prices increased. d. Price trend cannot be determined from information given. 67. In a period of rising prices, the inventory method which tends to give the highest reported inventory is a. FIFO. b. moving average. c. LIFO. d. weighted-average. 69. In a period of rising prices, the inventory method which tends to give the highest reported cost of goods sold is a. FIFO. b. average cost. c. LIFO. d. None of these choices are correct. 71. The acquisition cost of a certain raw material changes frequently. The book value of the inventory of this material at year end will be the same if perpetual records are kept as it would be under a periodic inventory method only if the book value is computed under the a. weighted-average method. b. moving average method. c. LIFO method. d. FIFO method. 73. In a period of rising prices which inventory method generally provides the greatest amount of net income? a. Average cost. b. FIFO. c. LIFO. d. Specific identification. 75. What is a LIFO reserve? a. The difference between the LIFO inventory and the amount used for internal reporting purposes. b. The tax savings attributed to using the LIFO method. c. The current effect of using LIFO on net income. d. Change in the LIFO inventory during the year. 77. Which of the following statements is true about specific-goods pooled LIFO approach? a. It determines and measures any increases and decreases in a pool in terms of total dollar value b. Most companies using a LIFO system prefer specific-goods pooled LIFO approach over dollar-value LIFO c. It usually results in large LIFO liquidation d. The reduction of one quantity in the pool may be offset by an increase in another 79. In the context of dollar-value LIFO, what is a LIFO layer? a. The difference between the LIFO inventory and the amount used for internal reporting purposes. b. The LIFO value of the inventory for a given year. c. The inventory in base year dollars. d. The LIFO value of an increase in the inventory for a given year. 81. Which of the following is not considered an advantage of LIFO when prices are rising? a. The inventory will be overstated. b. The more recent costs are matched against current revenues. c. There will be a deferral of income tax. d. A company's future reported earnings will not be affected substantially by future price declines. 83. The tax benefit that the LIFO method provides might get nullified when: a. unit costs tend to decrease as production increases. b. unit costs tend to increase as production increases. c. revenues are increasing faster than costs. d. a fairly constant “base stock” is present. Multiple Choice Answers—Conceptual Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. 21. c 31. d 41. d 51. b 61. a 71. d 81. a 23. a 33. a 43. a 53. b 63. a 73. b 83. c 25. c 35. d 45. d 55. a 65. a 75. a 27. d 37. b 47. c 57. c 67. a 77. d 29. b 39. b 49. d 59. d 69. c 79. d CHAPTER 8 MULTIPLE CHOICE—Computational 85. Lawson Manufacturing Company has the following account balances at year end: Office supplies $ 4,000 Raw materials 27,000 Work-in-process 59,000 Finished goods 102,000 Prepaid insurance 6,000 What amount should Lawson report as inventories in its balance sheet? a. $102,000. b. $106,000. c. $188,000. d. $192,000. 87. Malone Corporation uses the perpetual inventory method. On March 1, it purchased $60,000 of inventory, terms 2/10, n/30. On March 3, Malone returned goods that cost $6,000. On March 9, Malone paid the supplier. On March 9, Malone should credit a. purchase discounts for $1,200. b. inventory for $1,200. c. purchase discounts for $1,080. d. inventory for $1,080. 89. Bell Inc. took a physical inventory at the end of the year and determined that $810,000 of goods were on hand. In addition, the following items were not included in the physical count. Bell, Inc. determined that $96,000 of goods purchased were in transit that were shipped f.o.b. destination (goods were actually received by the company three days after the inventory count).The company sold $40,000 worth of inventory f.o.b. destination. What amount should Bell report as inventory at the end of the year? a. $810,000. b. $906,000. c. $850,000. d. $946,000. 91. Risers Inc. reported total assets of $3,200,000 and net income of $255,000 for the current year. Risers determined that inventory was understated by $69,000 at the beginning of the year and $30,000 at the end of the year. What is the corrected amount for total assets and net income for the year? a. $3,230,000 and $285,000. b. $3,170,000 and $294,000. c. $3,230,000 and $216,000. d. $3,200,000 and $255,000. 93. Hudson, Inc. is a calendar-year corporation. Its financial statements for the years 2015 and 2014 contained errors as follows: 2015 2014 Ending inventory $6,000 overstated $16,000 overstated Depreciation expense $4,000 understated $12,000 overstated Assume that no correcting entries were made at December 31, 2014. Ignoring income taxes, by how much will retained earnings at December 31, 2015 be overstated or understated? a. $ 2,000 understated b. $15,000 overstated c. $15,000 understated d. $18,000 understated 95. The following information is available for Naab Company for 2014: Freight-in $ 30,000 Purchase returns 75,000 Selling expenses 230,000 Ending inventory 260,000 The cost of goods sold is equal to 400% of selling expenses. What is the cost of goods available for sale? a. $ 920,000. b. $1,150,000. c. $1,135,000. d. $1,180,000. 97. Winsor Co. records purchases at net amounts. On May 5 Winsor purchased merchandise on account, $40,000, terms 2/10, n/30. Winsor returned $3,000 of the May 5 purchase and received credit on account. At May 31 the balance had not been paid. By how much should the account payable be adjusted on May 31? a. $ 0. b. $860. c. $800. d. $740. 99. The following information was available from the inventory records of Rich Company for January: Units Unit Cost Total Cost Balance at January 1 3,000 $9.77 $29,310 Purchases: January 6 2,000 10.30 20,600 January 26 2,700 10.71 28,917 Sales: January 7 (2,500) January 31 (3,700) Balance at January 31 1,500 Assuming that Rich maintains perpetual inventory records, what should be the inventory at January 31, using the moving-average inventory method, rounded to the nearest dollar? a. $15,757. b. $15,356. c. $15,390. d. $15,540. 101. Niles Co. has the following data related to an item of inventory: Inventory, March 1 200 units @ $2.10 Purchase, March 7 700 units @ $2.20 Purchase, March 16 140 units @ $2.25 Inventory, March 31 260 units The value assigned to cost of goods sold if Niles uses FIFO is a. $ 580. b. $ 552. c. $1,724. d. $1,696. 103. Transactions for the month of June were: Purchases Sales June 1 (balance) 1,600 @ $3.20 June 2 1,200 @ $5.50 3 4,400 @ 3.10 6 3,200 @ 5.50 7 2,400 @ 3.30 9 2,000 @ 5.50 15 3,600 @ 3.40 10 800 @ 6.00 22 1,000 @ 3.50 18 2,800 @ 6.00 25 400 @ 6.00 Assuming that perpetual inventory records are kept in units only, the ending inventory on a LIFO basis is a. $8,220. b. $8,320. c. $8,580. d. $8,940. 105. Using the above information and assuming that perpetual inventory records are kept in dollars, the ending inventory on a FIFO basis is a. $8,220. b. $8,320. c. $8,580. d. $8,940. 107. Milford Company had 500 units of “Tank” in its inventory at a cost of $4 each. It purchased, for $2,800, 300 more units of “Tank”. Milford then sold 400 units at a selling price of $10 each, resulting in a gross profit of $1,600. The cost flow assumption used by Milford a. is FIFO. b. is LIFO. c. is weighted average. d. cannot be determined from the information given. 109. June Corp. sells one product and uses a perpetual inventory system. The beginning inventory consisted of 40 units that cost $20 per unit. During the current month, the company purchased 240 units at $20 each. Sales during the month totaled 180 units for $43 each. What is the number of units in the ending inventory? a. 40 units. b. 60 units. c. 100 units. d. 280 units. 111. Checkers uses the periodic inventory system. For the current month, the beginning inventory consisted of 4,800 units that cost $12 each. During the month, the company made two purchases: 2,000 units at $13 each and 8,000 units at $13.50 each. Checkers also sold 8,600 units during the month. Using the average cost method, what is the amount of cost of goods sold for the month? a. $111,370. b. $115,800. c. $107,900. d. $111,800. 113. Checkers uses the periodic inventory system. For the current month, the beginning inventory consisted of 4,800 units that cost $12 each. During the month, the company made two purchases: 2,000 units at $13 each and 8,000 units at $13.50 each. Checkers also sold 8,600 units during the month. Using the FIFO method, what is the ending inventory? a. $80,292. b. $74,400. c. $83,700. d. $75,800. 115. Checkers uses the periodic inventory system. For the current month, the beginning inventory consisted of 4,800 units that cost $12 each. During the month, the company made two purchases: 2,000 units at $13 each and 8,000 units at $13.50 each. Checkers also sold 8,600 units during the month. Using the LIFO method, what is the ending inventory? a. $80,292. b. $74,400. c. $83,700. d. $75,800. 117. Black Corporation uses the FIFO method for internal reporting purposes and LIFO for external reporting purposes. The balance in the LIFO Reserve account at the end of 2014 was $140,000. The balance in the same account at the end of 2015 is $210,000. Black’s Cost of Goods Sold account has a balance of $1,050,000 from sales transactions recorded during the year. What amount should Black report as Cost of Goods Sold in the 2015 income statement? a. $ 980,000. b. $1,050,000. c. $1,120,000. d. $1,260,000. 119. Milford Company had 400 units of “Tank” in its inventory at a cost of $6 each. It purchased 600 more units of “Tank” at a cost of $9 each. Milford then sold 700 units at a selling price of $15 each. The LIFO liquidation overstated normal gross profit by a. $ -0- b. $300. c. $600. d. $900. 121. RF Company had January 1 inventory of $200,000 when it adopted dollar-value LIFO. During the year, purchases were $1,200,000 and sales were $2,000,000. December 31 inventory at year-end prices was $286,720, and the price index was 112. What is RF Company’s ending inventory? a. $200,000. b. $256,000. c. $262,720. d. $286,720. 123. Hay Company had January 1 inventory of $180,000 when it adopted dollar-value LIFO. During the year, purchases were $1,080,000 and sales were $1,800,000. December 31 inventory at year-end prices was $227,700, and the price index was 110. What is Hay Company’s ending inventory? a. $198,000. b. $207,000. c. $209,700. d. $227,700. 125. Gross Corporation adopted the dollar-value LIFO method of inventory valuation on December 31, 2013. Its inventory at that date was $550,000 and the relevant price index was 100. Information regarding inventory for subsequent years is as follows: Inventory at Current Date Current Prices Price Index December 31, 2014 $642,000 107 December 31, 2015 725,000 125 December 31, 2016 812,500 130 What is the cost of the ending inventory at December 31, 2014 under dollar-value LIFO? a. $600,000. b. $642,000. c. $603,500. d. $588,500. 127. What is the cost of the ending inventory at December 31, 2016 under dollar-value LIFO? a. $640,600. b. $637,000. c. $625,000. d. $658,500. 129. Web World began using dollar-value LIFO for costing its inventory last year. The base year layer consists of $400,000. Assuming the current inventory at end of year prices equals $552,000 and the index for the current year is 1.10, what is the ending inventory using dollar-value LIFO? a. $552,000. b. $512,000. c. $501,818. d. $607,200. 131. Opera Corp. uses the dollar-value LIFO method of computing its inventory cost. Data for the past three years is as follows: Year ended Inventory at Price December 31. End-of-year Prices Index 2013 $390,000 1.00 2014 756,000 1.05 2015 810,000 1.10 What is the 2013 inventory balance using dollar-value LIFO? a. $390,000. b. $371,424. c. $736,362. d. $810,000. 133. Opera Corp. uses dollar-value LIFO method of computing its inventory cost. Data for the past three years is as follows: Year ended Inventory at Price December 31. End-of-year Prices Index 2013 $ 390,000 1.00 2014 756,000 1.05 2015 810,000 1.10 What is the 2015 inventory balance using dollar-value LIFO? a. $810,000. b. $771,000. c. $736,500. d. $754,500. Multiple Choice Answers—Computational Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. CHAPTER 9 MULTIPLE CHOICE—Conceptual 21. Which of the following is true about lower-of-cost-or-market? a. It is inconsistent because losses are recognized but not gains. b. It usually understates assets. c. It can increase future income if the expected reductions do not materialize. d. All of these answers are correct. 23. When valuing raw materials inventory at lower-of-cost-or-market, what is the meaning of the term "market"? a. Net realizable value b. Net realizable value less a normal profit margin c. Current replacement cost d. Discounted present value 25. The designated market value a. is always the middle value of replacement cost, net realizable value, and net realizable value less a normal profit margin. b. should always be equal to net realizable value. c. may sometimes exceed net realizable value. d. should always be equal to net realizable value less a normal profit margin. 27. An item of inventory purchased this period for $15.00 has been incorrectly written down to its current replacement cost of $10.00. It sells during the following period for $30.00, its normal selling price, with disposal costs of $3.00 and normal profit of $12.00. Which of the following statements is not true? a. The cost of sales of the following year will be understated. b. The current year's income is understated. c. The closing inventory of the current year is understated. d. Income of the following year will be understated. 29. Lower-of-cost-or-market as it applies to inventory is best described as the a. drop of future utility below its original cost. b. method of determining cost of goods sold. c. assumption to determine inventory flow. d. change in inventory value to market value. 31. What is the rationale behind the ceiling when applying the lower-of-cost-or-market method to inventory? a. Prevents understatement of the inventory value. b. Allows for a normal profit to be earned. c. Allows for items to be valued at replacement cost. d. Prevents overstatement of the value of obsolete or damaged inventories. 33. Which of the following is not an acceptable approach in applying the lower-of-cost-or-market method to inventory? a. Inventory location. b. Categories of inventory items. c. Individual item. d. Total of the inventory. 35. Why might inventory be reported at sales prices (net realizable value or market price) rather than cost? a. When there is a controlled market with a quoted price applicable to all quantities and when there are no significant costs of disposal. b. When there are no significant costs of disposal. c. When a non-cancellable contract exists to sell the inventory. d. When there is a controlled market with a quoted price applicable to all quantities. 37. When inventory declines in value below original (historical) cost, and this decline is considered other than temporary, what is the maximum amount that the inventory can be valued at? a. Sales price b. Net realizable value c. Historical cost d. Net realizable value reduced by a normal profit margin 39. If a unit of inventory has declined in value below original cost, but the market value exceeds net realizable value, the amount to be used for purposes of inventory valuation is a. net realizable value. b. original cost. c. market value. d. net realizable value less a normal profit margin. 41. If a material amount of inventory has been ordered through a formal purchase contract at the balance sheet date for future delivery at firm prices, a. this fact must be disclosed. b. disclosure is required only if prices have declined since the date of the order. c. disclosure is required only if prices have since risen substantially. d. an appropriation of retained earnings is necessary. 43. In 2014, Orear Manufacturing signed a contract with a supplier to purchase raw materials in 2015 for $700,000. Before the December 31, 2014 balance sheet date, the market price for these materials dropped to $510,000. The journal entry to record this situation at December 31, 2014 will result in a credit that should be reported a. as a valuation account to Inventory on the balance sheet. b. as a current liability. c. as an appropriation of retained earnings. d. on the income statement. 45. At the end of the fiscal year, Apha Airlines has an outstanding purchase commitment for the purchase of 1 million gallons of jet fuel at a price of $4.60 per gallon for delivery during the coming summer. The company prices its inventory at the lower of cost or market. If the market price for jet fuel at the end of the year is $4.25, how would this situation be reflected in the annual financial statements? a. Record unrealized gains of $350,000 and disclose the existence of the purchase commitment. b. No impact. c. Record unrealized losses of $350,000 and disclose the existence of the purchase commitment. d. Only disclose the existence of the purchase commitment. 47. Which of the following is not a basic assumption of the gross profit method? a. The beginning inventory plus the purchases equal total goods to be accounted for. b. Goods not sold must be on hand. c. If the sales, reduced to the cost basis, are deducted from the sum of the opening inventory plus purchases, the result is the amount of inventory on hand. d. The total amount of purchases and the total amount of sales remain relatively unchanged from the comparable previous period. 49. Which statement is not true about the gross profit method of inventory valuation? a. It may be used to estimate inventories for interim statements. b. It may be used to estimate inventories for annual statements. c. It may be used by auditors. d. None of these answers are correct. 51. An inventory method which is designed to approximate inventory valuation at the lower of cost or market is a. last-in, first-out. b. first-in, first-out. c. conventional retail method. d. specific identification. 53. Which statement is true about the retail inventory method? a. It may not be used to estimate inventories for interim statements. b. It may not be used to estimate inventories for annual statements. c. It may not be used by auditors. d. None of these answers are correct. ] 55. To produce an inventory valuation which approximates the lower of cost or market using the conventional retail inventory method, the computation of the ratio of cost to retail should a. include markups but not markdowns. b. include markups and markdowns. c. ignore both markups and markdowns. d. include markdowns but not markups. 57. Which of the following is not required when using the retail inventory method? a. All inventory items must be categorized according to the retail markup percentage which reflects the item's selling price. b. A record of the total cost and retail value of the goods purchased. c. A record of the total cost and retail value of the goods available for sale. d. Total sales amount for the period. 59. What condition is not necessary in order to use the retail method to provide inventory results? a. Retailer keeps a record of the total costs of products sold for the period. b. Retailer keeps a record of the total costs and retail value of goods purchased. c. Retailer keeps a record of the total costs and retail value of goods available for sale. d. Retailer keeps a record of sales for the period. 61. What is the effect of net markups on the cost-retail ratio when using the conventional retail method? a. Increases the cost-to-retail ratio. b. No effect on the cost-to-retail ratio. c. Depends on the amount of the net markdowns. d. Decreases the cost-to-retail ratio. 63. Which of the following is not a common disclosure for inventories? a. Inventory composition. b. Inventory location. c. Inventory financing arrangements. d. Inventory costing methods employed. 65. The average days to sell inventory is computed by dividing a. 365 days by the inventory turnover ratio. b. the inventory turnover ratio by 365 days. c. net sales by the inventory turnover ratio. d. 365 days by cost of goods sold. *67. When using dollar-value LIFO, if the incremental layer was added last year, it should be multiplied by a. last year's cost ratio and this year's index. b. this year's cost ratio and this year's index. c. last year's cost ratio and last year's index. d. this year's cost ratio and last year's index. Multiple Choice Answers—Conceptual Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. CHAPTER 9 MULTIPLE CHOICE—Computational 69. Muckenthaler Company sells product 2005WSC for $40 per unit. The cost of one unit of 2005WSC is $36, and the replacement cost is $35. The estimated cost to dispose of a unit is $8, and the normal profit is 40%. At what amount per unit should product 2005WSC be reported, applying lower-of-cost-or-market? a. $16. b. $32. c. $35. d. $36. 71. Given the acquisition cost of product Z is $80, the net realizable value for product Z is $72, the normal profit for product Z is $6, and the market value (replacement cost) for product Z is $75, what is the proper per unit inventory price for product Z? a. $80. b. $75. c. $66. d. $72. 73. Given the acquisition cost of product Dominoe is $29, the net realizable value for product Dominoe is $26, the normal profit for product Dominoe is $3, and the market value (replacement cost) for product Dominoe is $27, what is the proper per unit inventory price for product Dominoe? a. $27. b. $23. c. $26. d. $29 75. Given the historical cost of product Z is $40, the selling price of product Z is $50, costs to sell product Z are $6, the replacement cost for product Z is $41, and the normal profit margin is 40% of sales price, what is the amount that should be used to value the inventory under the lower-of-cost-or-market method? a. $22. b. $40. c. $42. d. $41. 77. Given the historical cost of product Dominoe is $22, the selling price of product Dominoe is $30, costs to sell product Dominoe are $5, the replacement cost for product Dominoe is $20, and the normal profit margin is 20% of sales price, what is the amount that should be used to value the inventory under the lower-of-cost-or-market method? a. $22. b. $19. c. $20. d. $25. 79. Robust Inc. has the following information related to an item in its ending inventory. Packit (Product # 874) has a cost of $131, a replacement cost of $101, a net realizable value of $117, and a normal profit margin of $5. What is the final lower-of-cost-or-market inventory value for Packit? a. $112. b. $131. c. $101. d. $117. 81. Mortenson Corporation sells its product, a rare metal, in a controlled market with a quoted price applicable to all quantities. The total cost of 5,000 pounds of the metal now held in inventory is $150,000. The total selling price is $420,000, and estimated costs of disposal are $15,000. At what amount should the inventory of 5,000 pounds be reported in the balance sheet? a. $135,000. b. $150,000. c. $405,000. d. $420,000. 83. Turner Corporation acquired two inventory items at a lump-sum cost of $100,000. The acquisition included 3,000 units of product LF, and 7,000 units of product 1B. LF normally sells for $30 per unit, and 1B for $10 per unit. If Turner sells 1,000 units of LF, what amount of gross profit should it recognize? a. $3,750 b. $11,250. c. $20,000. d. $23,750. 85. At a lump-sum cost of $72,000, Pratt Company recently purchased the following items for resale: Item No. of Items Purchased Resale Price Per Unit M 4,000 $3.75 N 2,000 12.00 O 6,000 6.00 The appropriate cost per unit of inventory is: M N O a. $3.75 $12.00 $6.00 b. $3.11 $19.86 $3.32 c. $3.60 $11.52 $5.76 d. $6.00 $6.00 $6.00 87. Confectioners, a chain of candy stores, purchases its candy in bulk from its suppliers. For a recent shipment, the company paid $1,500 and received 8,500 pieces of candy that are allocated among three groups. Group 1 consists of 2,500 pieces that are expected to sell for $0.15 each. Group 2 consists of 5,500 pieces that are expected to sell for $0.36 each. Group 3 consists of 500 pieces that are expected to sell for $0.72 each. Using the relative sales value method, what is the cost per item in Group 2? a. $0.19. b. $0.30. c. $0.18. d. $0.20. 89. During the current fiscal year, Jeremiah Corp. signed a long-term noncancellable purchase commitment with its primary supplier. Jeremiah agreed to purchase $1.5 million of raw materials during the next fiscal year under this contract. At the end of the current fiscal year, the raw material to be purchased under this contract had a market value of $1.2 million. What is the journal entry at the end of the current fiscal year? a. Debit Unrealized Holding Gain or Loss for $300,000 and credit Estimated Liability on Purchase Commitment for $300,000. b. Debit Estimated liability on Purchase Commitments for $300,000 and credit Unrealized Holding Gain or Loss for $300,000. c. Debit Unrealized Holding Gain or Loss for $1,200,000 and credit Estimated Liability on Purchase Commitments for $1,200,000. d. No journal entry is required. 91. During 2014, Larue Co., a manufacturer of chocolate candies, contracted to purchase 200,000 pounds of cocoa beans at $4.00 per pound, delivery to be made in the spring of 2015. Because a record harvest is predicted for 2015, the price per pound for cocoa beans had fallen to $3.30 by December 31, 2014. Of the following journal entries, the one which would properly reflect in 2014 the effect of the commitment of Larue Co. to purchase the 200,000 pounds of cocoa is a. Cocoa Inventory 800,000 Accounts Payable 800,000 b. Cocoa Inventory 660,000 Loss on Purchase Commitments 140,000 Accounts Payable 800,000 c. Unrealized Holding Gain or Loss-Income 140,000 Estimated Liability on Purchase Commitments 140,000 d. No entry would be necessary in 2014 93. LF Corporation, a manufacturer of Mexican foods, contracted in 2014 to purchase 1,500 pounds of a spice mixture at $5.00 per pound, delivery to be made in spring of 2015. By 12/31/14, the price per pound of the spice mixture had dropped to $4.70 per pound. In 2014, LF should recognize a a loss of $7,500. b. a loss of $450. c. no gain or loss. d. a gain of $450. 95. The following information is available for October for Norton Company. Beginning inventory $300,000 Net purchases 900,000 Net sales 1,800,000 Percentage markup on cost 66.67% A fire destroyed Norton’s October 31 inventory, leaving undamaged inventory with a cost of $18,000. Using the gross profit method, the estimated ending inventory destroyed by fire is a. $102,000. b. $462,000. c. $480,000. d. $600,000. 97. Miles Company, a wholesaler, budgeted the following sales for the indicated months: June July August Sales on account $2,700,000 $2,760,000 $2,850,000 Cash sales 270,000 300,000 390,000 Total sales $2,970,000 $3,060,000 $3,240,000 All merchandise is marked up to sell at its invoice cost plus 25%. Merchandise inventories at the beginning of each month are at 30% of that month's projected cost of goods sold. Merchandise purchases for July are anticipated to be a. $2,295,000. b. $3,114,000. c. $2,448,000. d. $2,491,200. 99. A markup of 20% on cost is equivalent to what markup on selling price? a. 17% b. 20% c. 80% d. 83% 101. On January 1, 2014, the merchandise inventory of Glaus, Inc. was $1,200,000. During 2014 Glaus purchased $2,400,000 of merchandise and recorded sales of $3,000,000. The gross profit rate on these sales was 25%. What is the merchandise inventory of Glaus at December 31, 2014? a. $600,000. b. $750,000. c. $1,350,000. d. $2,250,000. 103. On April 15 of the current year, a fire destroyed the entire uninsured inventory of a retail store. The following data are available: Sales, January 1 through April 15 $480,000 Inventory, January 1 80,000 Purchases, January 1 through April 15 400,000 Markup on cost 25% The amount of the inventory loss is estimated to be a. $96,000. b. $48,000. c. $120,000. d. $80,000. 105. The sales price for a product provides a gross profit of 25% of sales price. What is the gross profit as a percentage of cost? a. 25%. b. 20%. c. 33%. d. Not enough information is provided to determine. 107. On August 31, a hurricane destroyed a retail location of Vinny's Clothier including the entire inventory on hand at the location. The inventory on hand as of June 30 totaled $960,000. Since June 30 until the time of the hurricane, the company made purchases of $255,000 and had sales of $750,000. Assuming the rate of gross profit to selling price is 40%, what is the approximate value of the inventory that was destroyed? a. $960,000. b. $544,500. c. $615,000. d. $765,000. 109. On March 15, a fire destroyed Interlock Company's entire retail inventory. The inventory on hand as of January 1 totaled $4,950,000. From January 1 through the time of the fire, the company made purchases of $2,049,000, incurred freight-in of $234,000, and had sales of $3,630,000. Assuming the rate of gross profit to selling price is 30%, what is the approximate value of the inventory that was destroyed? a. $6,144,000. b. $4,458,000. c. $4,692,000. d. $7,233,000. 111. Boxer Inc. uses the conventional retail method to determine its ending inventory at cost. Assume the beginning inventory at cost (retail) were $196,500 ($297,000), purchases during the current year at cost (retail) were $1,704,000 ($2,596,800), freight-in on these purchases totaled $79,500, sales during the current year totaled $2,333,000, and net markups were $207,000. What is the ending inventory value at cost? a. $767,800. b. $541,425. c. $490,624. d. $525,175. 113. Crane Sales Company uses the retail inventory method to value its merchandise inventory. The following information is available for the current year: Cost Retail Beginning inventory $ 30,000 $ 45,000 Purchases 175,000 240,000 Freight-in 2,500 — Net markups — 8,500 Net markdowns — 10,000 Employee discounts — 1,000 Sales revenue — 205,000 If the ending inventory is to be valued at the lower-of-cost-or-market, what is the cost-to-retail ratio? a. $207,500 ÷ $285,000 b. $207,500 ÷ $293,500 c. $205,000 ÷ $295,000 d. $207,500 ÷ $283,500 Use the following information for questions 115 and 117 The following data concerning the retail inventory method are taken from the financial records of Welch Company. Cost Retail Beginning inventory $ 147,000 $ 210,000 Purchases 672,000 960,000 Freight-in 18,000 — Net markups — 60,000 Net markdowns — 42,000 Sales — 1,008,000 115. If the ending inventory is to be valued at approximately the lower of cost or market, the calculation of the cost-to-retail ratio should be based on goods available for sale at (1) cost and (2) retail, respectively of a. $837,000 and $1,230,000. b. $837,000 and $1,188,000. c. $837,000 and $1,170,000. d. $819,000 and $1,170,000. *117. Assuming no change in the price level if the LIFO inventory method were used in conjunction with the data, the ending inventory at cost would be a. $127,800. b. $126,000. c. $122,400. d. $129,600. 119. Drake Corporation had the following amounts, all at retail: Beginning inventory $ 3,600 Purchases $140,000 Purchase returns 6,000 Net markups 18,000 Abnormal shortage 4,000 Net markdowns 2,800 Sales revenue 77,000 Sales returns 1,800 Employee discounts 1,600 Normal shortage 2,600 What is Drake’s ending inventory at retail? a. $69,400. b. $71,000. c. $72,600. d. $73,400 121. Fry Corporation’s computation of cost of goods sold is: Beginning inventory $ 60,000 Add: Cost of goods purchased 530,000 Cost of goods available for sale 590,000 Ending inventory 80,000 Cost of goods sold $510,000 The average days to sell inventory for Fry are a. 42.9 days. b. 43.5 days. c. 50.0 days. d. 57.0 days. 123. The 2014 financial statements of Sito Company reported a beginning inventory of $80,000, an ending inventory of $120,000, and cost of goods sold of $900,000 for the year. Sito’s inventory turnover ratio for 2014 is a. 11.3 times. b. 9.0 times. c. 7.5 times. d. 6.5 times. Use the following information for questions 125 through 129. Plank Co. uses the retail inventory method. The following information is available for the current year. Cost Retail Beginning inventory $ 234,000 $366,000 Purchases 885,000 1,245,000 Freight-in 15,000 — Employee discounts — 6,000 Net markups — 45,000 Net markdowns — 60,000 Sales revenue — 1,170,000 125. If the ending inventory is to be valued at approximately lower of average cost or market, the calculation of the cost ratio should be based on cost and retail of a. $900,000 and $1,290,000. b. $900,000 and $1,284,000. c. $1,119,000 and $1,650,000. d. $1,134,000 and $1,656,000. 127. The approximate cost of the ending inventory by the conventional retail method is a. $287,700. b. $284,760. c. $294,000. d. $307,440. *129. Assuming that the LIFO inventory method is used, that the beginning inventory is the base inventory when the index was 100, and that the index at year end is 112, the ending inventory at dollar-value LIFO retail cost is a. $241,379. b. $278,271. c. $287,700. d. $307,440. 131. Eaton Company, which uses the retail LIFO method to determine inventory cost, has provided the following information for 2014: Cost Retail Inventory, 1/1/14 $ 188,000 $280,000 Net purchases 756,000 1,124,000 Net markups 136,000 Net markdowns 60,000 Net sales 1,060,000 Assuming that the price index was 105 at December 31, 2014 and 100 at January 1, 2014, what is the cost of Eaton's inventory at December 31, 2014 under the dollar-value-LIFO retail method? a. $267,380. b. $277,830. c. $280,610. d. $263,600. Multiple Choice Answers—Computational Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. [Show More]

Last updated: 3 years ago

Preview 1 out of 41 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Buy NowInstant download

We Accept:

Reviews( 0 )

$9.00

Can't find what you want? Try our AI powered Search

Document information

Connected school, study & course

About the document

Uploaded On

May 28, 2020

Number of pages

41

Written in

All

Additional information

This document has been written for:

Uploaded

May 28, 2020

Downloads

0

Views

162

.png)

.png)

.png)

.png)

.png)

.png)

.png)